Pharmaceuticals

How oral GLP-1s could reshape the weight-loss drug market

Christopher Lee

Christopher Lee

July 10, 2026

The first surprise was that people were willing to inject themselves.

When the first generation of GLP-1 weight-loss drugs arrived, many assumed that a weekly injection would limit their appeal. Instead, millions of people embraced the treatment. After all, the drugs delivered something previous generations of medications largely could not: meaningful and sustained weight loss.

Researchers uncovered other benefits — lower cardiovascular risk, reversing liver disease, improving sleep apnea and others. In the process, GLP-1s became one of the most consequential pharmaceutical breakthroughs in history. Now, the industry is entering a new phase.

In late 2025, regulators approved the first oral GLP-1 for weight loss, and a second followed a few months later. The introduction of an oral tablet may seem incremental compared to the excitement that greeted the original injectables, but I believe it represents a substantial advance for the category. For investors, it demonstrates that the opportunity may be even broader and more durable than anticipated.

If the first chapter of the GLP-1 story was proving that millions of people were willing to embrace a weekly injection, the next chapter may be about expanding the market far beyond that initial audience. Early evidence suggests the oral formulations are reaching patients who were not previously using GLP-1s. That implies that the overall market may be expanding, rather than demand merely shifting from injections to pills.

If oral GLP-1s are luring new patients rather than simply cannibalizing existing treatments, the opportunity could prove substantially larger than investors once envisioned.

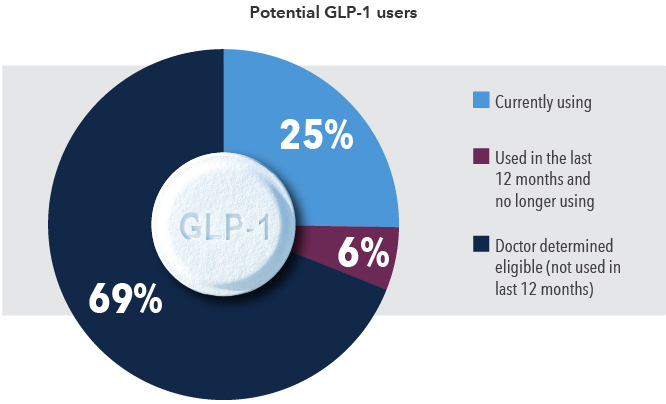

Up to three-quarters of people who could use GLP-1s are not using them currently

Source: National Center for Health Statistics (NCHS). NCHS Rapid Surveys System Round 7 Datasets and Documentation. As of March 2026.

The simplicity of an oral tablet matters for both users and suppliers.

For investors, the obvious question is whether pills will eventually make injections obsolete. I don’t think they will.

Patients now have more options, allowing them to choose which weight loss drug is the best fit considering their lifestyle and medical history alongside cost and potential side effects.

Injectable GLP-1s may remain the preferred option for patients with severe obesity or related conditions such as cardiovascular or liver disease, while oral therapies appear to be drawing in a different set of users.

Some patients simply prefer the convenience and familiarity of a daily pill over an injection. Others may be hesitant about self-injecting altogether. These differences in preference, while straightforward, have meaningful implications for how broad the market for GLP-1s may ultimately become.

From a supply standpoint, a pill offers a fundamentally simpler distribution model. Injectable GLP-1s require specialized manufacturing facilities, cold storage and a more complicated supply chain.

Those constraints become even more pronounced across geographies. In certain regions, the infrastructure required to store and distribute injectable therapies at scale is limited or does not exist. In those settings, an oral formulation may be the only viable option for widespread access.

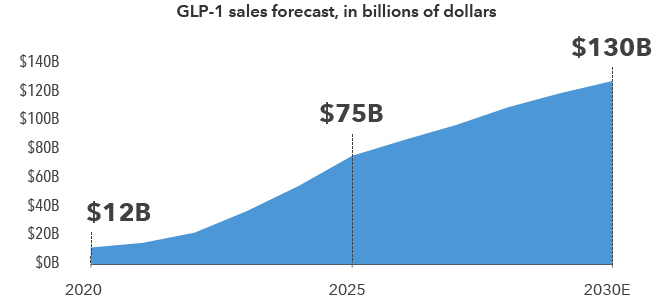

With a large addressable market, sales are forecast to grow through 2030

Source: S&P Global - Visible Alpha. As of November 2025.

In addition, I envision treatments evolving over time. A patient might start with an injectable for major weight loss before transitioning to an oral medicine for maintenance. As more products are unveiled — including longer-acting injections that may eventually be administered monthly or even quarterly — the number of consumer options will likely expand.

Durability of demand makes the opportunity more compelling.

Some people may achieve lasting weight loss through medication and lifestyle change that allow them to discontinue treatment. But I suspect they will represent a minority. If diet and exercise alone were sufficient, obesity rates would likely be very different today.

This observation touches on an important shift occurring alongside the development of these drugs: a changing understanding of obesity.

For decades, obesity was often framed as a matter of personal discipline. Being overweight was viewed as evidence of poor choices or insufficient willpower. Yet the scientific evidence indicates that genetics and neurochemistry play meaningful roles in regulating body weight, and that pharmaceutical intervention is achieving outcomes that decades of advice about diet and exercise often couldn’t. The medicines don’t replace healthy habits, but they reveal how deeply biology influences weight.

In some ways, this reminds me of the evolution in attitudes toward mental health. Conditions such as depression were once commonly dismissed as character flaws or failures of will. Over time, advances in science revealed underlying biological mechanisms that needed to be addressed through a multitude of methods, including in many cases, pharmaceutical intervention.

That is why I believe the story surrounding GLP-1s is still in its early chapters. The market continues to expand, the science continues to advance and new formats are making these therapies accessible to more patients. The first chapter was convincing people to embrace an injection. The next chapter may be bringing these medicines to millions more.

Explore topics

Related insights

-

-

U.S. Federal Reserve

-

Economic Indicators