Politics

Matt Miller

Matt Miller

There is much to digest from Tuesday’s historic U.S. midterm elections. With Democrats gaining a majority in the House of Representatives for the first time since 2011, and Republicans widening their majority in the Senate, each side can legitimately claim a qualified victory. Indeed, that’s exactly the message we heard in dueling press conferences on Wednesday.

Once they are finished celebrating, however, the tough work of governing the nation under a divided Congress will begin. What might that political environment look like? Can they get anything done on the legislative front? What are the likely implications for financial markets?

Here are three key developments that, in my view, will characterize the U.S. political scene over the next two years:

1. Government gridlock

Bottom line: do not expect much substantive change to happen between now and the 2020 presidential election. Major new Republican initiatives – such as additional tax cuts or immigration reform – are highly unlikely to pass, to the extent they require House approval. The same applies to any big-ticket items on the Democratic wish list, such as rescinding last year’s tax cuts, rolling back regulatory reductions or any sort of Medicare-for-all proposal.

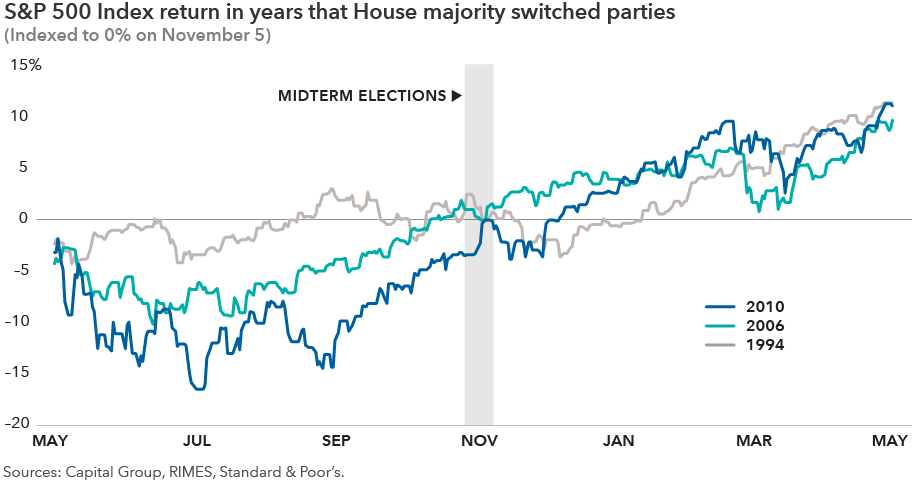

Early indications are that the stock market likes this gridlock scenario, as evidenced by the broad-based rally the day after the election. For companies, it means the status quo is likely to remain in place for the next two years. That’s a good thing for chief executives who now can advance their business plans accordingly. As we’ve seen in past years when the House has flipped, the market tends to take it in stride.

2. Limited areas of cooperation

While gridlock will be the overriding theme in Washington, it wouldn’t surprise me if some limited areas of cooperation emerge over the next two years. For Democrats and Republicans, it simply makes sense to get something done – not just so they can claim to be rising above partisanship, but so they have at least a few accomplishments to trumpet during the next election.

Predicting where this common ground may be found is challenging in such a hostile political environment. It’s entirely possible that no agreements will emerge. But some promising areas include increased infrastructure spending, new limits on drug pricing, a minimum wage hike and paid family leave. All are issues where Republicans and Democrats, at least at one time, had some overlapping interests.

In addition, one risk to the tax status quo involves a potential deal around the federal debt ceiling, which is expected to be addressed in the summer or fall of 2019. At his Wednesday press conference, President Trump signaled a willingness to make some “adjustments” on tax policy in negotiations with Democrats. We’ll have to wait and see what develops there, if anything.

3. It’s all about 2020

Needless to say, the U.S. presidential campaign began at midnight Tuesday. Everything must be seen in that context. Whatever happens over the next two years, every move will be calculated and measured based on how it could impact the presidential race. There probably will be new investigations launched by House Democrats. The White House and Senate Republicans may counter with their own.

On the legislative front, House Democrats probably will propose numerous measures that have no chance of passing the Senate. We may see proposals for new taxes on the wealthy, a rollback of corporate tax cuts, and perhaps even an attempt to expand the number of seats on the Supreme Court. Those measures will likely be dead on arrival, but may prove to be valuable talking points come 2020.

Market implications

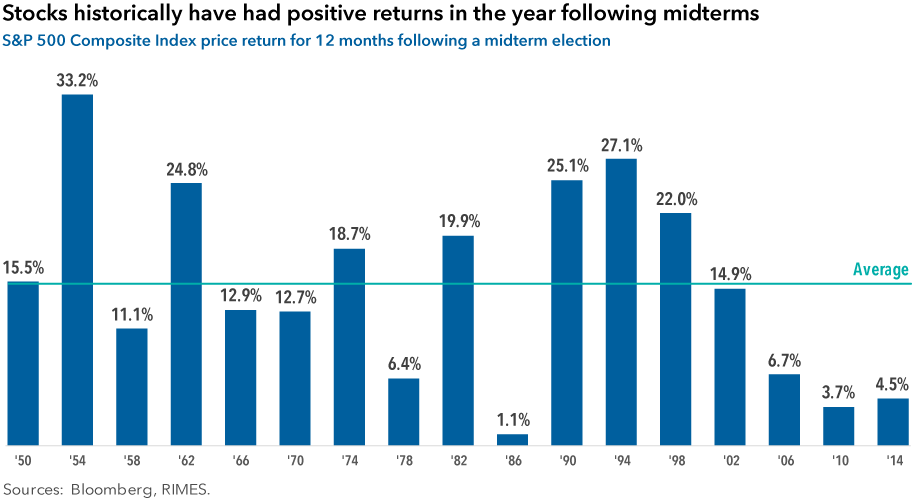

There’s no telling how markets will react to these events going forward. The sharp selloff we saw in October is a reminder that heightened volatility can return at any time, even when the U.S. economy is humming along nicely. But it’s always worth taking a look at history as one considerable data point.

Since 1950, U.S. stocks have always generated positive returns in the year following a midterm election. That may or may not be the case in 2019. But for investors with a long-term perspective, it’s worth noting that markets have the dynamic capacity to ignore political noise and move to the beat of their own drummer. More often than not, that’s good old-fashioned company fundamentals.

Our latest insights

-

-

-

Interest Rates

-

-

Municipal Bonds

This is the headline for the Newsletter promo. Customize the message.

RELATED INSIGHTS

Never miss an insight

The Capital Ideas newsletter delivers weekly investment insights straight to your inbox.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.