Global Affairs

U.S. Equities

A new chapter for luxury

Julie Wang Chou

Julie Wang Chou

July 1, 2026

In early 2021, it seemed that luxury brands could do no wrong. Flush with pandemic-era stimulus checks that couldn’t be spent on vacations or dining, consumers redirected their money, in force, toward designer handbags, watches and jewelry. The beneficiaries were some of the world’s most recognizable luxury houses, whose sales and valuations soared to unprecedented heights.

But as economies reopened, luxury lost some of its shine. Consumers spent more on travel and experiences. Inflation squeezed discretionary budgets. China’s economy slowed. The exuberance that had defined the industry began to fade, compressing valuations and sending luxury stocks into a prolonged — and quite painful — correction.

Markets, however, can be very attractive after expectations have been reset. I believe the luxury sector may be approaching that point.

The industry’s challenges have not disappeared: consumer spending remains uneven and geopolitical uncertainty persists. Yet beneath those headlines, several important trends are moving in a compelling direction. Demand in key markets, particularly the United States and China, has been gradually improving. A wave of new creative leadership has injected fresh energy into many of the industry’s most important brands. And after years of disappointing stock-price returns, valuations have fallen to levels that more appropriately reflect underlying fundamentals.

Expectations for the market have recalibrated.

The opportunity today is not simply that valuations are lower. Expectations are lower as well.

The pandemic created the conditions for an extraordinary period of growth for luxury retail, and companies became valued as though that momentum would continue. That assumption made us cautious. Now, many brands are being measured against a period of relatively weak performance, creating a more achievable backdrop for earnings growth.

Equally important, the businesses themselves remain strong. The leading luxury houses possess global brands, pricing power, high margins and customer bases that competitors struggle to replicate.

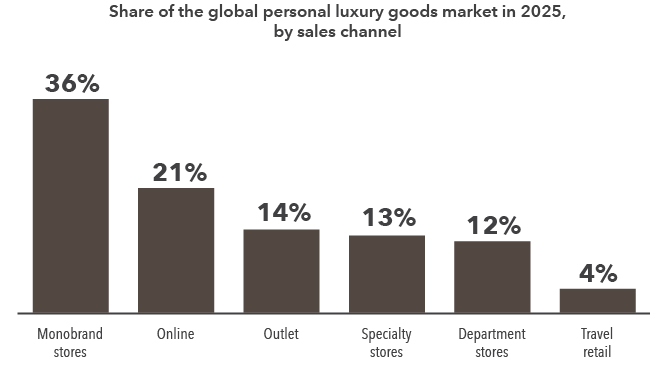

Exclusive brand stores remain the primary retail channels

Source: Worldwide. Bain & Company. As of 2025.

Additionally, brands have started to become more disciplined in pricing their products. During the boom, many luxury companies pushed prices aggressively higher, confident that demand would absorb the increases, and the results were dramatic: A Chanel Classic Flap handbag that sold for roughly $5,800 in 2019 now costs approximately $11,800. Across the industry, price hikes helped drive revenue growth, but they were also rooted in a broader assumption that the good times would continue indefinitely.

Today, the industry appears more focused on sustainable growth than it was during those peak years. Many companies are paying closer attention to perceived value and consumer affordability, particularly among aspirational customers who were priced out. In some cases, brands are expanding entry-level offerings to reconnect with those consumers while preserving the prestige of core franchises. The challenge is broadening access without compromising the exclusivity that underpins luxury’s appeal.

The U.S. is reemerging as a growth engine.

For much of the past two decades, luxury companies viewed China as the industry’s primary growth engine. While the country remains indispensable, the balance is beginning to shift.

Many luxury brands are devoting greater attention to the U.S., where wealth creation has remained remarkably strong and consumer spending has proven more resilient than expected.

This year, three key fashion houses staged high-profile events on American soil, underscoring the strategic importance of the market. In May, Gucci transformed Times Square into a celebrity-packed runway spectacle, Dior presented its collection at the Los Angeles County Museum of Art and Louis Vuitton showcased at New York’s famed Frick Collection. Fashion shows in New York and L.A. aren’t new, but the scale of these investments suggests brands are investing more in their U.S. presence.

Consumer preferences also vary meaningfully across regions. Chinese shoppers have become increasingly selective and discerning, often prioritizing craftsmanship, exclusivity and product originality. American consumers, particularly those entering luxury for the first time, tend to gravitate toward a brand’s most recognizable products, such as the handbags, accessories and logos that function as visible markers of status and identity.

Understanding those distinctions has become increasingly important as luxury companies pursue growth across multiple markets.

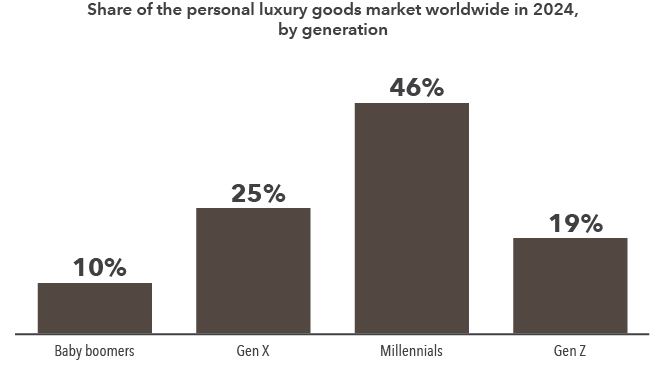

Younger generations are playing an important role in the luxury market

Source: Worldwide. Bain & Company. As of 2024.

New creative energy is bringing excitement to the industry.

One of the most significant developments in fashion over the past two years has been the widespread reshuffling of creative leadership across major houses. An unusually large number of brands have appointed new creative directors, creating a wave of anticipation around debut collections.

At the same time, aesthetic preferences appear to be shifting, with the era of “quiet luxury” showing signs of fatigue. In its place, many brands are returning to more distinctive, recognizable designs and products that clearly communicate brand identity.

Early results have been encouraging. Several recent launches have been well received, helping generate excitement at a moment when the industry needs renewed momentum.

For investors, the significance extends beyond trends and fashion shows. New creative leadership can reinvigorate brand relevance and attract new customers. When paired with improving demand and significantly lower expectations, the backdrop looks increasingly favorable for long-term investment. Luxury retail may not return to the extraordinary conditions of 2021, but after years of correction and recalibration, that is precisely what makes the opportunity attractive today.

Explore topics