Artificial Intelligence

Categories

Trade

Supply chain shifts signal reglobalization

Noriko Chen

Noriko Chen

Ben Lin

Ben Lin

Kent Chan

Kent Chan

August 23, 2022

The fragility of global supply chains exposed during the COVID-19 pandemic remains one of the top economic challenges facing the world. In one respect, globalization has long been characterized by developed market countries offshoring production to lower cost locations. But now, companies are recognizing the need to build redundancies into their supply lines, which will have varied impacts on countries, companies and industries.

While some have argued this could lead to a less globalized world or “deglobalization,” this could be the start of an era of “reglobalization," in which supply chains are reorganized and more countries are brought into global trade networks.

“I would expect most companies with a significant percentage of their manufacturing base in Greater China (including Taiwan) to diversify to other countries,” says Noriko Chen, equity portfolio manager. “The reinvestment in some countries is likely to be positive. But it will also come at a cost to profitability for some companies. However, this should lead to new investing opportunities for those who can identify companies that will benefit from changes in global trade patterns.”

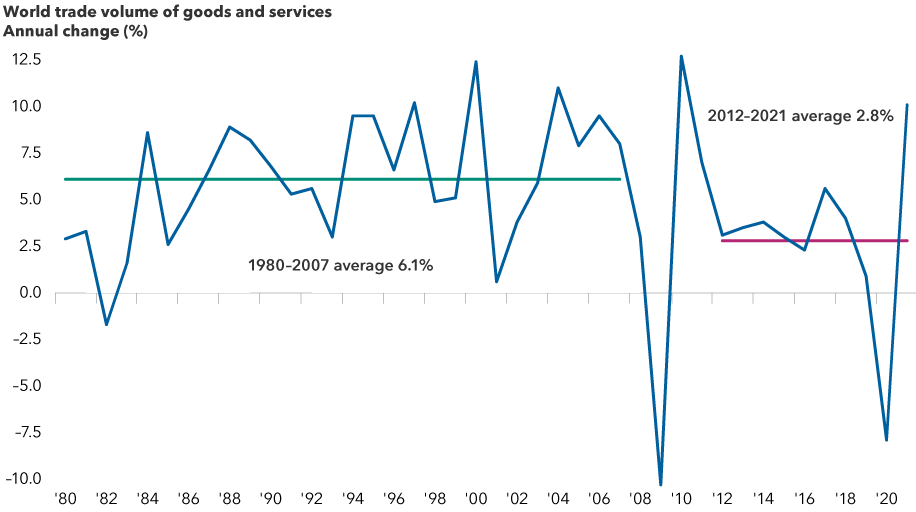

Global trade has slowed but is still growing

Sources: International Monetary Fund, Refinitiv Datastream. As of December 31, 2021.

Supply chains are shifting but not deglobalizing

Many companies are shifting their areas of manufacturing operations to multiple centres across the globe to disperse risk. That does not necessarily mean this could result in less economic integration. Consider Taiwan-based TSMC, the world’s dominant manufacturer of cutting-edge semiconductors. After having concentrated the bulk of its capacity in Taiwan — a focal point of geopolitical tensions — TSMC is building its first manufacturing hub in the United States. It’s also constructing a new semiconductor plant in Japan.

Multinationals with a significant presence in China are also looking for that next big opportunity to reach consumers outside of China. Apple, which has arguably built the most impressive supply chain of any multinational in China, moved some iPhone production to India, which is forecast to have an estimated 1 billion smartphone users by 2026.

There are also Chinese companies seeking to forge closer trade links with their customers outside of China. Chinese electric vehicle (EV) battery maker CATL (Contemporary Amperex Technology Co.) recently received approval to build a battery cell plant in Germany, where it works with the top German automakers.

Diversification from China will take time

For those companies reducing their dependence on China, the diversification from China’s supply chain will take time. China is likely to remain significant due to lack of viable alternatives and because more goods made in China will increasingly target Chinese consumers in the future.

“A common phrase I hear from companies is ‘China Plus,’” says Ben Lin, an investment analyst at Capital Group. “This means manufacturers will retain their existing China factory, but will gradually add production capacities outside of China and slowly build up the domestic supply chain in those countries. This could take at least several years or even a decade before they can replace Chinese suppliers.”

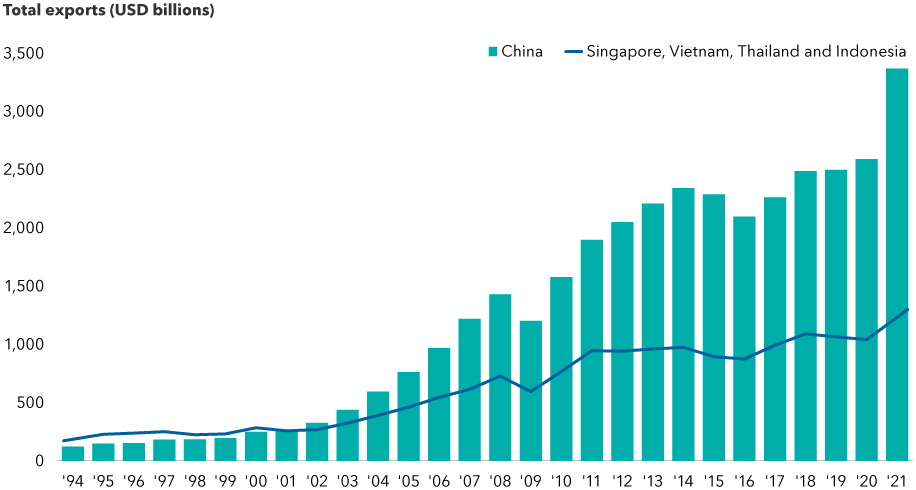

China's export sector dwarfs Southeast Asian rivals

Capital Group, Refinitiv Datastream. As of December 31, 2021. Values are not adjusted for inflation.

For now, China remains one of the world’s top destinations for foreign direct investment flows, which reflect companies buying, building or reinvesting in operations abroad. In 2021, China ranked second behind the U.S., with US$334 billion of flows, according to data from the Organisation for Economic Co-operation and Development (OECD).

Multinationals still see value in tapping into China’s large and skilled workforce. A case in point is Tesla. China has become a key production hub for the dominant EV maker. Tesla opened its Shanghai gigafactory in 2019 to help boost its annual car production and increase its global market share by selling to the world’s top consumer of EVs.

Another area is health care. Pharmaceutical giants such as AstraZeneca and Pfizer have built strong relationships with domestic Chinese biopharmaceutical companies to help develop and test new drugs. Clinical trials account for approximately 90% of the cost of developing a drug for global use, and labour costs for clinical trials are cheaper in China compared with the U.S., Germany and Switzerland, according to Capital Group analysts who cover the health care sector.

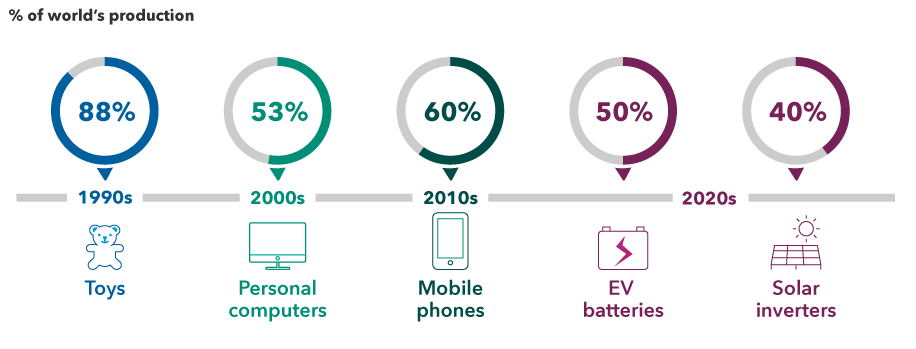

China has moved up the manufacturing value chain

Source: Capital Group, based on reports from Euromonitor, SNE Research and company filings. Data as of May 2021 and reflect approximate figures.

Building security and redundancy in supply chains

The global supply chain has been under unprecedented stress, from the U.S.-China trade war to the COVID-19 pandemic to the war in Ukraine. If any industry has felt the brunt of the supply chain snarls, it’s been the auto business.

General Motors, Ford, Stellantis and other global automakers have faced steep production cuts, resulting in a scarcity of vehicles on dealer lots and a sharp increase in the prices of new and used cars. This is leading to structural changes within the auto industry, which has had to entirely rethink its supply chains. One outcome has been a move away from receiving “just-in-time” inventory to holding “just-in-case” inventory when it comes to semiconductors.

Building redundancies in supply chains will come with opportunities and challenges. Certain industries will be beneficiaries, ranging from those supplying semiconductor equipment and industrial components to automation tools and physical metals.

“I anticipate reshoring to be a major growth driver for select industrial companies over the next five to 10 years,” says equity investment analyst Gigi Pardasani. “Many U.S. industrials are investing at levels we have not seen since the early 2000s to better position themselves to meet this demand.”

In the near term, there will be financial costs and potential ramifications of supply chain shifts, such as:

Greater levels of corporate spending and higher operating costs. For Western companies moving production back to their home markets, or for Asian companies expanding their footprint into the West, the costs will be higher than running factories solely in China or other Asian countries. Companies are likely to either pay for more expensive automation equipment or higher wages for workers.

Higher costs for consumers. Inflation is already running at a 40-year high in the U.S. as higher prices ripple through global supply chains. Higher costs for companies to build more inventories or reshore manufacturing is likely to translate into higher prices for consumers. Companies will absorb some, but not all, of the costs, which could weigh on consumer demand for their products.

Higher working capital needs and operating margin pressure due to costs associated with building redundancy and flexibility in supply chains. These factors could weigh on future margins and valuations for companies. Lower returns on invested capital may be here to stay as a result of a change in the geopolitical landscape and central banks’ rate policies.

“Companies and businesses with pricing power or economies of scale may benefit from this environment, but those without these advantages may face profit margin and earnings pressure and potentially lower valuation multiples,” says equity investment director Kent Chan.

However, he adds, there’s the possibility that “those companies that are able to diversify sourcing and build greater security and resilience in their supply chain may be rewarded with a higher valuation longer term, in spite of the costs.”

Opportunities from global shifts in production

Looking at modern history, this is not the first time the global supply chain has been realigned.

In the early 1990s, Hong Kong was a hub for textiles, and Taiwan was a large manufacturer of sneakers. That gradually changed when China set up special economic zones, luring manufacturers with a more affordable option.

“Not only did these shifts in the supply chain not harm the economies of Hong Kong and Taiwan, but rather created room for the evolution of their respective economies,” recalls Chan, who worked in Hong Kong in the 1990s. “Over time, Hong Kong overtook Tokyo to become Asia’s leading financial services hub, and Taiwan moved up the value curve to become the world’s dominant manufacturer of semiconductors.”

This is a reminder that, despite worries around supply shortages, fears of deglobalization and the expected shift in global supply chains, new opportunities could emerge in the regions where production is shifting, as well as in those countries where production is leaving.

Learn more about

Our latest insights

-

-

Demographics & Culture

-

Artificial Intelligence

-

-

RELATED INSIGHTS

-

-

Technology & Innovation

-

Long-Term Investing

Commissions, trailing commissions, management fees and expenses all may be associated with investments in investment funds. Please read the prospectus before investing. Investment funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer. For investment funds other than money market funds, their values change frequently. For money market funds, there can be no assurances that the fund will be able to maintain its net asset value per security at a constant amount or that the full amount of your investment in the fund will be returned to you. Past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.