Artificial Intelligence

Categories

Markets & Economy

Answers to your 5 biggest investment concerns

Martin Romo

Martin Romo

Darrell Spence

Darrell Spence

Ritchie Tuazon

Ritchie Tuazon

August 9, 2021

Markets have been climbing a wall of worry in 2021, reaching record highs even as investors brace for the possibility of elevated inflation, rising interest rates, runaway debt and a bitcoin bubble. With so much to trouble investors, many are wondering how these uncertain times will affect their portfolios.

That’s what we found when we polled more than 5,000 financial professionals recently to identify their top questions and concerns. Here are our investment team’s answers to the five most frequently asked questions of 2021:

1. Will U.S. inflation and rising rates affect my portfolio?

We received more questions about rising U.S interest rates and inflation than any other topic. And that was before the U.S. Consumer Price Index accelerated 5.0% in May and 5.4% in June — the two highest year-over-year growth rates since 2008.

The thinking goes like this: A powerful economic recovery fueled by massive stimulus measures will lead to runaway inflation, forcing the U.S. Federal Reserve to raise rates quicker than expected, which would slow economic growth and be a significant headwind to investors.

U.S. economist Darrell Spence doesn’t expect current levels of inflation to be sustainable over the long term, as they are still being driven by significant price increases in a small number of categories. “That said, a clear risk to this scenario is that a resurgence of the virus causes portions of the economy to shut down again and policymakers to unleash another round of stimulus,” notes Spence. “This will simply prolong the imbalance between stimulus-induced demand and COVID-restricted supply, and likely cause inflation to remain more persistent.”

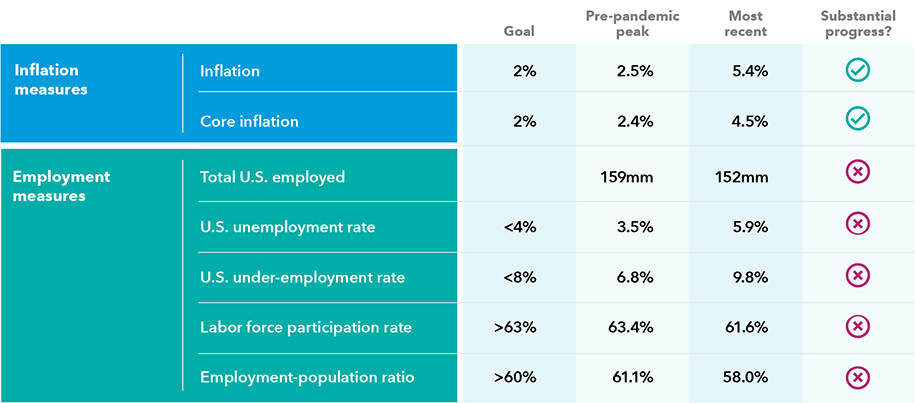

U.S. inflation has jumped but labour data suggests it may be temporary

Sources: Bloomberg, Bureau of Economic Analysis, U.S. Bureau of Labor Statistics, U.S. Federal Reserve. Data as of 6/30/21. Goals for the inflation and employment measures are estimated targets needed to meet the Federal Reserve’s stated dual mandate of achieving price stability and maximum sustainable employment. Goals for inflation are directly from the U.S. Federal Reserve. Goals for employment are estimates from Capital Group. Pre-pandemic peak considers the trailing 12 months prior to February 2020. Inflation shown based on the U.S. Consumer Price Index, with core excluding energy and food. Under-employment rate consists of total unemployed, plus all persons marginally attached to the labour force, plus total employed part time for economic reasons.

Likewise, the Capital Group rates team does not believe we have shifted to a new era of high long-term inflation, although it may remain elevated for longer than some initially expected. “While we should continue to see inflation volatility, I expect it to subside by the end of next year,” says Ritchie Tuazon, fixed income portfolio manager.

U.S. market jitters over these short-term inflationary pressures have hastened expectations for an interest rate hike to 2022. “That’s far earlier than anticipated given the U.S. Federal Reserve’s stated desire to let inflation run hot and get the U.S. economy back to full employment,” says fixed income portfolio manager Pramod Atluri.

In recent years, the Fed has made it a priority to take their time and signal moves well in advance. So before the next rate increase, the Fed is likely to take several distinct steps to facilitate the tapering of its bond-buying activities and communicate an imminent hike.

Bottom line: Inflation will likely remain elevated through the end of next year but then should moderate back to the Fed’s 2% long-term target. Higher volatility is likely as surprises in inflation data could trigger market turbulence in the near term. Our rates team believes the Fed’s first interest rate hike is at least 12–18 months away.

2. Is surging U.S. debt sustainable?

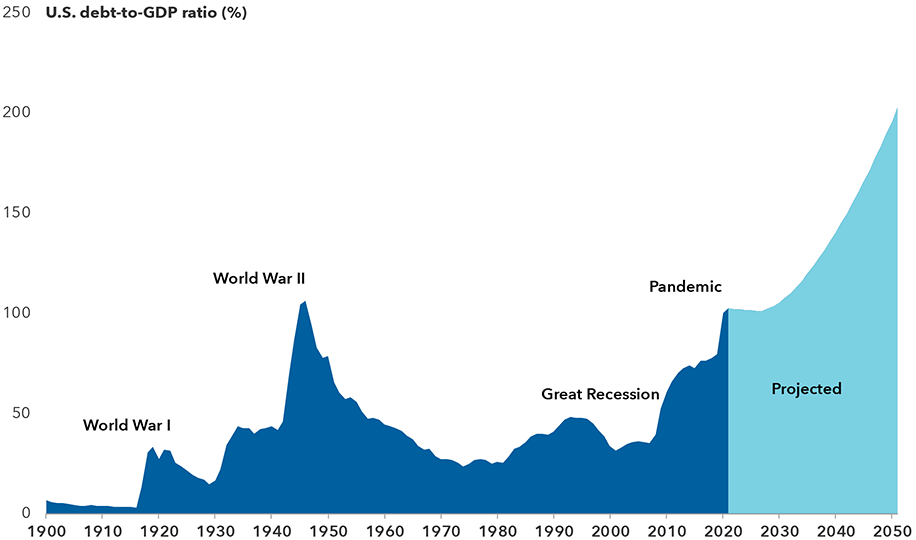

U.S. government debt has been mounting, and current policy proposals suggest there is no end in sight. The passage of a $1.9 trillion pandemic relief package in March helped drive the trailing 12-month federal deficit to 18.6% of gross domestic product — the largest shortfall since 1945. This will almost certainly push Uncle Sam’s public debt above its World War II-era peak of 106% of GDP.

U.S. debt is projected to reach new heights

Source: U.S. Congressional Budget Office as of March 4, 2021. Federal debt held by the public. Long-term forecast excludes the impact of the American Rescue Plan Act of 2021 and assumes no meaningful changes to current laws affecting U.S. government revenues and spending. Based on USD.

So with U.S. debt nearing unprecedented levels, is it time for investors to worry? Opinions vary, but here are four reasons U.S. debt may not spiral out of control:

- U.S. interest rates are lower than GDP growth

- The U.S. debt position is worsening but is not an outlier

- Governments have various levers to pull

- Monetary policy can adapt to changing conditions

Between the perpetually low U.S. interest rate environment and a multitude of U.S. government response measures available, current debt levels should be sustainable for now. Typically, a debt crisis arises when investors are no longer willing to purchase a country’s debt, and that seems unlikely to happen in the U.S. anytime soon.

Bottom line: Although U.S. debt may act as a headwind to long-term growth, it is unlikely to cause a crisis as long as interest rates are lower than GDP growth and the U.S. dollar remains the world’s reserve currency. Even if debt eventually becomes an issue, it could be decades before markets feel an impact.

3. Should I shift from growth to value stocks?

The growth-value decision doesn’t have to be an either-or proposition, says veteran equity portfolio manager Martin Romo, one of the portfolio managers on Capital Group U.S. Equity FundTM (Canada).

“There can be growing companies that are cheap and cheap companies that grow, so value and growth are not in opposition,” Romo noted in a recent interview. We are in a target-rich environment, and there are opportunities to invest in fast-growing companies as well as classic cyclical companies."

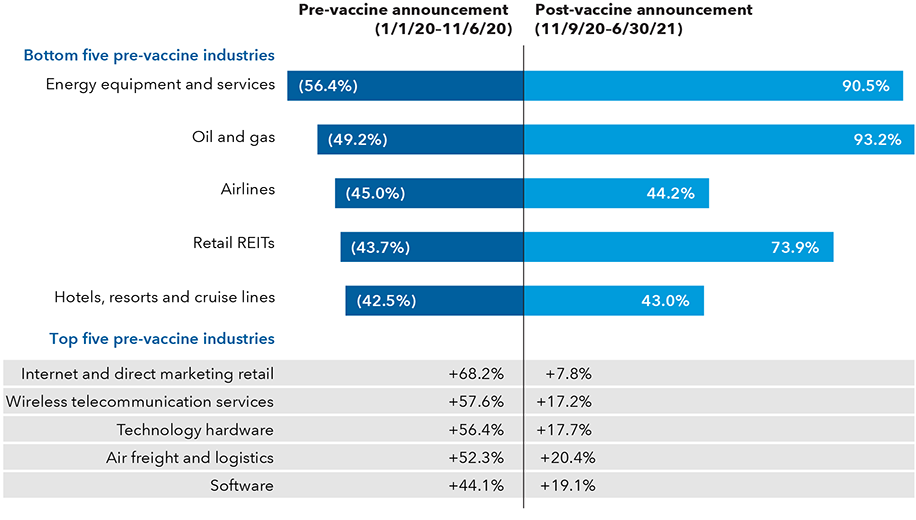

Value stocks got a booster shot in November 2020 when the first COVID-19 vaccine was found to be highly effective. Since then, industries that suffered the most during the pandemic such as energy, financials and real estate have enjoyed massive rebounds. However, the two worst performing sectors in the market in 2021 through June 30 — utilities and consumer staples — are also traditionally value sectors.

November 9 was a turning point for many cyclical companies

Sources: FactSet, Standard & Poor’s. All data represent total returns for industries within the Standard & Poor's 500 Composite Index and are in USD. 11/6/20 was the last business day before the Pfizer-BioNTech vaccine candidate was revealed to have more than 90% efficacy against COVID-19 in global trials.

Bottom line: It’s important to balance individual investment opportunities rather than make decisions based on a binary label like growth or value. And as markets continue to reach new records and frothy valuations increasingly become a concern, company-by-company analysis will likely become even more essential.

4. Is Big Tech in big trouble?

U.S. government efforts to rein in Big Tech have been underway for years, but 2021 could be a watershed moment. Political, societal and market-based forces are combining to put these companies — Alphabet, Amazon, Apple, Facebook, Microsoft and others — under the microscope. It’s an important issue for investors, as these stocks enjoyed dazzling returns over the last decade. They are among the largest in the world and may represent outsized positions in many portfolios.

Assessing the regulatory risks of large tech companies is a complex task, given that they operate in different industries with vastly different competitive profiles — everything from retail to advertising to television.

The antitrust cases against Google and Facebook don’t appear to be strong and likely won’t result in any forced breakups, according to Brad Barrett, an analyst who covers ad-supported internet companies. Notably, many of the products provided by these goliaths are free, diminishing traditional antitrust arguments that rely on pricing power to help determine monopoly status. And in the unlikely event that one or more of these companies is forced to break up, a reasonable argument could be made that some of the spinoffs may be worth more on their own.

In addition to antitrust issues, legislation over content monitoring and privacy and data protections are also on the table. But according to internet analyst Tracy Li such regulations may have surprising consequences for the industry. “I believe that concerns related to privacy or content may actually strengthen, rather than weaken, the moats of the largest platforms,” says Li. “These companies often boast well-established protocols and deep resources pertaining to privacy and legal matters."

Bottom line: Regulatory pressures may continue to hang over Big Tech stocks for years, but current valuations already reflect much of this risk. An outright breakup of companies seems improbable, and even in that unlikely scenario a spinoff of certain assets could unlock additional shareholder value.

5. My client wants to invest in Bitcoin. What should I tell them?

Fear of missing out is a powerful force in investing. And it’s difficult to ignore an asset that has gained more than 500,000% in just a few years, eliciting headline-grabbing commentary from Elon Musk and Warren Buffett, among others.

Bitcoin and other cryptocurrencies have captured the imagination of investors, putting financial professionals, plan sponsors and consultants at the centre of an increasingly frenetic discussion about whether to jump into the fray or steer clear.

“If you have a client who really wants to buy Bitcoin, just saying ‘don’t do it’ is a disservice,” says Barbara Burtin, an equity investment analyst who covers the banking industry. “In fact, owning a small amount can be a learning experience — for you and the client.”

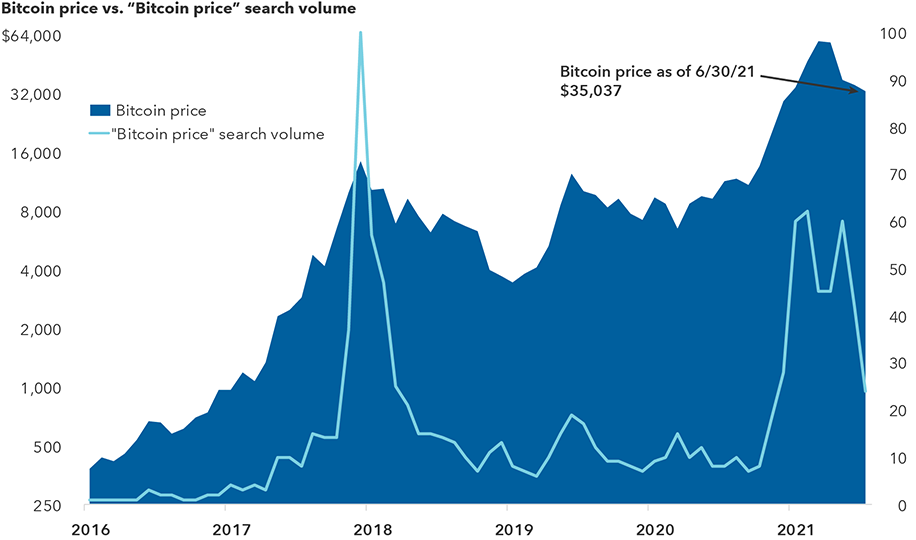

In a recent article, How to talk to clients about Bitcoin, Burtin suggested investors dedicate no more than 1% of their portfolio to any cryptocurrency. Such a limit may have seemed overly conservative because Bitcoin’s price had done nothing but skyrocket for months. But the fastest growing assets often fall just as quickly and, given Bitcoin’s speculative nature, the suggestion had merit. Since then, Bitcoin prices have declined nearly 40% in U.S. dollars.

“If a client insists, ‘I must put money into this,’ advise them to invest no more than they can afford to lose,” Burtin cautioned.

Bitcoin has had periods of spectacular gains — and losses

Sources: Google Trends, Refinitiv Datastream. As of 7/14/21. Prices are shown on a logarithmic scale and expressed in U.S. dollars. Search volume data represent Google search volume relative to the highest point for the given time period. A value of 100 is the peak popularity for the term. A value of 50 means that the term is half as popular as the peak.

Bottom line: It may be tempting to dismiss Bitcoin as a fad and tell clients it’s inappropriate for their portfolios, but simply discounting it won’t be an adequate answer for some. There are certainly risks associated with Bitcoin and other cryptocurrencies, but there are also groundbreaking innovations and potential for the future of the technology. Whether looking at cryptocurrencies for your clients or your own portfolio, discipline and proper expectations are key.

Learn more about

Our latest insights

-

-

Demographics & Culture

-

Artificial Intelligence

-

-

RELATED INSIGHTS

-

Artificial Intelligence

-

Artificial Intelligence

-

Commissions, trailing commissions, management fees and expenses all may be associated with investments in investment funds. Please read the prospectus before investing. Investment funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. For investment funds other than money market funds, their values change frequently. For money market funds, there can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.