Active Management

Categories

Trade

U.S. tariffs overturned: What happens next?

Tom Cooney

Tom Cooney

February 23, 2026

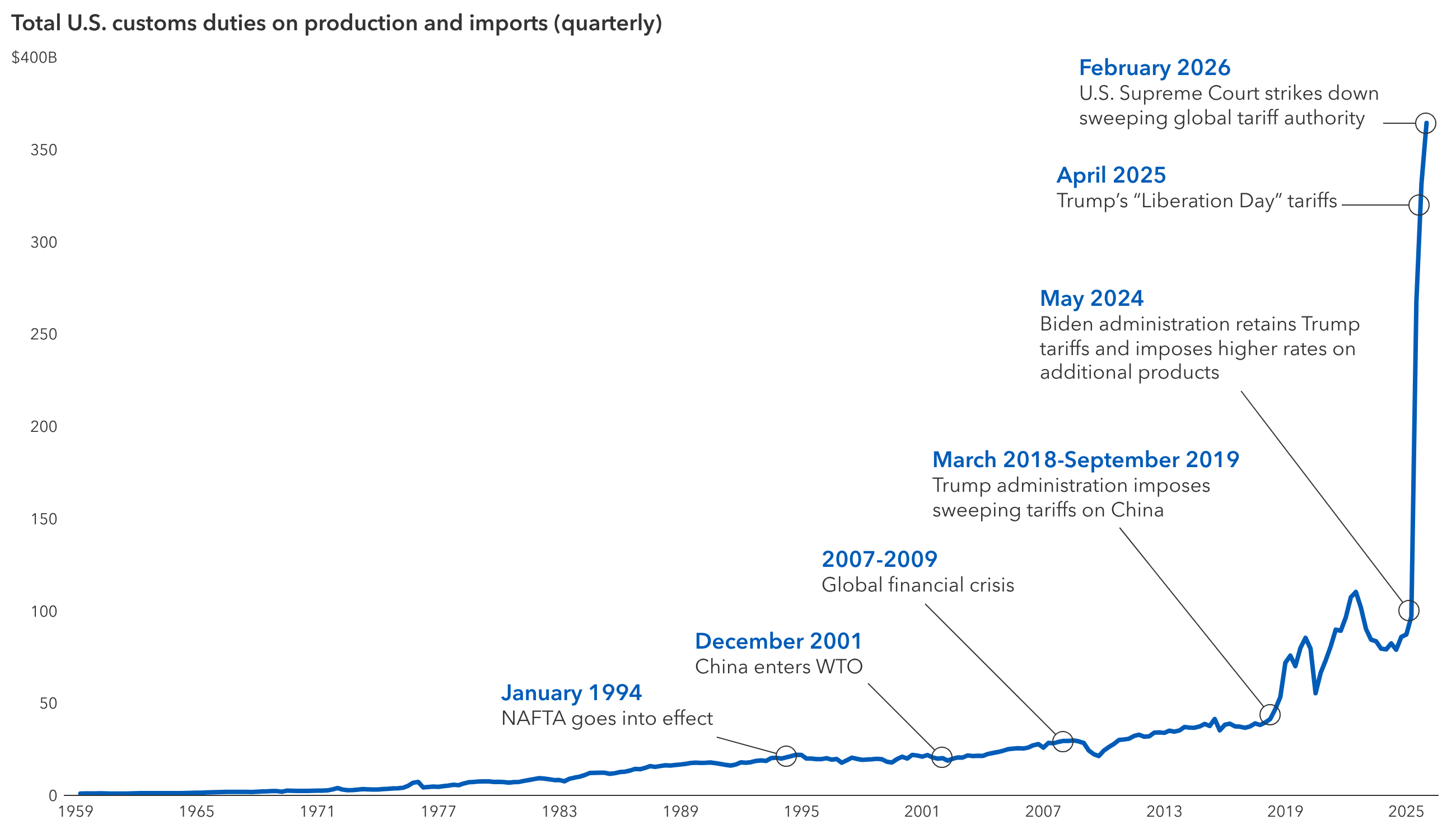

The U.S. Supreme Court has knocked down some of the pillars of President Trump’s global tariff structure, but over the next few months it is likely to be rebuilt. The wall will simply have a different look, in my view, as it is reconstructed with alternative materials.

The court on Friday struck down all the tariffs Trump implemented under the International Emergency Economic Powers Act (IEEPA), including the so-called “Liberation Day” tariffs. While that decision was undoubtedly a major setback for the White House, the administration retains several alternative and far more legally durable statutory authorities through which it can reestablish most of the existing tariffs.

The president immediately announced his intention to begin using those authorities. The first step is a 15% blanket global tariff to be imposed for the next five months under Section 122 of the U.S. Trade Act of 1974. This tariff will serve as a temporary placeholder, ensuring that revenue continues to flow while giving the Office of the U.S. Trade Representative time to pursue a series of country-by-country investigations under Section 301 of the act, addressing alleged unfair trade practices.

Trade barriers: U.S. tariffs have risen sharply in recent years

Sources: Capital Group, U.S. Bureau of Economic Analysis, Federal Reserve Bank of St. Louis. As of February 20, 2026.

In summary, much of the tariff wall is likely to be restored over the next six months using authorities approved by Congress considerably more resilient to legal challenges than IEEPA. Importantly, only IEEPA-based tariffs were invalidated by the court. Other sector-specific tariffs — such as those covering automobiles, steel and aluminum — remain in place because they were imposed under Section 232 of the U.S. Trade Expansion Act of 1962, a statute with firmer legal footing.

Moreover, the administration has threatened additional sector-based tariffs over the past year on medical supplies, semiconductors, pharmaceuticals and other products. These warrant close attention as the administration moves to reconstruct the broader tariff framework.

Near-term uncertainty in global markets

New trade uncertainty may emerge as policymakers and markets debate how to address the tens of billions of dollars in IEEPA tariff revenue that has already been collected. The court ruling did not address this issue, meaning that refund claims from importers, and potentially even from consumer groups, are likely to tie up lower courts for several years.

The outcome also has ramifications for countries that have already reached trade deals with the United States based on IEEPA tariff leverage, including the United Kingdom, Japan, Vietnam, Indonesia and the European Union. Some observers have raised the question of whether those countries might seek to renegotiate their agreements. In my view, that is unlikely. The Trump administration could respond by initiating punitive Section 301 investigations and by turning to other trade-related and non-trade-related tools, such as U.S. support for Ukraine, to pressure countries seeking revised terms.

However, even if these countries do not pursue renegotiation, it is conceivable that economies such as the EU, Japan and Korea, which committed to hundreds of billions of dollars each in investment in the United States, could move more slowly to fulfill those commitments. This is because the U.S. had incorporated the threat of “snap back” penalty tariffs into the agreements if sufficient investment progress was not made. But those penalties were based on the now-vacated IEEPA authority.

Recall that various tariff deals struck last year were executed at considerably lower rates than were announced on “Liberation Day” in April 2025. The actual effective U.S. tariff rate has hovered in a range of about 14% to 17% in recent months. With Section 122 in place for five months, and then new 301 tariffs complete, we still end up at an effective rate of roughly 13% to 14%. So, the tariffs will still be high, but their composition will be different.

U.S. Treasuries may come under pressure

From a market perspective, U.S. Treasuries could come under near-term pressure, pushing yields higher. Fixed income markets have already treated tariff revenues as part of fiscal planning at a time when the U.S. Congressional Budget Office forecasts US$1.9 trillion in debt this year. In 2025, the U.S. government collected about US$287 billion in customs duties, according to U.S. Treasury data. A ruling against the tariffs could also trigger refund obligations potentially exceeding US$100 billion, further adding to fiscal uncertainty and weighing on Treasuries.

Learn more about

Our latest insights

-

-

Demographics & Culture

-

-

Trade

-

RELATED INSIGHTS

-

Global Equities

-

-

Economic Indicators

Commissions, trailing commissions, management fees and expenses all may be associated with investments in investment funds. Please read the prospectus before investing. Investment funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. For investment funds other than money market funds, their values change frequently. For money market funds, there can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian investment funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2026. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.