Active Management

Categories

Global Equities

Rob Lovelace on the year ahead

Rob Lovelace

Rob Lovelace

February 12, 2026

As 2026 unfolds, markets are once again climbing a proverbial wall of worry. Trade wars, geopolitical conflicts and fears of a bubble in AI stocks have shaken investor confidence at times, but markets have managed to look past these daunting events and forge ahead. Can this remarkable resilience continue?

In a wide-ranging Q&A, Rob Lovelace, equity portfolio manager and chair of Capital International, Inc. offers his view on where stock markets are headed, how changes in global trade are reshaping the global economy, and why rapid advancements in artificial intelligence (AI) are among the most compelling investment themes reflected in his portfolios.

After three years of double-digit returns, what’s your outlook for global equities in 2026?

My starting point would be: Does it matter that we've had three double-digit up markets? I'll just start with a blank piece of paper, which I think is a good way to start any year. Corporate profits in the U.S. are strong. They are generally concentrated in certain sectors, such as technology and related areas, but financials have also been strong. With higher interest rates, banks are generating better profit margins. The lending environment has improved. For all the talk about U.S. market concentration, it isn't just about technology. When I look at the market going forward, the key element is that underpinning of strong earnings. Earnings growth has been evident for the last three years, and it doesn't look like it's slowing down.

Outside the U.S., companies are scrambling to deal with a new wiring for global trade. There's a new order emerging. As that reordering happens, there will be winners and losers. Europe is realizing it must take care of itself. It needs more onshore manufacturing. Defence stocks across the board have provided some of the best returns as defence spending necessarily goes up. So far there are more winners than losers around the world and that is, in part, why I think non-U.S. stocks have outpaced the U.S. over the past year.

So with a blank piece of paper, looking at the pluses and minuses, there are enough pluses that say the market should be supported. The question then comes down to the multiple. What is the market willing to pay for those earnings? I'd rather have it pay for good earnings than not.

U.S. markets have rallied in recent years, driven by strong earnings

Sources: Capital Group, MSCI, Standard and Poor's. Data shown is from June 30, 2019, through January 31, 2026. Magnificent Seven (Mag 7) represents a basket of mega-cap tech stocks consisting of Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA and Tesla. Defensives represent the consumer staples, energy, health care and utilities sectors in the MSCI USA Index. Cyclicals represent the consumer discretionary, communication services, financials, industrials, information technology, materials and real estate sectors in the MSCI USA Index.

Will non-U.S. stocks continue to outpace U.S. stocks?

For the last several years, the U.S. has had nearly twice the multiple as the rest of the world. I think that begins to balance out, both because earnings are catching up outside the U.S. and certainty in the investment horizon will be slightly better outside the U.S. It doesn't mean the U.S. market has to go down for the price/earnings multiple to come down. It just may not rise as much as earnings.

Two years ago, I remember sitting down, looking at the world, and trying to think how the U.S. could possibly be bumped out of its leadership role. I now know the answer to my question: It is a rewiring of the world trade and political order. Without judging that — without saying it’s good or bad — it’s a change, and it’s dramatic, and we're all sorting it out. But the U.S., so far, does not appear to be the main winner from that reordering. In 2026, I don't see anything that's going to start to change that. We'll have to see what happens with tariffs. But for now, U.S. policy uncertainty is reducing investment.

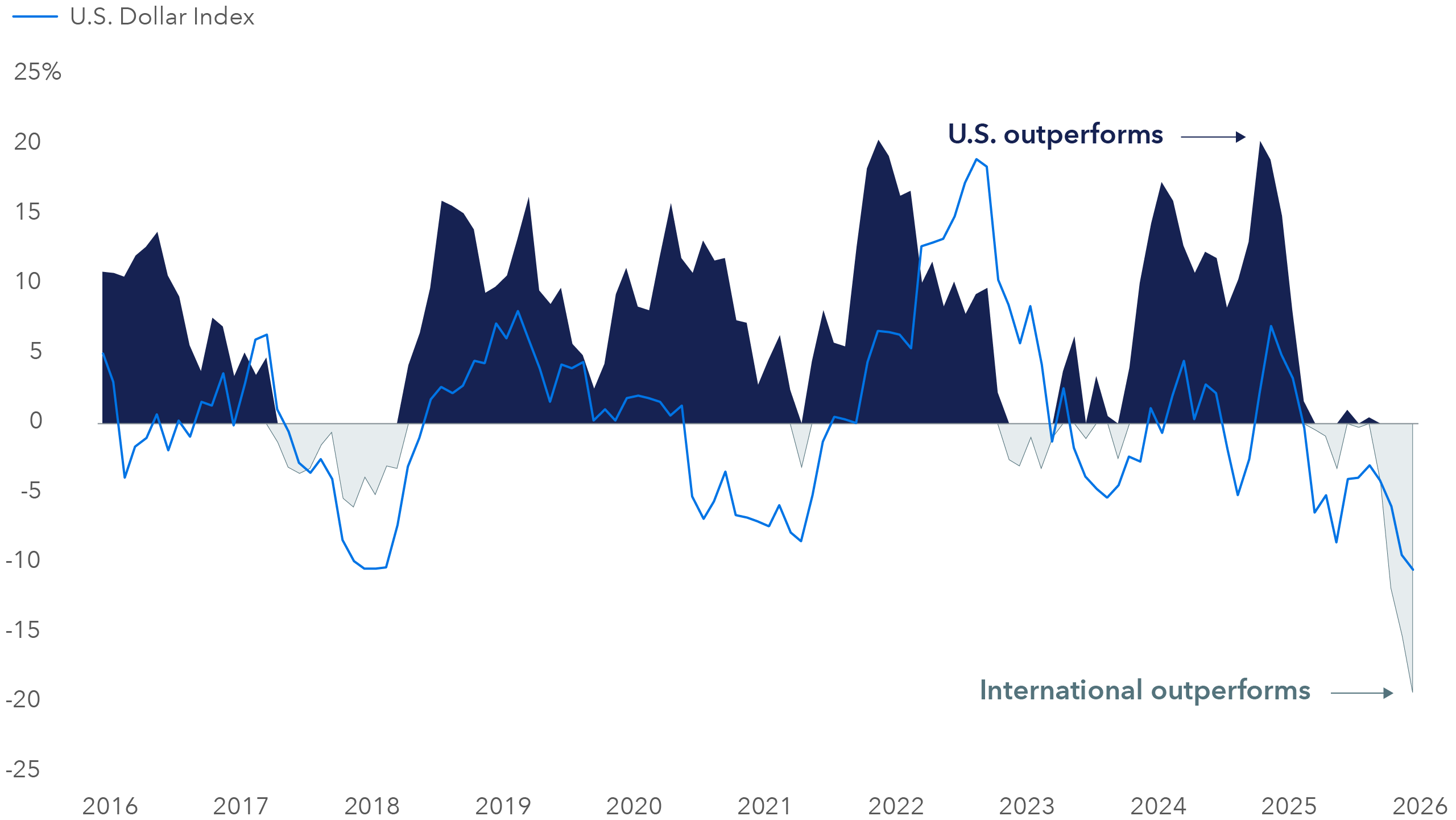

International stocks soared above U.S. markets last year

Sources: Capital Group, Intercontinental Exchange (ICE), MSCI, Standard & Poor's. U.S. relative returns are represented by the S&P 500 Index; international returns are represented by the MSCI All Country World ex USA Index. Relative returns are measured on a rolling one-year monthly total return basis in USD. As of January 31, 2026.

Which investment themes do you find compelling today?

I have to start with the caveat that I, and Capital Group in general, tend to invest at the company level. As you look across a portfolio you do begin to see themes, but I want to emphasize I am not a thematic investor. Most of the leadership companies, particularly in the U.S., are focused one way or another on technology. Some develop software. Others make hardware or computer chips. Some are a mix of the two. Some specialize in IT consulting. And then there's an ancillary group dedicated to building data centres, which require a lot of cooling and electricity. There's a whole series of companies I would refer to as the technology stack. That, no doubt, is the biggest theme we’ve been talking about and will continue to talk about.

AI tends to dominate the conversation but remember, AI is simply a piece of the stack. It can be the software that we interact with when we use Google, our smartphones, or any type of device to do a search. But behind that, there are algorithms being written, and they are running on hardware located at data centres. Those buildings require cooling systems and electricity. You can invest in all those different pieces of the stack. The theme isn’t just AI, it’s the growth and strength of the technology stack itself.

The AI opportunity set expands across the economy

Source: Capital Group. AI tech stack represents Capital Group’s interpretation of four layers of technology that enable AI to operate. Companies listed are examples of businesses that are among leaders of market share in each segment. TSMC is Taiwan Semiconductor Manufacturing Company. As of January 31, 2026.

A second theme we have focused on for a long time is health care and drug development. The health care sector matters a lot. We are now seeing the benefits of decades of work understanding DNA and how to develop new drugs. And we are just beginning to see the benefits of using AI in the drug discovery process, as well as other areas, such as accelerating the regulatory filing process.

Today, fewer than 5% of drugs under development are successful. That’s a terrible success rate. If AI can help identify earlier in the process which drugs are likely to fail and those more likely to succeed, we could potentially raise that success rate to 10%, which is still pretty terrible, but it's double the success rate we have now. That is likely to lead to an acceleration in drug discovery.

Health care stocks have come under pressure because of changes in the regulatory and pricing environment, but I don't think it changes the excitement we should have for an industry aiming to create more effective drugs that will help patients live better lives. We might even be getting closer to actual cures for certain diseases. Health is something we are all willing to invest in. Governments are also willing to invest in it. The money is there. It’s just a matter of finding its way to the right places.

A third theme I would mention — which was a surprise last year, but worth everyone’s attention — is financials. The rise in interest rates over the last few years benefited the financials sector. Not many other sectors celebrated it, but financials did. Financial institutions have been able to get back into the traditional banking market as lending rates increased. European banks particularly so due to more favourable interest rate and regulatory environments.

European banks beat the Magnificent 7 last year by a wide margin

Sources: Capital Group, FactSet, RIMES, MSCI, Standard & Poor’s. Returns reflect total returns in USD. Magnificent 7 (Mag 7) represents a basket of mega-cap tech stocks consisting of Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA and Tesla. As of December 31, 2025.

Are there any specific companies you find interesting?

One area that has my attention is technology consulting firms. They are considered AI roadkill because some people think we don't need coders anymore. We don't need anyone to come in and do the work. When we talk to these companies, our analysts are seeing that the business mix is shifting. The complexity of the business isn't getting any easier, and the complexity of AI isn't getting any easier. It's a real debate as to whether people will continue to outsource these services at the same level they did in the past.

CEOs are thinking they won’t be hiring as much in this area. But chief technology officers are more guarded, because they think we might just be hiring different types of consultants to help with this new technology. As of right now, I haven't seen anyone spend less money in this area. The overall theme is that hiring in the U.S. and around in the world may plateau for the next few years as AI works its way through the system. I think every company is adjusting with that in mind. My instinct is that the complexity of this work is going to shift somewhere else. We will need to hire people to do that other thing. And the savings from AI will be a fraction of what everyone is predicting.

Don’t get me wrong, I think AI will make us more efficient. But I think the actual financial savings of less head count or less technology spending — I just don't see that happening. I don't know if that's going to play out based on the most negative scenario. And, right now, these companies are definitely pricing in the most negative scenario. We’ve been doing a lot of work on Accenture and CapGemini. Both companies are already well positioned in the world. They're adjusting, learning and working with their partners to figure out how to be the right companies going forward.

As a former mining analyst, what are your thoughts on rising gold prices?

I learned early on as a mining analyst that there is about a 10-year cycle for metals and mining stocks. So what's led to the recent spike? There are base metals, such as copper and zinc. Then there are rare earth metals that are used in microchips. And then there are precious metals. Each one of those is a very different thing. Base metals tend to be about infrastructure and construction. Copper is used in wiring, for instance. So that's why copper and certain other metals are going up, but they're not as dramatic as the precious metals.

The rare earth metals are hard to find. While there are plenty out there, they're expensive and messy to extract. For a long time the U.S. decided to let other countries mine those materials. Now that everyone is worried about controlling the sources of these metals, we're trying to figure out how to bring the process back on shore. The precious metals used in technology — gold, silver, platinum, palladium — are a store of wealth. Their prices have risen the most over the past year.

Gold and silver prices have surged in recent months

Sources: Capital Group, ICE Benchmark Administration, LBMA, Standard & Poor's. Industrial metals refers to the S&P GSCI Industrial Metals Index. Silver, gold and copper prices reflect daily spot rates. As of January 31, 2026.

With uncertainty about economic policies and inflation, there is a desire by investors to diversify portfolios into hard assets. That can be real estate, but it can also be things like gold and silver. As a geologist, I do find it fascinating that we spend so much time and effort to dig up a metal, refine it and move it, only to put it back underground and put a guard on it. That is its main purpose, but that's a separate story. What we’ve seen is a reaction in the precious metals pricing to scarcity value, a desire for hard assets, and concerns about fiat currency.

What lessons have you learned in 40 years of investing?

Well, there's certainly no shaking my faith that bottom-up fundamental research, focusing on a longer time horizon, and active management make a difference. These are the core principles we hold at Capital Group.

On a personal note, I have learned that sleep matters. So be sure to get sufficient sleep. I think especially my younger colleagues think they’ll somehow get to catch up on sleep in the future. The science is pretty compelling — that’s not the case. And being kind is something I've learned is worth the effort over my 40-year career.

Learn more about

Fiat currency is a national currency that is not pegged to the price of a commodity such as gold or silver.

The London Bullion Market Association (LBMA) is the international trade association that represents the over the counter (OTC) gold and silver bullion market. This market encompasses trading and refining physical precious metals, primarily gold and silver, but also extends to other precious metals like platinum and palladium.

MSCI USA Index is a free float-adjusted, market capitalization-weighted index designed to measure the performance of the large- and mid-cap segments of the U.S. market.

MSCI All Country World ex USA Index is a free float-adjusted, market capitalization-weighted index designed to measure equity market results in the global developed and emerging markets, excluding the United States. The index consists of more than 40 developed and emerging market country indices.

MSCI Europe Banks Index is composed of large- and mid-cap stocks across Developed Markets countries in Europe. All securities in the index are classified in the Banks industry group (within the financials sector) according to the Global Industry Classification Standards (GICS®).

U.S. Dollar Index is a measure of the value of the U.S. dollar relative to the value of a basket of currencies of the majority of the U.S.'s most significant trading partners.

S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

S&P GSCI Industrial Metals Index provides investors with a reliable and publicly available benchmark for investment performance in the industrial metals market.

The S&P 500 Index and S&P GSCI Metals Index are products of S&P Dow Jones Indices LLC and/or its affiliates and have been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

Our latest insights

RELATED INSIGHTS

-

Global Equities

-

-

Economic Indicators

Commissions, trailing commissions, management fees and expenses all may be associated with investments in investment funds. Please read the prospectus before investing. Investment funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. For investment funds other than money market funds, their values change frequently. For money market funds, there can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian investment funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2026. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.