Markets & Research

The electrification opportunity extends beyond data center hype

Carol Cuello

Carol Cuello

May 5, 2026

For many years, electricity wasn’t exactly a front-and-center topic, either in American living rooms or in the investment world. That’s changed of late as artificial intelligence (AI), hyperscale computing and cloud infrastructure have caused an immense surge in demand. This is most evident in the rise of data centers and projections of dramatically growing energy usage.

But another significant shift is taking shape more quietly: industrial electrification. This involves transitioning existing industrial energy uses powered by fossil fuel sources to electric alternatives. While slower and less visible than anything AI-related, it represents a large and long-duration opportunity. And within that, what’s known as process heat — the boilers, furnaces and kilns behind everything from steel to food production — represents a core opportunity.

Unlike the demand tied to data centers, electrifying existing technology is gradual — a steady cycle of equipment replacements, retrofits and new builds. The slower pace can make the opportunity easy to overlook. But over time, incremental changes are poised to add up, expanding demand across a broad base of the economy.

Indeed, this sort of electrification is already pushing forward with no signs of stopping. Countries are looking to reduce reliance on imported fossil fuels, particularly as energy markets remain volatile. Policymakers have introduced incentives to boost the economics of electric technologies. And ongoing investment in power generation and grid infrastructure is gradually making electrification more feasible.

I foresee beneficiaries of this trend beyond the companies adopting the technologies. Manufacturers of electrification technologies such as heat pumps, electric boilers and arc furnaces are likely to gain as industrial systems begin to turn over. Electrical equipment providers — such as ABB, Schneider Electric, Siemens and Eaton — are also well-positioned, as they supply the systems used to manage industrial power loads and upgrade grid infrastructure. Utilities stand to be another pick-and-shovel beneficiary. As industrial processes shift toward electricity, they could experience sustained growth.

Process heat conversion is a core electrification opportunity.

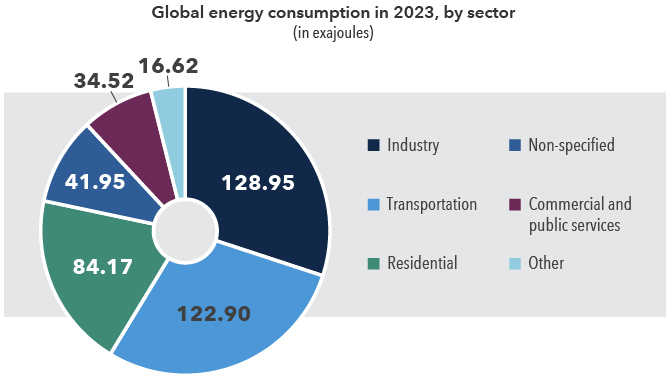

I believe that process heat conversion is the largest opportunity. Industry accounts for roughly a third of global energy consumption, and process heat makes up the majority of that, most of which is still reliant on fossil fuels.

Adoption across different sectors has been unfolding at dramatically different paces. The big dividing line? Temperature.

Low and medium temperature applications are moving first, where electric boilers and heat pumps can deliver low-cost alternatives to combustion-based equipment. The food and beverage sector has started adopting technologies such as heat pumps, since most processes operate below roughly 200°C.

Moreover, the foundation is being laid for a secular shift in steelmaking. Although near-term hurdles exist, the combination of tightening European regulations and evolving carbon pricing suggests that electrification will play an increasingly central role in future industrial replacement cycles. Facilities are moving away from coal-based blast furnaces toward electric arc furnaces that use scrap or direct-reduced iron. Similar trends are taking shape in general manufacturing.

Industry is the largest source of global energy demand

Sources: International Energy Agency (IEA). Survey period: 2023. Figures were rounded.

Conversely, the technologies needed to electrify higher temperature processes are still prohibitively expensive for most businesses. Cement production, for example, requires temperatures above 1,000°C, which are not easily achieved with current electric technologies. Chemical production, which includes industrial gases and fertilizers, also needs high temperatures. New, cost-effective high-heat technologies, such as electrified steam methane reforming (e-SMR) are still in early development.

Despite this, it’s important to remember the sheer size of industry as a whole. Even slow and steady electrification gains over decades can produce significant electricity demand, supporting durable growth for many sectors in the years to come.

Why adoption has been slow, so far.

The scale of the opportunity raises a natural question: why hasn’t industrial electrification moved faster?

Cost remains a primary constraint. Electrifying industrial heat is often more expensive than maintaining existing fossil-fuel systems. Where electricity is cost-competitive with fossil fuels, adoption tends to accelerate.

In addition, natural replacement cycles will dictate the pace of change. Industrial companies rarely rip out working equipment early, locking in fuel choices over long horizons. For example, a gas boiler at a manufacturing plant can operate for close to 40 years.

Grid capacity is another limiting factor. Power systems globally were not built to accommodate a large-scale shift in industrial load. Expanding transmission and distribution networks takes time, and in many regions, that work is still in its early stages.

Government policy is an important lever.

Policy helps set the pace of adoption, more so than for many other sectors. Right now, Europe has the most progressive global electrification policies. Decarbonization targets and carbon pricing frameworks are already influencing corporate and public investment decisions. In coming months, the European Commission is scheduled to announce an action plan, which is expected to provide signals for how officials plan to address grid constraints and cost barriers to electricity adoption.

In the United States, progress has been more fragmented. There is no national electrification strategy, and adoption is largely driven at the state level. This has led to pockets of activity, but less consistency across regions, particularly in heavy industry.

Over the past decade, China has experienced faster electrification than Europe and the U.S., driven less by policy and more by alignment with broader industrial and clean energy priorities. Efforts to improve air quality, reduce emissions and modernize industrial capacity have collectively supported the shift toward electricity, even without a nationwide electrification mandate.

While slower and less visible, industrial electrification represents a long-term opportunity within broader electrification trends. Electrifying existing processes will take time, unfolding alongside replacement cycles and grid investment rather than all at once. Even so, across such a large share of global energy use, incremental change can carry significant weight.

Explore topics

Related insights

-

-

U.S. Federal Reserve

-

Economic Indicators