Technology & Innovation

Categories

Energy

Clean hydrogen: Growing opportunities beyond the hype

Seema Suchak

Seema Suchak

Cheryl Wilson

Cheryl Wilson

February 14, 2023

Demand for clean energy is climbing fast. Many companies, industry bodies and over 150 countries have committed to or are considering net-zero targets. What is net zero? Put simply, it refers to a status where the amount of human-produced greenhouse gas (GHG) emissions is offset by an equal reduction. Clean hydrogen is expected to play a crucial role in helping heavy industry decarbonize to meet these targets. Our specialists explore the investment implications for some of the most carbon-intensive sectors.

Why is hydrogen important for the energy transition?

Hydrogen can be used as a carrier of energy and as an input into chemical and industrial processes. Clean hydrogen is a crucial decarbonization tool for a range of industrial activities, including steel, aluminum, iron and chemical production. We also see it as an option to decarbonize commercial transportation and, notably, the energy and utilities sector. Significant demand will likely initially come from today’s users of gray hydrogen (see hydrogen rainbow below), such as oil refiners and chemicals producers. But as the world progresses toward net zero, that usage could eventually be overtaken and then diminished by growing demand from heavy industry and energy storage.

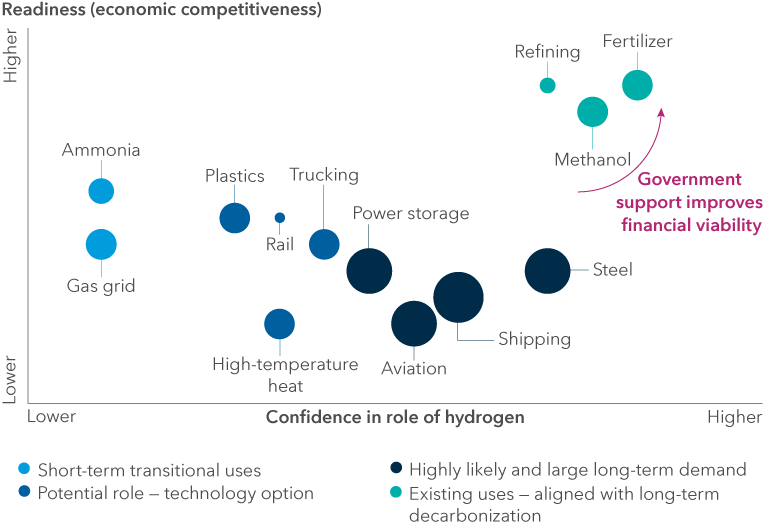

Sweet spots for clean hydrogen adoption

Source: SYSTEMIQ analysis for the Energy Transitions Commission 2021. Note: Readiness refers to technical readiness, economic competitiveness and ease of sector use. High-temperature heat refers to industrial heat above 800 degrees Celsius. Current hydrogen use in refining is higher due to oil consumption.

The Inflation Reduction Act is a game changer

Clean hydrogen is only produced in small quantities today, but it is changing. Clean energy legislation and government financial support for hydrogen projects should help to establish infrastructure and meet the high cost of transitioning away from fossil fuels. In the past decade, governments in Europe and Asia have mostly led the way — but now the U.S. is joining the journey. The $369 billion clean energy spending package included in the Inflation Reduction Act will be transformational in the U.S. and beyond. Signed into law in August 2022, this landmark legislation includes massive clean-energy-related financial incentives for individuals and businesses. Crucially, clean hydrogen supply and demand should be boosted by a 10-year production tax credit, an investment tax credit for energy storage technologies and a new tax credit for hydrogen fuel cell (and battery-powered) commercial vehicles. “The Inflation Reduction Act of 2022 looks set to be transformational,” says equity investment analyst Doug Upton. “I expect to see very large amounts of capital allocated to blue hydrogen and green hydrogen over the next five years.”

The new measures come on the heels of the $8 billion earmarked in the 2021 Infrastructure Investment and Jobs Act for creating regional hydrogen hubs. Hydrogen’s role in the energy transition is still nascent, but it can work hand in hand with electrification. Hydrogen can serve as a fuel for areas of the economy that are hard to decarbonize, like steel production and trucking. It offers another way to store energy in much larger capacities for industries such as long-haul transport, where current battery technology limits the adoption of electric vehicles.

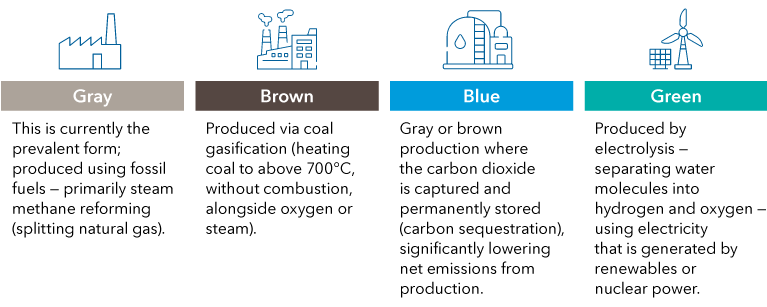

Clean hydrogen can be labeled as blue or green within the hydrogen rainbow, an informal naming convention that connotes the relative GHG emissions arising in production. “Everyone is focused on the explicit clean energy hydrogen subsidy, but the 70% jump in the carbon sequestration tax credit may prove even more consequential,” says equity investment analyst Gideon Spitzer. This credit is increasing from $50 per metric ton of stored carbon dioxide (CO2) to $85 per metric ton. “Blue hydrogen projects have become financially viable as carbon sequestration becomes a cost-competitive technology on an after-tax basis,” Spitzer adds. In several countries across Europe, explicit carbon price and taxing programs have been deployed to help incentivize investment in alternative energies, including green hydrogen.

The hydrogen rainbow

Three disrupted areas we’re keeping a close eye on

1. Cost-effective green steel is on the long-term horizon

The steel industry has been hard to decarbonize, relying on carbon-intensive industrial processes for production. Historically, steelmakers have used the blast furnace-blast oxygen furnace method (BF-BOF), which uses coal to reduce the iron ore and remove oxygen before it is converted into steel. Now steelmakers have developed a method in which only hydrogen and renewable energy are required: Iron ore is reduced with green hydrogen in a direct reduced iron (DRI) plant. The iron is then sent to an electric arc furnace (EAF), and steel is produced in a process powered by renewable energy. In this way, the use of fossil fuels can (in theory) be eliminated, and the production of steel generates no CO2.

Use of green hydrogen in the DRI-EAF process is unlikely to be deployed at scale before 2035. Current economics, including the upfront capital required to transition the production process, are not that favorable. In the near term, consumers of steel will need to be comfortable paying a premium for green steel. Demand is likely to come from customers such as automakers and infrastructure providers who increasingly wish to source CO2-free steel to bolster the green credentials of their products. In the wake of the Russia-Ukraine war, European governments are committing serious capital to funding green hydrogen projects. There are already several pilot programs underway to further develop green hydrogen technology in steel production. Steelmakers in countries across parts of Europe, Asia and Canada have greater access to competitively priced renewable energy, and these countries will likely lead as hubs for green steel.

Steelmakers with operations in countries with lower cost renewable energy — that are supported by government subsidies for clean hydrogen solutions — will be best positioned first movers. The European Union granted €143 million to Sweden’s Hydrogen Breakthrough Ironmaking Technology (HYBRIT) initiative. The joint project by the steel, mining and power companies SSAB, LKAB and Vattenfall is tasked with developing a hydrogen-based production plant for CO2-free steel. The plant should bring steel to market as soon as 2026 and is estimated to reduce Sweden’s carbon emissions by up to 10%. Future developments in carbon pricing may accelerate market adoption. China has the world’s largest emissions trading scheme (ETS), a market-based approach to controlling GHG emissions that allocates a limited number of emissions permits to carbon-intensive sectors. Although China’s ETS currently only covers power generation, by 2025 it is expected to also incentivize industrial sectors, including steel, to decarbonize their operations.

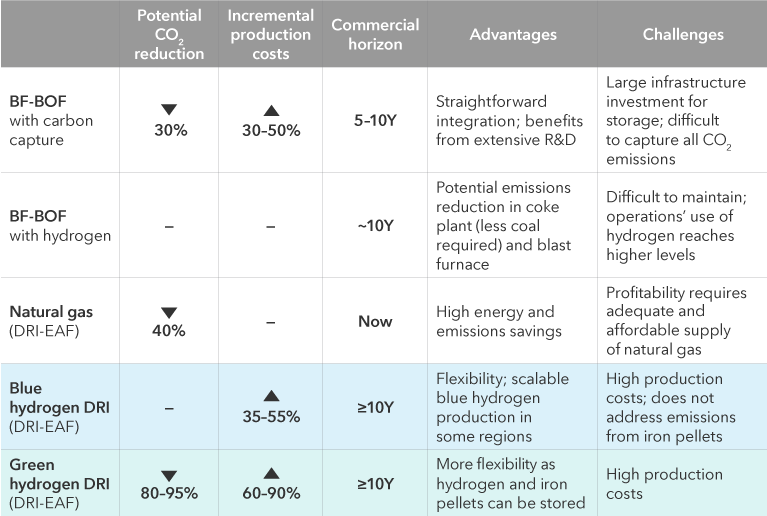

Potential costs and benefits of hydrogen-powered green steel

Source: Analyses and estimates from Ernst & Young Global Limited mostly based on transition to low-emissions steel in Europe. Incremental production costs (operating expenditure and capital expenditure) compared with average annual net income of steel industry. Values compared for crude steel production. Sources: BNP Paribas, BHP, IEA and ArcelorMittal. Data as of June 2021.

2. Hydrogen’s role in the energy and utilities sectors will be crucial for the energy transition

Use of hydrogen across the energy and utilities sectors is currently negligible. For green hydrogen to be a viable fuel, feedstock and energy storage solution, increased investment is needed in renewables, electrification and an upgrading of the power grid. Blue hydrogen is also an option, especially as depleted oil and gas fields can be used for carbon storage.

The U.S. currently has few large-scale oil and gas company-led clean hydrogen projects underway. However, the Inflation Reduction Act’s incentives should entice companies scoping out possibilities to move off the sidelines. “With an explicit tax credit of up to $3 per kilogram for low-carbon hydrogen, the economics of blue hydrogen projects look a lot more compelling,” says Craig Beacock, equity investment analyst. “Meaningful progress on development and execution are now much more likely.”

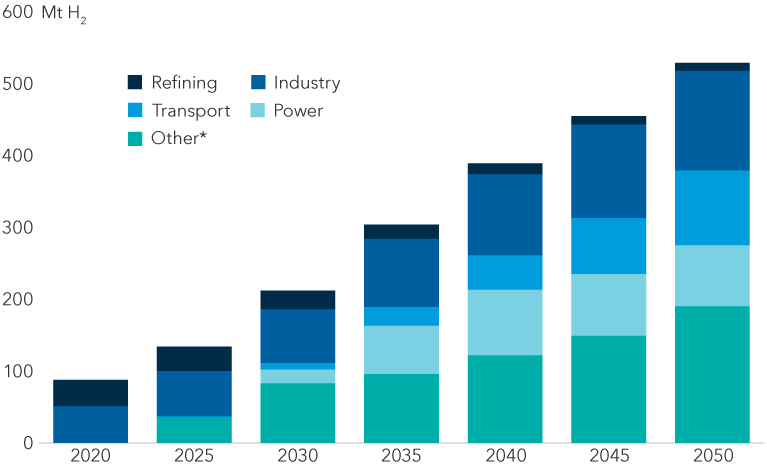

Growing global hydrogen demand in a net-zero scenario

*Other includes ammonia, grid injections, buildings, NH3 — fuel and synfuels.

Source: International Energy Agency. 2020 actual, 2025–2050 based on net-zero scenario estimates, as of October 2021.

3. For commercial vehicles, hydrogen could overtake batteries

Advances in battery technology and charging infrastructure mean hydrogen fuel cell models may remain a niche choice in the passenger vehicle marketplace. For long-haul and heavy road transport, however, hydrogen fuel cells should prove a compelling option with greater range and faster refueling. The price of hydrogen and fuel cells, as well as the infrastructure build-out and government incentives, will influence just how quickly hydrogen becomes a competitive option. Transportation could grow to become a leading consumer of clean hydrogen demand over time, according to a study by the International Energy Agency (IEA). Heavy trucks, marine ships and aircraft are anticipated to account for the lion’s share of demand.

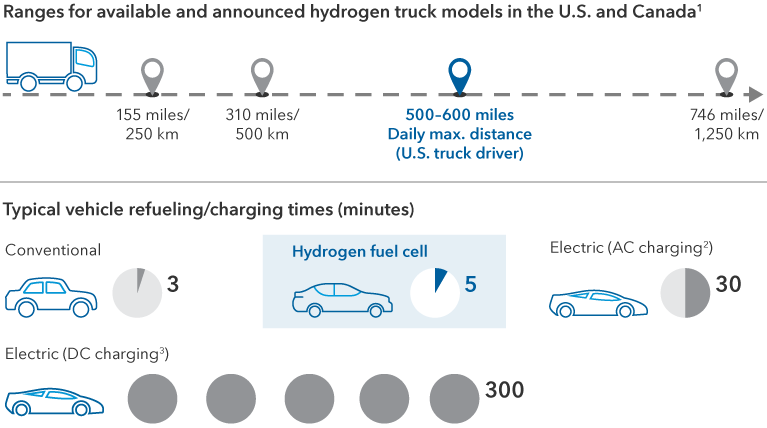

Range and refueling time: Why hydrogen fuel cell use could rise

Sources: International Council on Clean Transportation (hydrogen fuel cell truck ranges, from October 2020 report), Wishart, Jeffrey (2014). Fuel Cells vs Batteries in the Automotive Sector and U.S. Congressional Research Service. Ranges and times are illustrative only. Within federal limits on hours of driving, 500 to 600 miles is the distance a U.S. truck driver can cover in a typical day. 1Ranges up to 400 km are currently in production in the U.S. and Canada; >400 km up to 1,250 km ranges have been planned but are currently in pre-production stages. 2AC= alternating current. 3DC = direct current.

Is it time to get ahead of the coming disruption?

Whether the net-zero commitments of various governments, industries and companies are met remains to be seen. What seems clearer is that making substantial progress toward meeting targets will be very challenging without widespread use of clean hydrogen. For instance, pledged clean hydrogen projects globally amount to less than one-tenth of what is likely needed to achieve net zero. The availability of low-cost renewable energy, in addition to government incentives, will be crucial to the successful deployment of clean hydrogen projects over the long term. While net-zero commitments are long term, fiscal incentives and other government support should help create early opportunities for long-term investors. Over the years, assuming renewable energy costs become even more competitive with fossil fuels, use of clean hydrogen could flourish. From heating buildings to fueling furnaces, and from hydrogen-powered trains to ships fueled by green ammonia, clean hydrogen has the potential to reshape the investment landscape.

Learn more about

Don't miss our latest insights.

Related insights

OUR LATEST INSIGHTS

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

On or around July 1, 2024, American Funds Distributors, Inc. will be renamed Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.