Market Volatility

Categories

Dividends

Meta shifts the narrative on dividends in the world of Big Tech

Chris Buchbinder

Chris Buchbinder

Marc Nabi

Marc Nabi

Jacob Gerber

Jacob Gerber

May 15, 2024

Meta’s dividend initiation this year appears to have changed the payout paradigm for Big Tech companies. Soon after, Alphabet and Salesforce followed suit, announcing dividends for the first time.

Investors have historically balked at dividends as a sign of declining growth prospects. That was the signal that investors sent when Microsoft first announced its dividend in 2003. But Meta appears to have successfully changed that narrative. The stock went up 23% following the announcement, accruing almost US$200 billion in market cap.

The distinguishing feature today is that the larger cap tech companies have buttressed balance sheets, strong earnings, reasonable valuations and what may be the beginning of an AI megacycle that will require massive amounts of capital expenditure. In this context, the introduction of dividends by both Meta and Alphabet is viewed as a sign of capital discipline and confidence in earnings sustainability.

Big Tech’s foray into dividends

Meta and Alphabet will still spend billions on AI infrastructure. Dividends come after aggressive cost cutting and realignment of resources by many large tech companies. Along with Salesforce’s first-ever dividend of 40 cents per share, total dividend payments from the companies could amount to about US$4.2 billion on a quarterly basis.

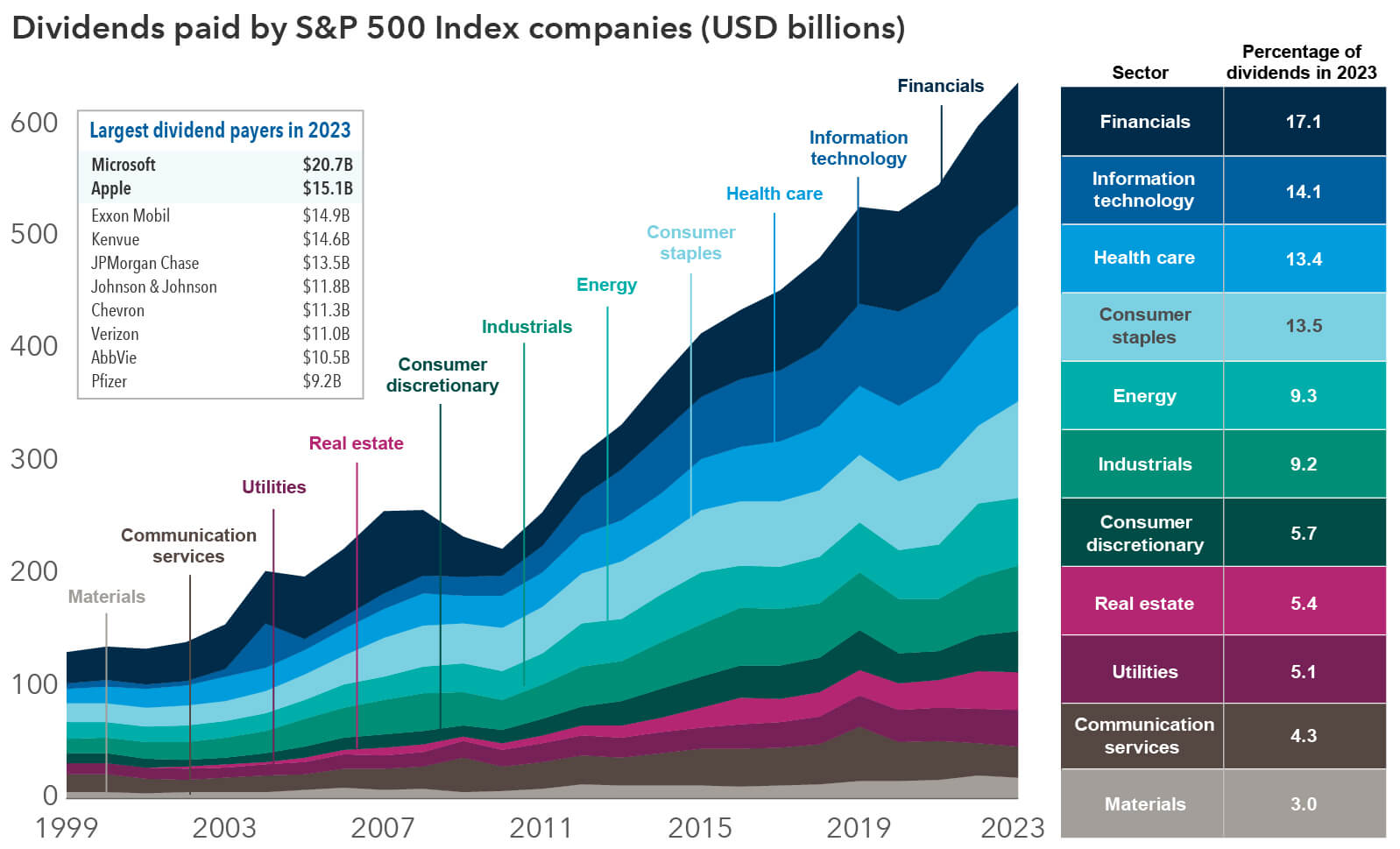

Tech’s share of dividends is growing

Sources: FactSet, Capital Group. Data from 1999 to 2023.

While dividend-focused investors may not be thrilled with Meta's low dividend of 50 cents per share and dividend yield of 0.4% or Alphabet’s annual dividend of 80 cents and yield of 0.5%, the sheer scale shows substantial payments: US$5.1 billion for Meta and US$10 billion for Alphabet. And the dividends will likely grow over time, as has been the case with other tech firms. Microsoft's dividend has consistently increased since 2003. Apple initiated its dividend in 2012 and has raised quarterly payouts for 12 straight years.

Tech firms have traditionally leaned on share buybacks, and these will likely continue to be a core part of their overall capital allocation framework. For example, Apple recently announced plans for a record buyback of US$110 billion of stock, while Meta authorized a buyback of US$50 billion. But an increasing number of tech firms are recognizing that dividends can prove management’s commitment to shareholder returns. Companies are loath to cut their dividends, as it sends a negative signal to investors and often leads to a decline in share price. Furthermore, the dividend is a way the technology giants can potentially expand their base beyond growth-oriented investors.

As tech firms have grown in market cap, the information technology sector has become a bigger part of the overall dividend equation for U.S. stocks. Technology companies ranked as the second-largest contributors to S&P 500 dividends, behind the financial sector and traditional dividend-paying areas of the market, such as health care and consumer staples.

Notably, 37 of the 65 technology companies in the S&P 500 Index pay a dividend. That’s more than half, which also means that there is room for tech companies to grow dividends further. Five of the Magnificent Seven stocks now pay dividends.

Looking beyond tech firms, dividends are growing across industries

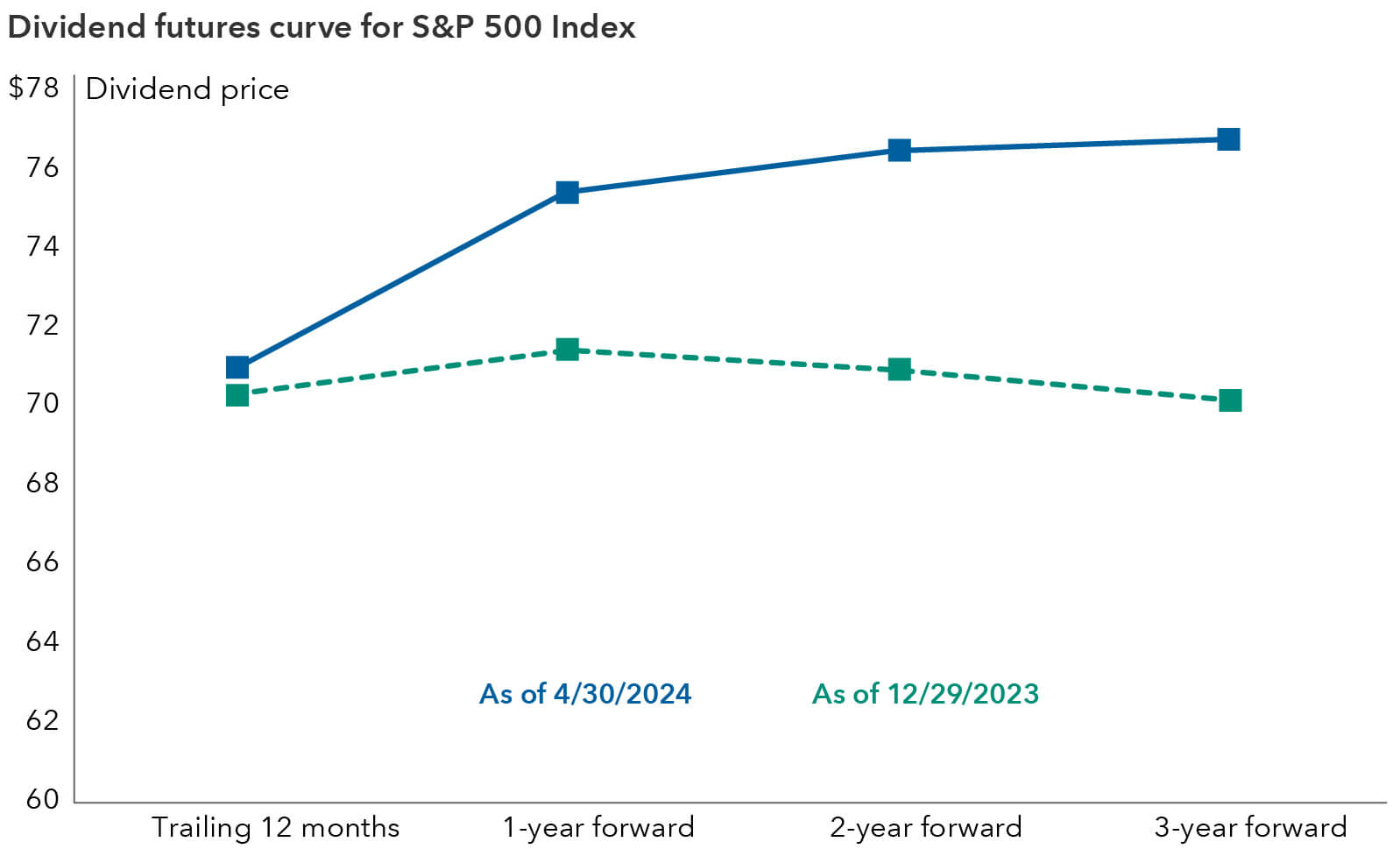

Given rising cash flows and expectations of earnings growth for U.S. equities, the outlook for dividend payers is brightening. The S&P 500 is expected to post a 6% increase in payments for 2024, compared to its 5% increase in 2023, according to S&P Dow Jones Indices data.

The dividend futures pricing curve is also significant as market expectations have increased following Meta’s and Alphabet’s announcements. The slope of the curve has steepened and can be used to represent expected dividend growth overtime, in this case, for the current year.

Tech brightens outlook for S&P 500 dividends

Sources: Capital Group, Bloomberg. Data includes trailing 12-months, 1-year forward, two-year forward, and 3-year forward dividend futures prices as of April 30, 2024. Based in USD.

Dividends are being initiated and restored in many industries. As free cash flows rise on corporate balance sheets, many companies are increasing their payouts or reinstating dividends. Aerospace, airline and cruise companies were among industries that conserved cash during the COVID-19 travel slump and are now shifting gears as global travel rebounds.

Ryanair, for example, announced its first-ever dividend in 2023 after a rebound in profit and a brighter forecast. Booking.com also initiated a dividend, citing earnings and free cash flow strength. Delta Air Lines reinstated its dividend after suspending it during the pandemic. General Electric, which makes and services jet engines, recently boosted its dividend.

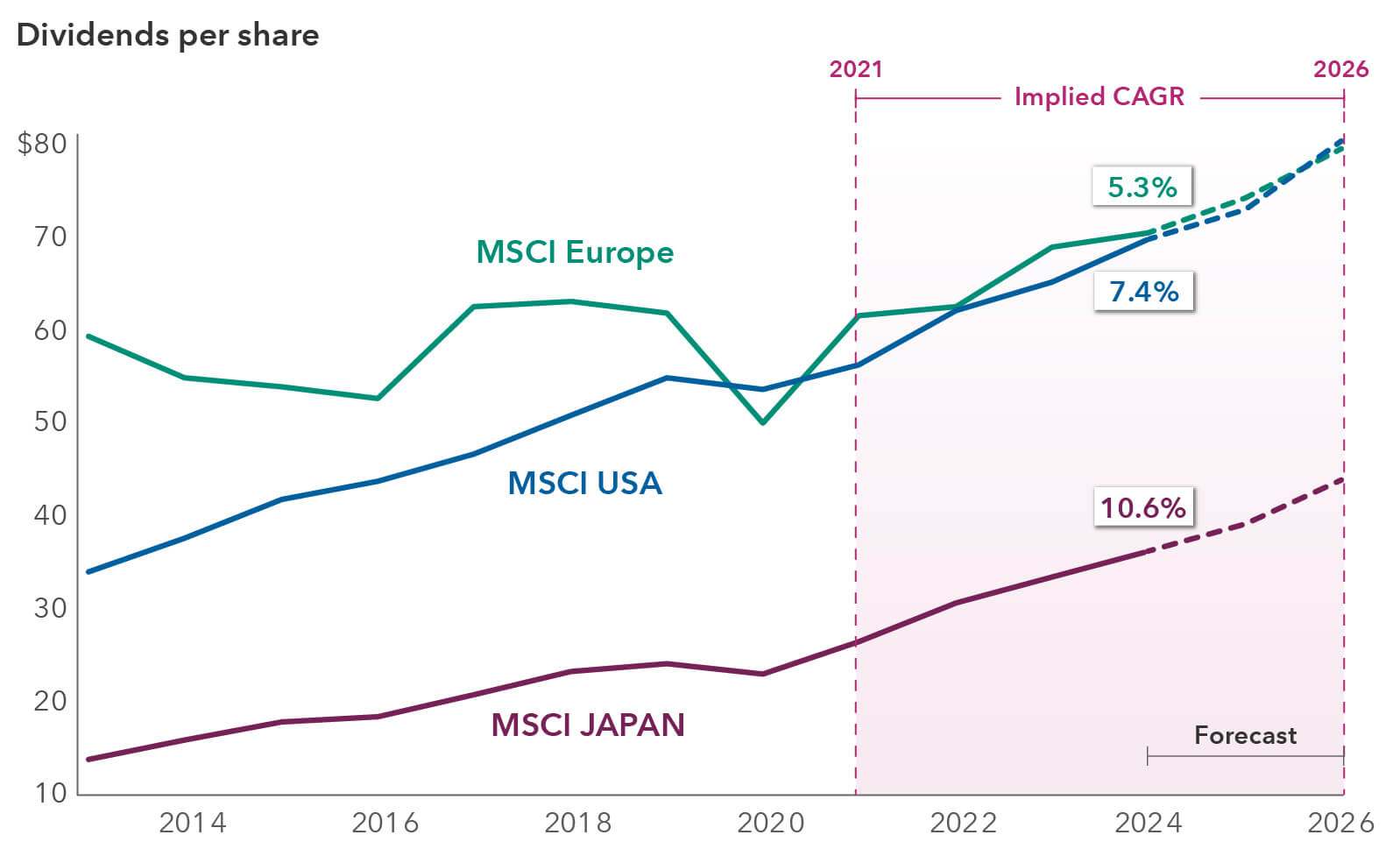

Dividends are growing globally. European banks Santander, Deutsche Bank, UniCredit and BNP Paribas have also elected to raise dividends in 2024.

Global dividends are expected to grow

Source: FactSet. Data from 2013 to 2023, with 2024 through 2026 based on consensus estimates as of April 24, 2024. CAGR = compound annual growth rate. Based in USD.

Energy giants such as ExxonMobil and Canadian Natural Resources have maintained a steady base of investors amid volatile oil prices by maintaining and growing their dividend for over 20 years. Some exploration & production companies have opted to incorporate variable or special dividends in addition to their base payouts as they manage cash flow levels given fluctuations in commodity prices.

Bottom line

Dividends benefit management in several ways. First, they can widen a company’s shareholder base. Having more investors can reduce stock volatility by accommodating both growth and dividend income investors. Second, many employees at technology and innovation companies receive shares as compensation. Consequently, a dividend can be seen as an indirect pay raise and boost employee morale.

Over the past 12 months, we have seen signs that the U.S. equity market has broadened beyond a highly concentrated group of stocks, and traditional dividend payers have been garnering more attention. Dividend stocks have the potential to ride out market volatility, along with elevated interest rates.

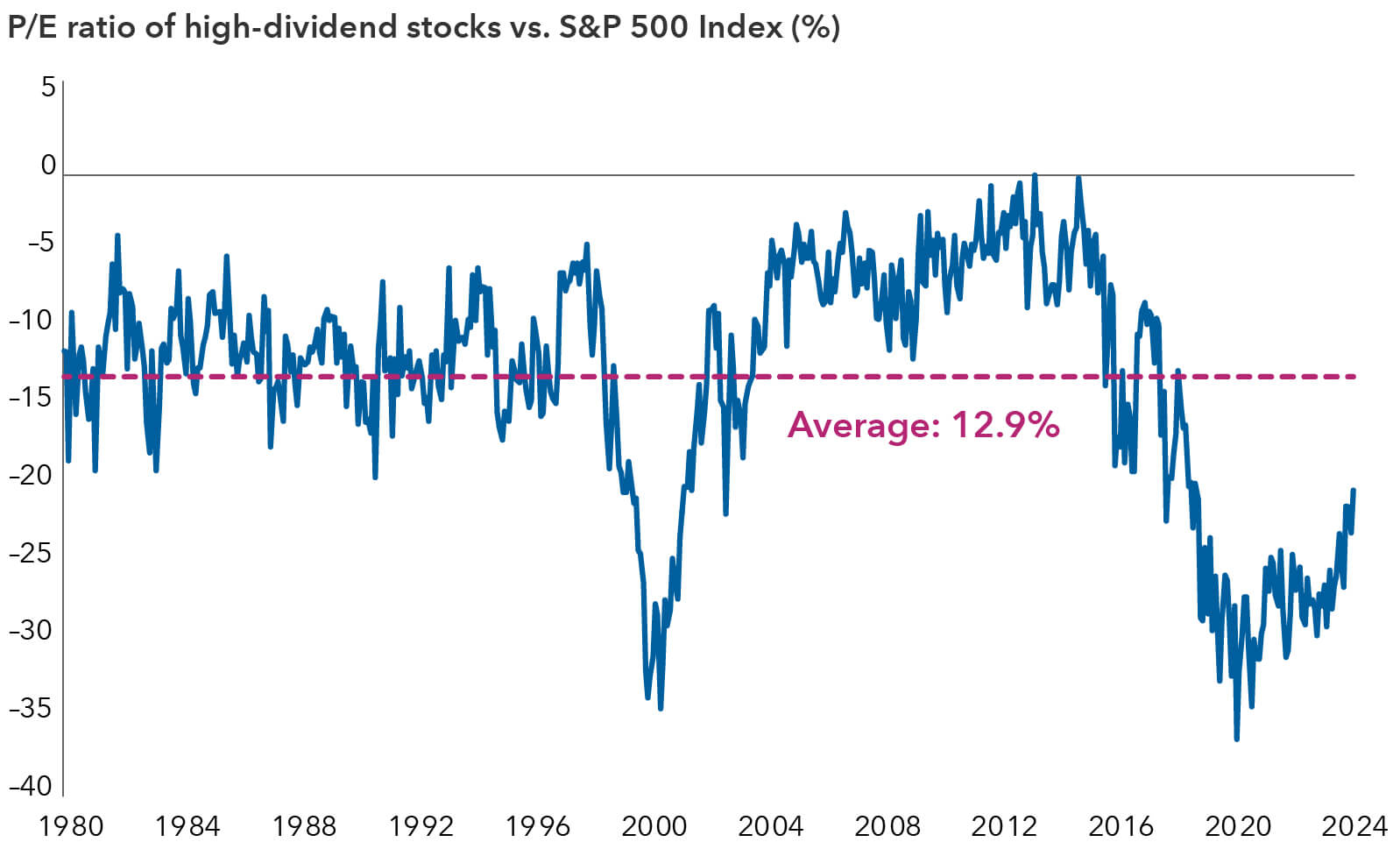

It’s possible that dividend-paying companies may see a valuation re-rating. The P/E ratio of high-dividend stocks versus the S&P 500 has lagged, though the ratio is gradually improving.

Dividend payers present opportunities

Source: Goldman Sachs. Data as of March 31, 2024. P/E ratio = price-to-earnings ratio. Past results are not predictive of results in future periods. This chart examines the P/E multiple of the cohort of stocks in the S&P 500 Index with the highest quintile dividend yield (sector-neutral) relative to the broader S&P 500.

If the U.S. Federal Reserve eventually cuts interest rates, it could also be a catalyst for higher yielding dividend stocks. While a large portion of the nearly US$6 trillion in cash sitting on the sidelines may move to fixed income, declining interest rates coupled with a more resilient economic environment could also increase investor demand for these stocks.

Learn more about

Chris Buchbinder is a portfolio manager for Capital Group U.S. Equity Fund (Canada).

The MSCI Japan Index is designed to measure the performance of the large- and mid-cap segments of the Japanese market.

The MSCI USA Index is designed to measure the performance of the large- and mid-cap segments of the US market

The MSCI Europe Index captures large- and mid-cap representation across 15 developed markets (DM) countries in Europe.

S&P 500 Index is a market-capitalization-weighted index based on the results of 500 widely-held common stocks.

The price-to-earnings (P/E) ratio measures a company's share price relative to its earnings per share (EPS).

The Magnificent Seven are a group of large and influential technology and consumer discretionary stocks: Alphabet, Amazon, Apple, Microsoft, Nvidia, Meta and Tesla.

Our latest insights

-

-

Market Volatility

-

-

Currencies

-

Market Volatility

RELATED INSIGHTS

Commissions, trailing commissions, management fees and expenses all may be associated with investments in investment funds. Please read the prospectus before investing. Investment funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. For investment funds other than money market funds, their values change frequently. For money market funds, there can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian investment funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2026. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.