Wealth Planning

Legacy

Charitable LLCs provide another option for making philanthropic gifts

Michelle Black

Michelle Black

March 31, 2019

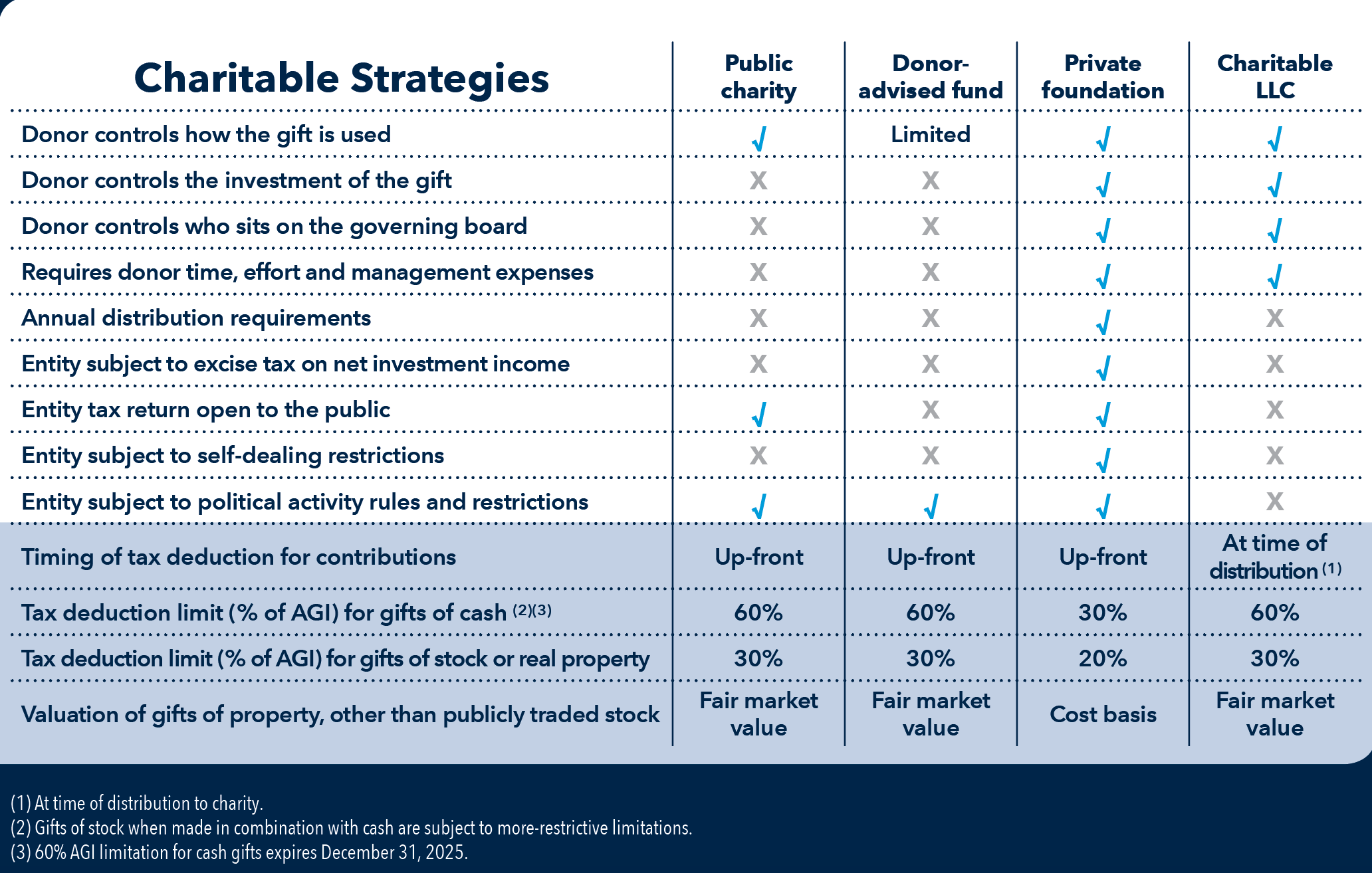

Those who make charitable donations typically do so in one of three ways: contributing directly to a charity, using a donor-advised fund or establishing a private foundation. Each of these approaches can have distinct benefits depending on the donor’s philanthropic goals and financial circumstances. These remain the preferred vehicles for most people, but another mechanism, known as a charitable LLC, may be worthwhile for donors in certain situations.

As the name implies, a charitable LLC is a limited liability company. Its primary advantage is that it generally provides donors with greater flexibility and control than do traditional tax-exempt entities. LLCs are not bound by some of the regulations that typically govern more-common philanthropic vehicles, including rules on required distributions, public disclosures, investment holdings and political involvement. Among the more notable adherents of the LLC model are Facebook founder Mark Zuckerberg and his wife, Priscilla, who use an LLC as their primary philanthropic vehicle, and Laurene Powell Jobs, the widow of Apple co-founder Steve Jobs, who created an LLC known as Emerson Collective.

As with any type of charitable-gifting mechanism, LLCs involve trade-offs, and they must be examined carefully in the context of overall philanthropic and financial strategies. One of the most notable trade-offs is that LLCs are not technically charitable vehicles and do not offer tax advantages per se. In contrast to other types of vehicles, for example, donor contributions to LLCs do not provide immediate charitable deductions. Instead, deductions come later when the LLC itself disburses money. Nevertheless, the convenience and freedom can make an LLC an appealing choice for donors in some situations.

LLCs offer autonomy with relatively few headaches.

Among the most compelling features of a charitable LLC is that there is less paperwork involved — and less public disclosure required — than with other charitable vehicles. For tax purposes, an LLC is a pass-through entity, meaning that all financial activity passes through to its owner. LLCs don’t have to submit annual 990-PF forms, which are public documents that list, among other facts, the compensation of top executives and independent contractors. Thus, LLCs can be particularly attractive to those seeking a high degree of personal privacy.

There are no annual distribution requirements with LLCs. That stands in contrast to family foundations, which must give away at least 5% of their net investment assets each year. LLCs also are not subject to so-called self-dealing restrictions that prohibit foundations from holding more than 20% of a single stock. That gives donors much more leeway to invest in a family-owned business or in entities that are considered to be speculative in nature. And unlike family foundations, LLCs are allowed to lobby government officials on behalf of their causes and make financial contributions to political campaigns.

LLCs don’t have specific tax advantages.

The logistical benefits of LLCs must be considered alongside their relative disadvantages — starting with the fact that LLCs don’t carry tax benefits. One of their most notable drawbacks is their lack of up-front tax deductibility. Contributions to public charities, donor-advised funds and foundations all are deductible the moment a donor makes a gift. That’s not the case with an LLC; deductions apply only when the entity itself disburses money to a qualified 501(c)(3).

If charitable LLCs don’t carry immediate tax benefits, why not just give directly to charities? The answer lies primarily with an LLC’s intangible benefits. First, an LLC can, in effect, be the “entity” through which a family carries out its philanthropic objectives. This work might include research, due diligence and the administration of implementing multiple grants over time. A private foundation can accomplish these tasks as well but comes with additional restrictions, including the minimum distribution requirement, self-dealing prohibitions and reporting obligations.

Second, an LLC enables family members who are actively engaged with the charitable work to be compensated as employees. Finally, an LLC can be used in conjunction with direct giving, a donor-advised fund or even a private foundation, if desired. This may be especially appealing for investors who want to create a legacy with large, private holdings but prefer the simplicity of non-LLC vehicles or need the up-front tax deduction.

Of course, tax rules are complex and can have diverse applications for different individuals. It’s extremely important for people considering charitable vehicles to consult with their tax and legal advisors before pursuing any strategies. Our Wealth Advisory Group can help with the decision-making process through a customized planning analysis. Please contact your Private Wealth Advisor for more information.

The above article originally appeared in the Spring 2019 issue of Quarterly Insights magazine.

Explore topics

Related Insights

Related Insights

-

-

Life Events

-