Active Management

Categories

Bonds

Bond outlook: Strong yields offer upside as risks linger

Chitrang Purani

Chitrang Purani

Damien McCann

Damien McCann

Timothy Ng

Timothy Ng

June 17, 2026

KEY TAKEAWAYS

- Elevated bond yields have created a more favourable entry point.

- Markets expect U.S. Federal Reserve (the Fed) rate hikes, but we see a patient Fed as more likely.

- Strong fundamentals provide selective opportunity across credit sectors.

Halfway through the year, bond markets are contending with the twists and turns of war in Iran, shifting labour market dynamics and heightened risks to economic growth.

“Bond markets have been influenced by the inflationary impact of higher energy prices,” says portfolio manager Chitrang Purani. "But I’m increasingly concerned about how the war could weigh on economic growth as certain consumers have little buffer to absorb another inflation spike.”

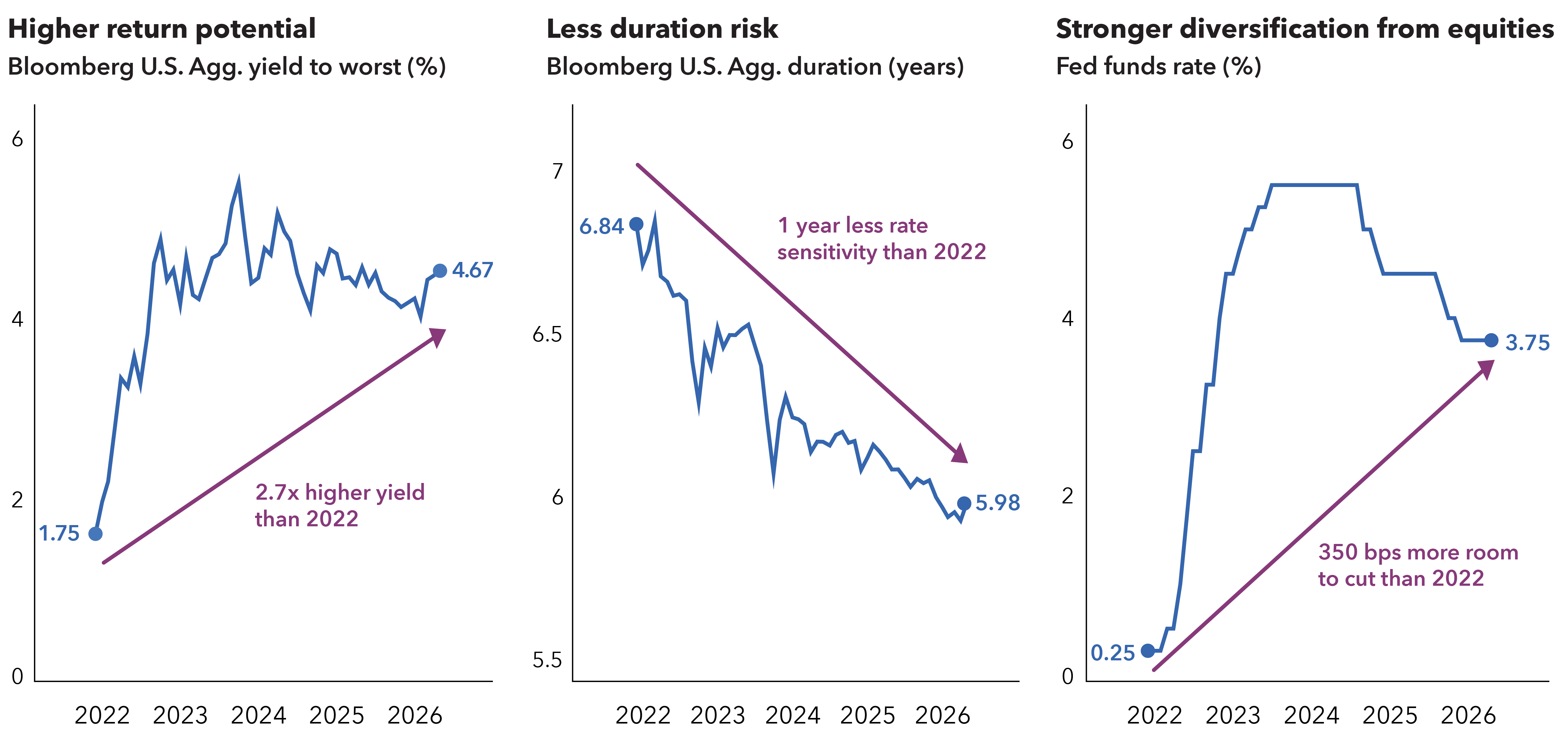

While bond returns this year have been muted, this view suggests that ample starting yields could lead to a stronger second half as elevated rates either persist or drift down to boost total returns. The Bloomberg U.S. Aggregate Bond Index, which delivered a 7% return in 2025, now offers a starting yield of 4.7%, up about 40 basis points (bps) from year-end.

Bonds hit a sweet spot for income and diversification

Sources: Capital Group, Bloomberg. As of May 31, 2026. Duration is a measure of a bond’s price sensitivity to interest rate changes, expressed in years. Yield-to-worst is the lowest possible annualized return an investor could receive, assuming no default and that the bond is called, put or held to maturity. Fed funds target rate reflects upper bound of range. Returns are in USD.

“We remain in this period of elevated yields, which is a great setup for forward returns,” says Damian McCann, portfolio manager for Capital Group Multi-Sector Income FundTM (Canada) and Capital Group Multi-Sector Income Select ETFTM (Canada). “You’d have to go back about 17 years to find another period where forward return expectations are as attractive as they’ve been in recent years.”

Interest rate strategy comes into focus

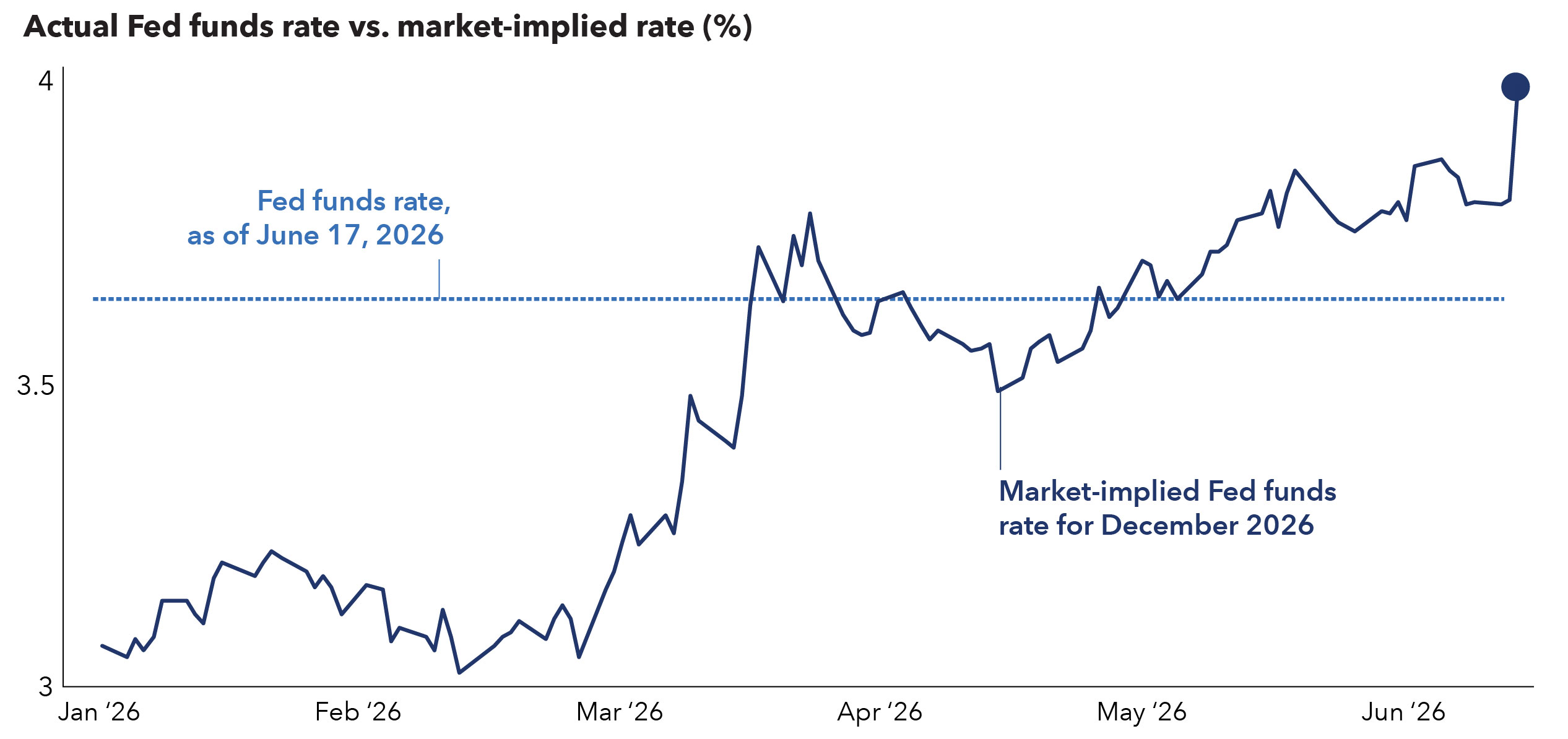

Inflation concerns dominated bond market sentiment in the first half of the year, with the U.S. Consumer Price Index (CPI) rising from 2.4% in February to reach 4.2% in May, its highest level in three years. This has led the market to reprice the Fed expectations toward seeing a rate hike more likely than a cut.

Markets expect U.S. rate hikes, but we see a patient Fed as more likely

Sources: Capital Group, Bloomberg. As of June 17, 2026. The federal funds rate shown is the midpoint of the upper and lower bounds of the U.S. Federal Reserve’s target range for the federal funds rate. Market-implied federal funds rates are derived from federal funds futures pricing and reflect market expectations. These expectations are subject to change and may differ from actual U.S. Federal Reserve decisions.

But several factors could help inflation stay more contained, especially when compared to past inflationary episodes. Money supply growth and bank lending are running at significantly lower levels than in prior surges, suggesting less fuel for sustained price pressures. The consumer also appears more constrained as the savings rate remains low and wage growth is tepid. These dynamics point to a more limited and potentially self-dampening inflation impulse.

History also shows that oil-driven inflation shocks have not translated into a consistent long-term path for U.S. Treasury yields. Yields have often risen in the near term, but over a one-year horizon there doesn’t appear to be a clear cause-and-effect relationship between the initial oil shock and where yields ultimately settle.

Core inflation holds steady amid high energy prices

Sources: Capital Group, U.S. Bureau of Labor Statistics, Bloomberg. Data shown is CPI for all items. Latest data available is for May 2026 as of June 10, 2026.

Inflation pressures within the core PCE Index — the Fed’s preferred U.S. inflation measure — remain muted. At the same time, real consumer income growth and spending growth have declined, while a key measure of consumer confidence1 dropped to an all-time low in May. We're watching inflation and labour market developments closely to monitor for changes in underlying consumer strength. We believe these factors may lead the Fed to stay on hold rather than hike rates over the next several quarters.

“Higher oil prices are pushing up the cost of living for consumers already under pressure from weak wage growth, depleted savings and softening economic sentiment,” says Timothy Ng, portfolio manager for Capital Group Canadian Core Plus Fixed Income FundTM (Canada).

Against this backdrop, we find it favourable to extend duration within bond portfolios. The recent rise in rates, with 10-year U.S. Treasury yields hitting above 4.6% in May, has translated into strong starting yields and attractive valuations. The position also serves as a potential hedge against further economic softening.

Beyond geopolitics, longer term forces such as artificial intelligence may also support lower rates across a range of outcomes. Strong productivity gains could help dampen inflation, while potential disruption to labour markets or risk sentiment could accelerate the need for a Fed response. Additionally, a Fed helmed by chairman Kevin Warsh is anticipated to lean more dovish.

If economic prospects fade and the Fed resumes cuts, that could lead to a steepening of the U.S. Treasury yield curve as short-term yields fall and long-term yields rise.

Strong fundamentals provide selective opportunity across credit sectors

The outlook for credit reflects a combination of attractive starting yields and largely resilient fundamentals. Elevated yields provide meaningful income support, and although spreads are tight, they can be justified by strengthening fundamentals. In this environment, we're finding value in a diversified and flexible approach to credit investing.

“The outlook for credit quality remains strong, and we expect that strength to continue,” says McCann. “Overall, this is a supportive environment for credit returns.”

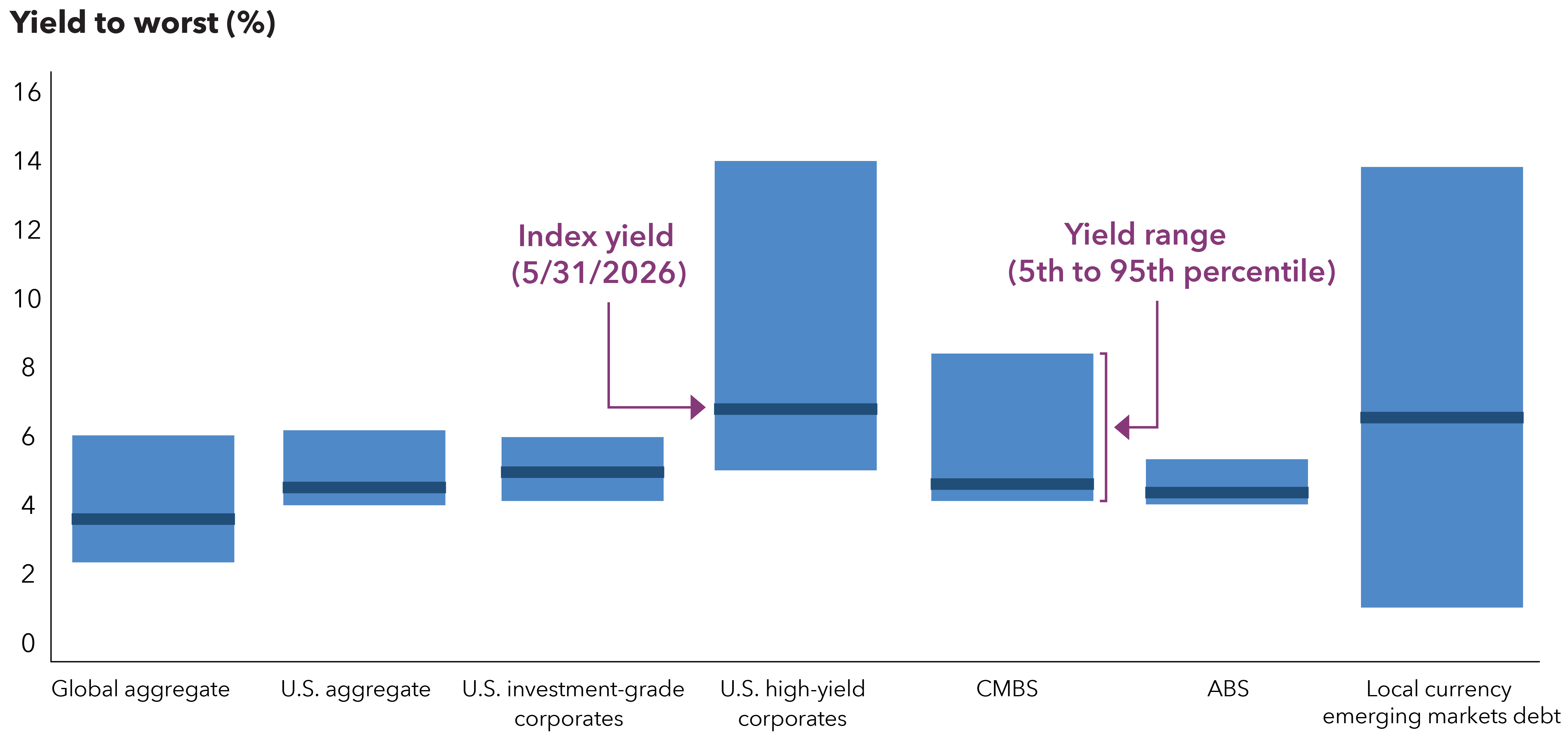

With widening dispersion, broad-based exposure is less attractive. Rather, yield and spread differences across sectors and within rating cohorts are creating opportunities for issuer selection.

Key credit sectors offer attractive yield

Sources: Capital Group, Bloomberg, J.P. Morgan. As of May 31, 2026. Global aggregate is the Bloomberg Global Aggregate Bond Index. U.S. investment-grade corporates is the Bloomberg Corporate Investment Grade Index. U.S. high-yield corporates is the Bloomberg U.S. Corporate High Yield 2% Issuer Capped Index, CMBS is the Bloomberg CMBS: Erisa Eligible Index, ABS is the Bloomberg ABS Index, Local currency emerging markets debt is the J.P. Morgan GBI-EM Global Diversified Index.

Investment‑grade (BBB/Baa-rated and above) corporates remain supported by strong corporate balance sheets and disciplined capital allocation. Net leverage levels have held relatively steady, reflecting a measured approach to financing, including around merger and acquisitions activity.

One key area of interest is debt tied to AI and data centre investment, where large issuers with well‑capitalized balance sheets, resilient cash flows and high credit ratings are helping drive what may be a record year for investment-grade issuance. “Most of the AI financing has come from the hyperscalers,” McCann says. “The resulting supply has widened spreads just enough to create opportunity in very high‑quality credit.” Areas such as pharmaceuticals, utilities and managed care also stand out, where factors ranging from new product launches to wildfire mitigation efforts and stronger underwriting may support further spread compression.

We have high conviction in the securitized debt universe, where valuations remain attractive relative to corporates and fundamentals remain positive. Although our outlook on mortgage-backed securities has faded somewhat in recent quarters as valuations look less attractive, other parts of the sector have our attention. A slow-motion recovery in commercial real estate is creating opportunities in commercial mortgage-backed securities as refinancing conditions improve and help drive sales transactions and price discovery. Asset‑backed securities are benefiting from robust structural protections that are helping insulate investors from mixed consumer balance sheets.

Within the high-yield universe, fundamentals also appear relatively solid. Leverage has risen only modestly from recent lows while cash balances and interest coverage ratios remain healthy. The impact from tariffs has been manageable, and elevated operating costs have largely flowed through to consumers. High-yield spreads may look a little tight relative to other sectors, making security selection key in industries such as media and commercial real estate. Across the sector, an improvement in credit quality and a short duration help explain why spreads are tight relative to history.

In emerging markets debt, robust yields paired with healthy fundamentals are creating compelling opportunities. A number of sovereign issuers offer higher real yields and relatively lower debt levels than many developed markets, including the United States. Positioning is highly differentiated by region, with greater conviction in parts of Latin America and a more cautious stance towards areas that are more sensitive to energy prices or geopolitical risk. Local currency bond markets also stand out, offering both income potential and a possible hedge against a weaker U.S. dollar.

Overall, the case for credit is less about chasing spread compression and more about obtaining income from fundamentally sound issuers in an elevated rate environment.

Robust yields paired with healthy fundamentals drive emerging markets debt

Sources: Bloomberg, International Monetary Fund, J.P. Morgan. Real yields data as of May 31, 2026. Real yields represent country yield components of the J.P. Morgan GBI-EM Global Diversified Index minus core inflation. U.S. real yields represent five-year U.S. Treasury yields minus U.S. core inflation. Debt-to-GDP represents general government gross debt as a percent of GDP and is sourced from the IMF's World Economic Outlook report from April 2026.

Income and ballast in a shifting landscape

Elevated yields have strengthened the opportunity set in fixed income, creating a more favourable entry point. Duration positioning and an emphasis on diversification and flexibility across credit sectors can help investors target attractive returns. Should economic conditions weaken, bonds are also in a position to play their historically critical role in providing diversification from equities and other risk assets. That ballast may prove especially valuable as markets navigate geopolitical uncertainty and downside risks to growth in the second half of the year.

Learn more about

1The University of Michigan Consumer Sentiment Index fell to 44.8 in May, down from 49.8 in April, and the lowest level on record.

Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Bond ratings, which typically range from AAA/Aaa (highest) to D (lowest), are assigned by credit rating agencies such as Standard & Poor's, Moody's and/or Fitch, as an indication of an issuer's creditworthiness.

A spread over Treasuries is the difference between the yield of a bond and the yield of a similar maturity Treasury bond.

Duration measures a bond’s sensitivity to changes in interest rates. Generally speaking, a bond's price will go up 1% for every year of duration if interest rates fall by 1% or down 1% for every year of duration if interest rates rise by 1%.

Hyperscalers are large-scale cloud service providers that offer computing power and storage to organizations and individuals globally.

Bloomberg U.S. Aggregate Bond Index represents the U.S. investment-grade fixed-rate bond market.

Bloomberg U.S. Corporate High Yield 2% Issuer Capped Index covers the universe of fixed-rate, non-investment-grade debt. The index limits the maximum exposure of any one issuer to 2%.

Bloomberg U.S. Corporate Investment Grade Index represents the universe of investment-grade, publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity and quality requirements.

Bloomberg CMBS Index represents the universe of U.S. commercial mortgage-backed securities.

Bloomberg ABS Index represents the universe of U.S. asset-backed securities.

JP Morgan Government Bond Index – Emerging Markets (GBI-EM) Global Diversified covers the universe of regularly traded, liquid fixed-rate, domestic currency emerging market government bonds to which international investors can gain exposure

.

This report, and any product, index or fund referred to herein, is not sponsored, endorsed or promoted in any way by J.P. Morgan or any of its affiliates who provide no warranties whatsoever, express or implied, and shall have no liability to any prospective investor, in connection with this report. J.P. Morgan disclaimer: https://www.jpmm.com/research/disclosures.

Our latest insights

RELATED INSIGHTS

-

Economic Indicators

-

-

Economic Indicators

Commissions, trailing commissions, management fees and expenses all may be associated with investments in investment funds. Please read the prospectus before investing. Investment funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. For investment funds other than money market funds, their values change frequently. For money market funds, there can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian investment funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2026. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.