Investing after the war ends

As we anxiously await the outcome of peace negotiations, I am looking ahead to the investment opportunities that may emerge as the world moves on from this conflict. In my view, developed ex-US and emerging market stocks were highly attractive before the Iran war interrupted a rally in non-US markets, and I think they are still attractive today. The biggest reason for that is a valuation advantage.

Even after a strong rally among non-US stocks in 2025, stocks in the rest-of-world are still trading at a sizable price-to-earnings discount relative to the S&P 500. Emerging markets are trading at a roughly 40% discount. So, in my view, there are real bargains outside the US today, and often they can be found among companies that are world leaders in their industries. They include UK-based drug giant AstraZeneca, China-based Tencent, the largest gaming company in the world, and Taiwan Semiconductor Manufacturing Company, the largest computer chip maker in the world.

Much earlier in my career, leadership shifted back and forth between US and non-US stocks. It was like a game of ping-pong. I think there is a strong chance that we are headed back to that type of investment environment — where US stocks lead for a while, but other regions also have their time to shine.

Energy sector on the rise

I am also constructive on the energy sector, which has also been out of favour with investors for many years. Yes, oil companies such as Exxon, Royal Dutch Shell and TotalEnergies have benefited from higher oil prices during the Iran conflict, but I find the sector attractive on a long-term basis, as well.

Setting aside near-term moves in oil prices, the industry has changed its spots in recent years. There is less focus on finding new oil fields to drill and more of an emphasis on being thoughtful about the balance sheet, strategic about capital expenditures, and serious about dividends. I am not likely to walk away from the oil industry after this conflict is over because it offers some positive attributes for long-term shareholders, not the least of which are very generous dividend payments.

I am also sifting through the artificial intelligence wreckage for companies that may have been unfairly hit by fears that easy-to-use AI applications will impair their business. Those include large software companies, such as Germany’s SAP, and companies in the online travel space, including China’s Trip.com and Spain’s Amadeus IT Group. These companies are AI enablers, in my view, not ‘AI roadkill’.

Volatility is your friend

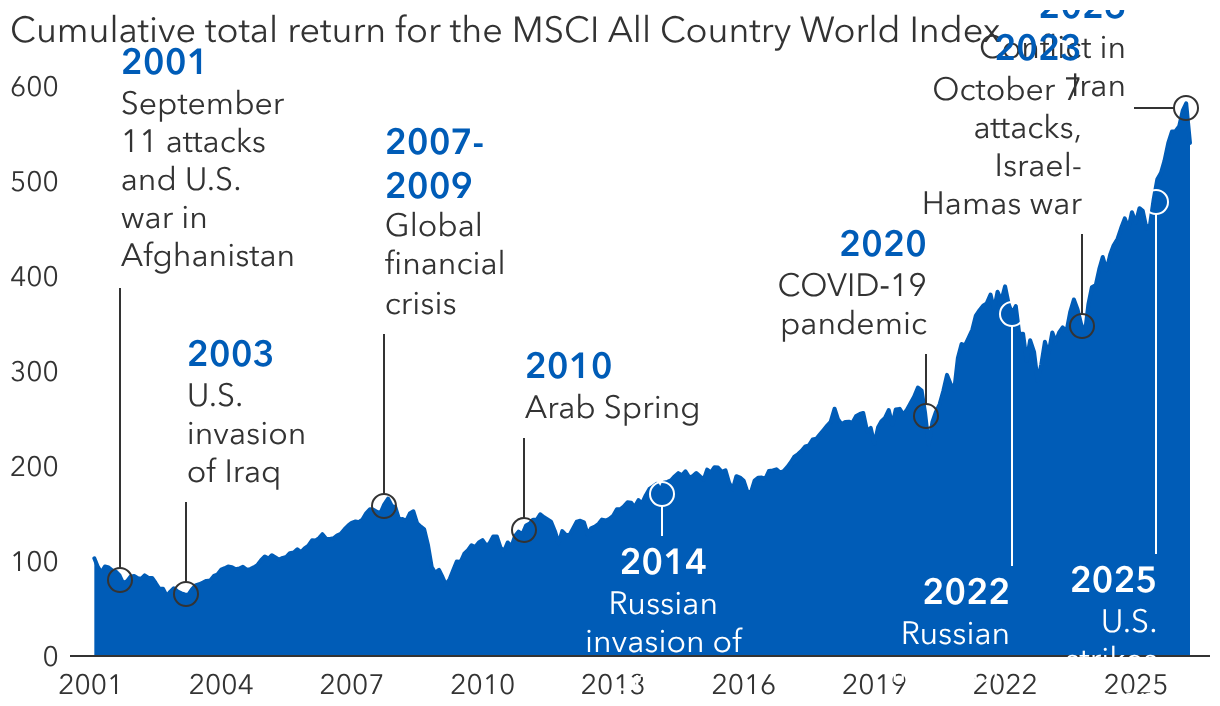

All the investment themes I have discussed thus far have gone through bouts of volatility, unloved by investors for one reason or another. It comes with the territory, especially if you are the type of investor, like me, who prioritises valuations and doesn’t mind waiting for an investment to come back into favour at some point down the road. Trouble and uncertainty are fertile hunting grounds for these opportunities.

And uncertainty is always just around the corner. We may imagine a past characterised by low volatility, and great certainty, but I think if that's how you remember the past, you're probably misremembering.