Global Equities

Categories

Global Equities

A unique market moment and the case for active judgment

Martin Romo

Martin Romo

July 9, 2026

We are living through an extraordinary market environment. The level of concentration in many equity benchmarks has increased significantly.

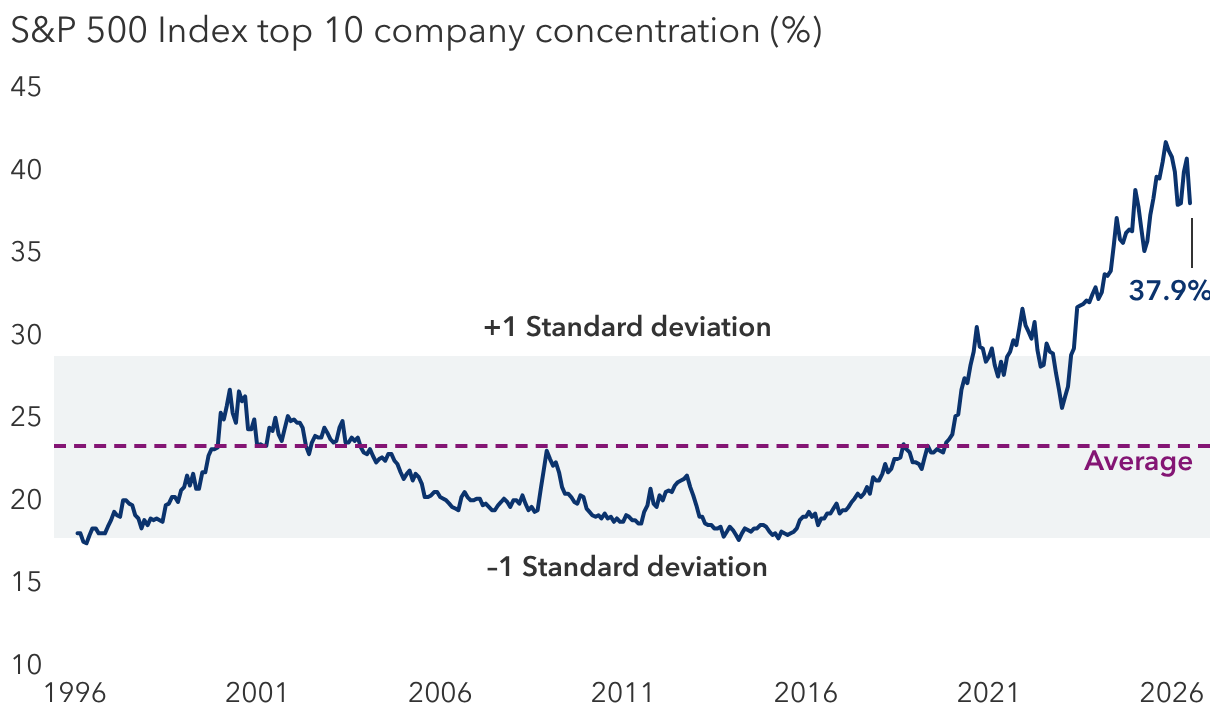

The evidence is striking. The 10 largest companies in the S&P 500 represent nearly 40% of the index, a level not seen since the mid-1960s. Semiconductor-related companies are approaching one-fifth of the S&P 500. In emerging markets, the exposure is even more acute: Three companies alone — TSMC, Samsung and SK hynix — represent 29% of the MSCI EM Index.

As this concentration grows amid investor euphoria, I felt it appropriate to remind Capital’s investment group of our responsibilities, which I did in collaboration with Capital Group Vice Chair Jody Jonsson and CEO Mike Gitlin. I want to share those same thoughts with you now.

As I told my colleagues, Capital Group’s mission to improve people’s lives through successful investing carries a deep obligation. We are entrusted with the savings of individuals, families and institutions who rely on us to grow their wealth, generate income, fund retirements, support beneficiaries and leave enduring legacies.

That requires us to pursue superior long-term outcomes on a risk-adjusted basis with the discipline to help protect, to the best of our abilities, our clients’ savings during market extremes. We should not simply mirror the risk profile of an index when that index becomes unusually concentrated or extended, as is increasingly the case in markets around the world today.

How today’s market structure is driving concentration

This is not an argument against investing in companies driving the artificial intelligence era. Many are extraordinary businesses with durable prospects. The point is that, at today’s weights and valuations, the benchmarks — and the passive strategies following them — increasingly assume one set of outcomes will dominate.

We have seen this before. Markets have always displayed moments when leadership narrows around a compelling view of the future. Sometimes that view is right. Sometimes it is partly right but valued to perfection. And sometimes the greatest beneficiaries are not the ones investors expect.

In 1980, fossil fuels represented 29% of the S&P 500; today they are roughly 3%. At the peak of Japan’s late-1980s equity boom, Japan reached 44% of the MSCI World Index; today it is around 5%. These are not perfect analogs, and concentration is not a timing tool. But they are powerful reminders that benchmark weights can become increasingly concentrated as conviction in a prevailing theme builds.

A handful of stocks are driving a highly concentrated market

Sources: Capital Group, FactSet, S&P Global. Figures represent the index concentration of the top 10 companies by market capitalization. Standard deviation is a statistical measure of how much values vary from their average. A higher number indicates greater variation. Data shown is monthly, from January 31, 1996, through June 30, 2026.

History shows that the leaders of one era are rarely the leaders of the next. Active managers can use research and judgment to adapt as market leadership evolves. Maintaining a clear-eyed view of fundamentals can be especially important when enthusiasm becomes widespread.

Passive investors may be taking unintended risks

A passive allocation by design is a benchmark tracking position with no mechanism to manage valuation risk, position size or changes in underlying fundamentals. Indices do not assess whether a business is strengthening or weakening, whether a competitive moat is widening or narrowing, or whether today’s price adequately compensates investors for long-term risk.

Jody Jonsson recently testified before the U.S. Congress and told its members that there is a broad misperception that index funds somehow are safer for most investors. She explained that an index fund doesn’t assess whether markets are overvalued, whether a sector is in a bubble, or whether a specific holding has deteriorated.

As index ownership has grown to roughly half of U.S. assets under management, the share of investors actively weighing prices against fundamentals has declined. Jody noted in her testimony that active managers play a central role in price discovery — the process by which markets translate information into price — while index funds, by design, do not.

A moment to rebalance — and to exercise judgment

Of course, where deep fundamental research gives us conviction, we managers should hold AI beneficiaries where appropriate. We should seek companies that can use AI to improve productivity, strengthen moats and expand addressable markets. We research and invest globally across the full value chain for opportunities the benchmark may underappreciate and where valuations may provide compelling risk-adjusted returns.

And we should size positions with an awareness that market benchmarks can become lopsided in markets like the ones we are seeing today.

We recognize that our clients do not hire us simply to replicate the risk profile of an index. They hire us to exercise judgment and thoughtful differentiation in investments to deliver solid results over the long term. And that is what we have done.

Our job is to remain faithful to a process that has navigated change for nearly a century. That heritage goes back to our founder, Jonathan Bell Lovelace. He recognized early the power of collaborative research, diverse perspectives and a long-term view, which became the foundation of The Capital System™. It was not designed for easy markets. It was designed for markets like this one.

The winners of this current period will need to be both bold and humble. Bold enough to own great companies when the fundamentals justify it. Humble enough to recognize that no single theme, however powerful, should dictate the shape of portfolios. Bold enough to differ from the benchmark when risk and reward call for it. Humble enough to know that being different can be uncomfortable but necessary, especially when a narrow market continues to rise.

Learn more about

Martin Romo is a portfolio manager for Capital Group U.S. Equity Fund (Canada).

MSCI Emerging Markets Index: A free-float-adjusted market-capitalization-weighted index designed to measure equity market results in global emerging markets.

MSCI World Index: A free-float-adjusted market-capitalization-weighted index designed to capture large- and mid-cap representation across developed market countries.

S&P 500 Index: A market capitalization-weighted index of about 500 major U.S. stocks. Includes reinvested dividends but excludes fees and taxes.

Our latest insights

RELATED INSIGHTS

-

Global Equities

-

U.S. Equities

-

Commissions, trailing commissions, management fees and expenses all may be associated with investments in investment funds. Please read the prospectus before investing. Investment funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. For investment funds other than money market funds, their values change frequently. For money market funds, there can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian investment funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2026. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.