Retirement Planning

Do you live in the right state for retirement?

Michael Schmid

Michael Schmid

April 28, 2026

Across the country, states are debating new ways to tax wealth. In California, voters are weighing a contentious one-time “billionaire tax.” In Hawaii, a measure to tax those with more than $20 million in assets hangs in the balance. Rhode Island’s governor recently proposed a new tax on state income topping $1 million. Even when proposals stall, the broad trend is clear: Policymakers are looking closely at the assets of high net worth households.

For many wealthy investors, especially those nearing retirement, one question quickly follows: Am I living in the right state?

Clients frequently ask whether relocating could reduce taxes on a future windfall, such as the sale of a large company stock position, the exercise of stock options or another liquidity event that may coincide with retirement.

On the surface, the idea seems straightforward: Move to a lower-tax state and keep more of what you’ve earned. In practice, it’s rarely that simple. When we talk through this question with clients, taxes are only the starting point. A move can have wide-ranging financial, legal and personal implications. Determining whether it truly makes sense requires looking well beyond a single state’s tax rate.

Liquidity events often start the conversation.

For many clients, the idea of moving states surfaces when a large taxable event is approaching. States tax income very differently, and the gap can be meaningful when a large transaction is involved.

But once we start talking, the discussion usually expands beyond tax rates. Why are they considering the move in the first place? Are there family ties in the potential new state? Do they plan to maintain a residence or other connections to where they currently live?

These questions matter, particularly for residents of high-tax states such as California, where authorities closely examine whether someone who claims to have moved has truly done so. Maintaining significant ties to the state can complicate that determination.

In many cases, these conversations ultimately lead to a recommendation that clients consult with an attorney who specializes in residency issues. We can connect you with professionals who understand the legal and practical requirements of establishing residency in a new state.

Considering taxes beyond income tax.

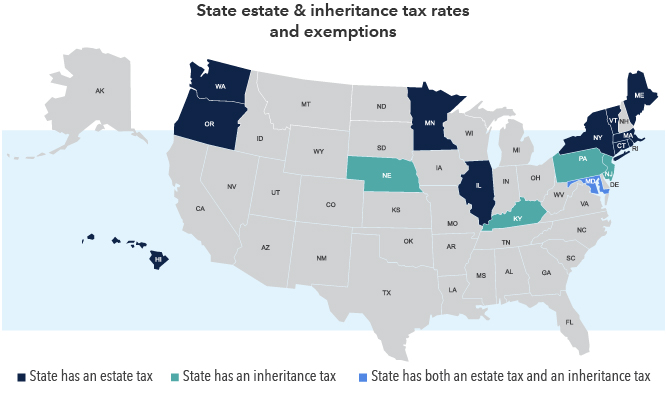

Income taxes tend to dominate these discussions at first, but they’re only part of the picture. State estate or inheritance taxes can also vary widely. Some states impose their own estate taxes with relatively low exemption thresholds, while others have none at all. For families thinking about multigenerational wealth planning, those differences can be significant.

Retirement income itself may also be treated differently depending on where you live. For example, Illinois, Iowa, Mississippi and Pennsylvania all have state income taxes, but exempt most retirement plan distributions (including Social Security benefits) from those taxes. More broadly, over 40 states do not tax Social Security benefits, including California and New York.

These nuances mean that two states with similar income tax rates may ultimately produce very different outcomes for retirees.

Cutting ties can be a major undertaking.

One of the most common misconceptions about moving states for tax reasons is that it simply comes down to where you spend the most time. Time spent in each location is certainly a factor, but it’s rarely the only one. States evaluating residency can look closely at many aspects of a person’s life. That might include where their primary home is located, where their doctors and dentists practice, where their children attend school and where close family members live.

In some cases, investigators may even examine the logistics of the move itself. One story I’ve heard involved officials asking whether a moving truck had actually arrived to transport a taxpayer’s belongings.

The point isn’t that every move will be scrutinized this way. But states with higher tax rates are well aware that some residents may attempt to relocate ahead of a large taxable event, and they want to ensure that the move is genuine. For that reason, properly establishing residency in a new state can require careful planning and documentation — another reason legal guidance is important.

Beyond taxes, do you have a reason to move?

Relocating, especially in retirement, is a significant life decision. It can mean leaving behind a longtime home, social network and community.

In my experience, those who ultimately follow through with a move often have motivations that extend beyond financial considerations. They may want to be closer to children or grandchildren, spend more time in a place where they’ve long enjoyed vacationing or reconnect with another region where they’ve previously lived. Those personal ties can make a transition feel sustainable over the long run.

Ultimately, while taxes can influence where you live, retirement itself is about much more than the tax bill. The goal is to find a place that supports both your financial goals and your quality of life.

Explore topics

Related insights

-

-

U.S. Federal Reserve

-

Economic Indicators