Philanthropy

Three steps that can help your endowment or foundation shine

Creating a legacy is one of the most satisfying roads we can take, whether it’s in the form of running a successful business, providing for our loved ones or making a more personal contribution to the world. However, when we leverage some of that work for the general good, it carries an additional reward — a sense that we’ve made a mark that will benefit others, possibly for generations to come.

Maybe that’s why so many successful people serve on the boards of nonprofits. Whether it’s combating hunger, enriching culture or providing for the families of first responders, involvement in endowments and foundations provides a chance to directly promote worthy causes.

But despite the dizzying range of goals such organizations pursue, they all face the same fundamental question: How can we effectively fund our mission?

That question is clearly paramount for new groups, but it’s still relevant for venerable institutions. As groups mature, their objectives can grow or shift. Sound investment advice can turn creaky as economic reality changes. Organizations and their directors must constantly evaluate their mission and how they’re approaching it.

“We recommend that endowments and foundations review their funding plans and distribution goals periodically,” says Aaron Petersen, a senior wealth advisory manager with Capital Group Private Client Services. “With so many changing variables, it’s easy for an organization to find itself getting off track over time.”

Of course, every nonprofit has its own needs and hazards. You should consult your group’s legal and financial advisors before making any changes. But there are some things you can consider when thinking about how you and your group can better approach your goals.

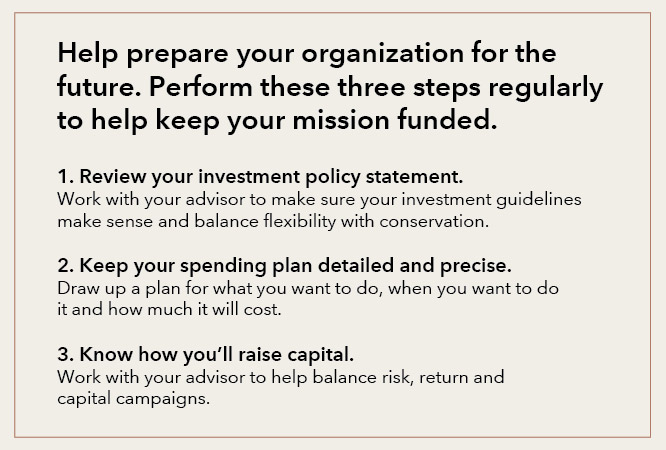

No. 1: Examine your organization’s investment policy statement.

An investment policy statement is the set of guidelines that dictate how your organization can invest. The goal is to help your group responsibly fund its mission by limiting risk and generating income. As a result, many such documents set requirements for withdrawals, returns, asset allocation and other metrics.

Board members should be familiar with the investment policy statement, Petersen says, because the investment rules could impact your group’s mission. For example, particularly conservative statements could make it difficult to meet return objectives, which could shape your group’s goals and how it pursues them.

Your Private Wealth Advisor can help you identify ways to make your group’s investment policy statement better work for your organization, Petersen says.

“The longer you go without evaluating your investment policy statement, the more likely it is to be out of date,” he says. “It’s like any other guiding document — it must be maintained and updated to meet your organization’s changing needs. I recommend boards review it annually.”

No. 2: Make sure your group has concrete objectives.

Of course, every endowment and foundation has a mission. But whether you’re housing the needy or funding art projects, your organization could be handicapping itself if it’s not outlining exactly how and when to spend its funds.

“If you don’t know how much you’ll need to fund a project or program, it’s hard to know how long you can sustain it,” Petersen explains. “It’s incredibly important to understand the organization’s long-term distribution plan.”

Your organization may already know some of these details, such as whether it plans to last for perpetuity or draw down its funds. Other, aspirational questions can pop up again many times over an organization’s life: Do you want to expand the work you’re doing? Do you want to pursue larger projects, such as building a food bank or a museum? Hammering out a long-term plan can set your group on a solid path and give a detailed idea of how much capital you’ll need. And that’s key to knowing how you will need to invest and fundraise to meet your goals.

“Once you have a detailed blueprint for what you want, you can create a plan to get you there,” Petersen says. “Your Private Wealth Advisors can help you understand the trade-offs to make your goals, investments and funding campaigns make sense.”

No. 3: Consider what kind of risk-return profile your group needs to accomplish its goals.

Once you have a sense of how much your group will need to accomplish its goals, you’ll want to put an investment plan into place. This lets you understand which goals the portfolio might support and how much you’ll need to raise through capital campaigns.

And it’s important to assess all your available tools when determining what your group’s portfolio might be able to support. For example, considering total return is an appropriate, but often overlooked, approach to constructing a portfolio, Petersen says. Some boards concentrate on yield, such as interest payments from bonds or dividends from stocks, to meet distribution needs. While such payments historically tend to boast lower volatility and a more predictable cash flow, they’re just one potential source of returns for a portfolio. By concentrating solely on yield, boards can actually limit what an organization can distribute.

Overall, managing an endowment or foundation can be a meaningful experience, but it requires dedication and clarity of purpose. By working with their Private Wealth Advisor to maintain up-to-date investment rules and concrete goals, board members can help their organization benefit their communities for years to come.

Learn more about

Related Insights

Related Insights

-

-

Wealth Planning

-

Demographics & Culture