Energy

The new era of energy as a geopolitical instrument

Talha Khan

Talha Khan

April 28, 2026

It’s no surprise that energy has long occupied a central position in the global economy, with governments jockeying for ready access and favorable pricing in the oil and natural gas markets. But a host of recent events, most notably the war in Iran, shows that energy is now playing a profound role on an even bigger stage — the world of geopolitics.

Beyond its traditional job as an economic asset, energy is being deliberately deployed as an instrument of statecraft. From Russia’s curtailment of gas flows into Europe to the West’s sanctions on Russian oil, and from recurring instability in the Middle East to alarm over China’s dominance in critical minerals, energy is no longer simply shaping the global economy. It’s being wielded as a strategic tool to shape political outcomes.

This marks a shift from the episodic supply shocks of the past to something more structural. In today’s fragmented geopolitical landscape, energy is being harnessed to influence trade, coerce rivals, rewire supply chains and, in the case of Iran, try to fend off a military action by far more powerful rivals.

This year alone, the intervention in Venezuela’s oil sector and intense U.S. focus on resource-rich territories such as Greenland brought the dynamic to the fore. Control over energy is now being pursued more directly, and more assertively, than at any point in recent decades.

Taken together, these moves underscore a new chapter of aggressive foreign policy. Numerous countries are making big plays to advance their agendas, and view the control and distribution of oil and gas as elemental tools at their disposal.

For investors, the implications are significant. Energy and commodities may experience sustained higher prices and volatility. Companies tied to infrastructure and energy security could see stronger demand. On the other hand, sectors that depend heavily on cheap energy or smooth global trade may face persistent cost pressures.

Energy has become a key tool of geopolitical pressure.

Interestingly, the primary goal of modern energy policies isn’t always to redress near-terms problems such as abrupt supply shocks. In several cases, the U.S. has pursued control over resources and supply chains even where immediate gains would be limited. The U.S. focus on Greenland is a case in point. Pursuing control of the island was both an effort to secure a strategic Arctic corridor and to position for future access to critical minerals such as uranium, iron and potentially untapped oil and gas reserves.

A similar logic applied in Venezuela, where intervention was a long-term play for supply rather than a near-term fix. The country holds some of the world’s largest oil reserves, but years of underinvestment have limited its production capacity. Meaningfully increasing barrels brought to market would require sustained capital and time.

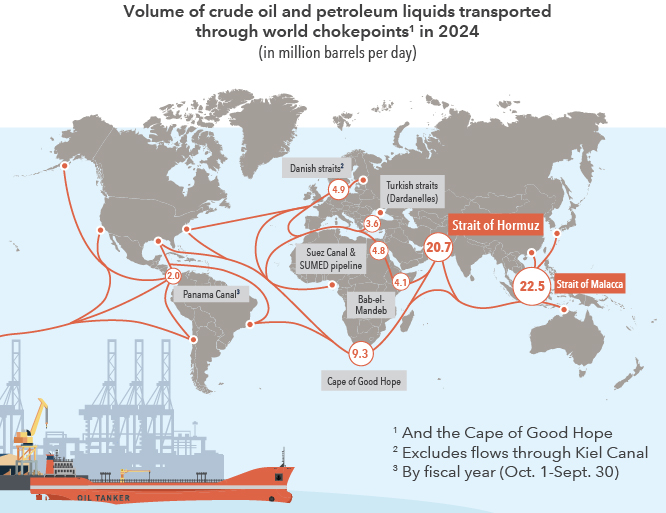

The war in Iran, by contrast, illustrated the most immediate and forceful version of energy leverage. Iran retaliated against the U.S. and Israel by drastically restricting traffic through the Strait of Hormuz, interrupting key flows of oil and gas and triggering a major spike in global oil prices. The sustained bottleneck gave Iran leverage against two of the world’s most technologically advanced military powers, and the ripple effects of massive trade disruption continue to domino.

One thing is clear: the Iran war is not simply about military capability — it’s about control over energy flows and transit routes. Long-lasting Iranian control over the Strait of Hormuz would alter the geopolitical balance in the region. Not surprisingly, markets reacted sharply to the reality of constrained flows, and that reaction is the point..

Energy markets will likely experience higher prices and more volatility.

For markets, this does not imply a world of constant crisis, nor does it suggest permanent or unconstrained “weaponization” of energy. These tools are costly and, in many cases, limiting. But the clear message is that politics is now a more central part of how energy markets work.

That has a clear implication: energy prices are likely to stay higher on average, with a so-called risk premium baked in — essentially, an extra cost reflecting the chance of disruption.

Markets are already adapting. Trade flows are being rerouted, companies are investing more cautiously and there’s a growing emphasis on shoring up supply chains rather than simply minimizing costs. That means a tradeoff, as systems that are more reliable are often more expensive.

And even after tensions ease, the pre-shock dynamic is unlikely to snap back into place. The global economy keeps functioning, but at a higher cost and with more friction.

Iran provides an example. Regardless of the long-term outcome of this crisis, I believe the damage to confidence won’t immediately disappear. Shipping routes have already adjusted, insurance costs have risen and confidence in key transit corridors has been compromised. Once a route or region undergoes such upheaval, that perception tends to stick.

All of this points to a broader transition. The world economy is growing more fragmented, national security is trumping efficiency and economic statecraft is becoming normalized. Energy sits at the center of this shift, linking politics and economics in ways that are hard to ignore.

Explore topics

Related insights

-

-

U.S. Federal Reserve

-

Economic Indicators