Retirement Income

Categories

Insights on Investors

3 Reasons to Rethink Global Equity

Mark Barile

Mark Barile

Chris Lanctot

Chris Lanctot

Holly Colvin

Holly Colvin

January 5, 2024

In the centuries-old riverside town of West Newbury, Massachusetts, advisor Holly Colvin at Helm Financial Planning serves a wide range of clients with different backgrounds and needs. “Many of my clients are young and need more growth in their portfolios,” says Colvin. “At the same time, other clients have reached a stage in life when they need to draw on their assets.”

Recently, Colvin identified a common theme in many of her client portfolios: a lack of global diversification following significant market shifts over the last few years. She reached out to Capital Group’s Portfolio Consulting and Analytics team to discuss options for international equity exposure. The team suggested a more flexible global equity model that could be easily customized to different clients. (International equity includes developed non-U.S. equity and emerging markets, whereas global also includes U.S.)

“I wanted a fresh point of view from professionals whose perspective I could trust,” Colvin says. A certified financial analyst and former municipal bonds trader, Colvin worked at Capital Group before becoming a financial advisor more than 20 years ago. She consulted with the team in the past and valued their suggestions. In the three years since they last met, her business had nearly tripled, and she felt that some of her models had morphed with the market.

Here are three insights that helped Colvin rethink her global equity allocations, which may help you rethink yours too:

1. International equity exposure may reduce concentration risk

It may not be surprising that some advisors have avoided international equity over the last decade, with the S&P 500 Index returning 11.91% for the last 10 years ended September 30, 2023, versus 3.35% for the MSCI All Country World Index ex US (ACWI ex US). “We see a lot of scenarios where advisors are underallocated to international equity,” says portfolio consultant Chris Lanctot. “What may be surprising,” he adds, “is the potential for international equity right now, especially given a heavily concentrated U.S. equity market.” In fact, international equities are far less concentrated than the U.S. equities market, where the top 10 stocks made up nearly a third of the S&P 500 Index as of September 30, 2023 — as much as during the height of the dot-com bubble. “A broader international landscape offers the potential for less concentration risk than domestic markets,” says Lanctot.

International equities are far less concentrated than the S&P 500

Source: Capital Group, Morningstar. As of 9/30/23. Past results are not predictive of results in future periods.

2. Company revenue is as important as domicile

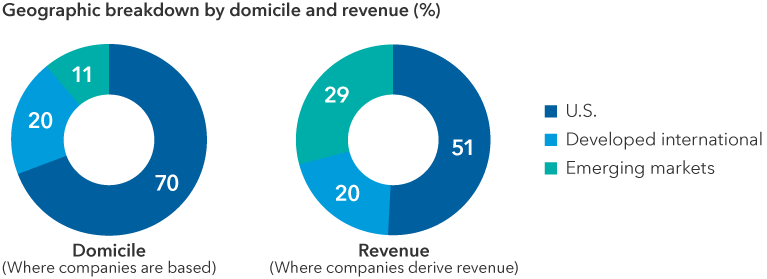

“I was most interested in the analysis of where company revenues come from rather than where companies are domiciled,” says Colvin. “That’s a fantastic way to approach global diversification, rather than only focusing on where companies are based. It’s a more targeted approach to global diversification to think about how good a company is at accessing consumers in every part of the world,” she says.

Average advisor regional allocations by revenue versus domicile

Sources: Capital Group, FactSet, and Morningstar. Totals may not reconcile due to rounding. The average advisor portfolio is representative of the aggregate exposures of 1,188 advisor portfolios analyzed by Capital Group’s Portfolio Consulting and Analytics team from 7/1/23 to 9/30/23.

By domicile (where companies are based), advisor equity exposure averaged about 70% U.S. and 30% non-U.S. equities (20% in developed international and more than 10% in emerging markets). When analyzing the underlying holdings based on where companies derived revenues, the total non-U.S. exposure increased to almost 50%. “We find revenue exposure to be a compelling way to deconstruct risk and diversification, while positioning the benefits of research-driven global flexibility,” Lanctot says.

3. Global flexibility can help as markets shift

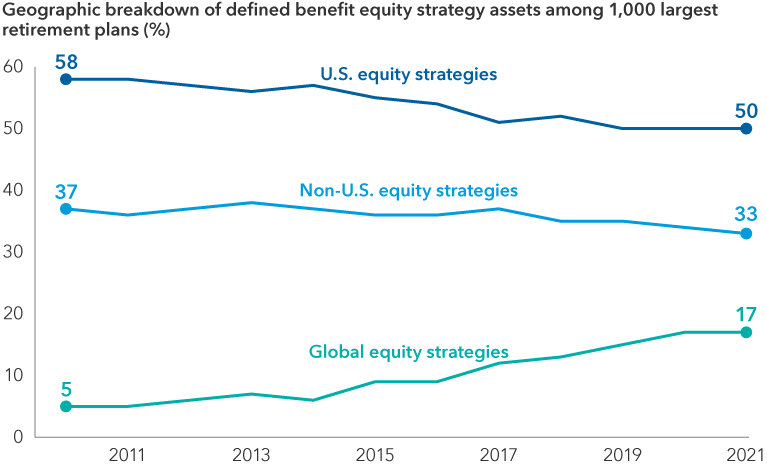

“Most advisors do not have global flexibility in their client portfolios,” says Lanctot. In fact, the average advisor portfolio has only a 6% global average allocation. Fifty-five percent of advisors have no global allocation at all, according to our research.* Meanwhile, institutional allocators for defined benefit plans steadily increased exposure to global equity mandates from 5% in 2010 to 17% in 2021. “Over the years, average advisor exposure to global equity hasn’t kept pace with increased global allocations to defined benefit plans,” says Mark Barile, manager of the Capital Group Portfolio Consulting and Analytics team. “Now may be the time for advisors to rethink that and stay ahead of the curve, especially given that advisors tend to follow institutional trends like this over time,” says Barile.

“We encourage advisors to make their portfolios more dynamic via global exposure,” says Lanctot. “Many advisors are using regional exchange-traded funds (ETFs) to access global exposures. But using active global ETFs instead can be a good way to take advantage of opportunities around the globe in real time, based on direct investment research,” Lanctot says. Ultimately, Colvin decided on a global model that includes Capital Group ETFs with flexible global allocations.

Advisors may be underallocated to global strategies

Could advisors follow rising global allocations in defined benefit plans?

Sources: First chart: Capital Group. Second chart: Pensions & Investment Research Center (as of 12/31/21).

“International equity research is a major strength at Capital Group, from my point of view,” says Colvin. “We looked at a range of vehicles for the global model. I liked the flexibility of the global and international ETFs and how they were able to access company opportunities across emerging and developed markets.” While she likes to dig into the details of portfolio construction and conduct her own analysis, she says she appreciates having access to the team’s sophisticated tools and software used to discuss different success metrics.

To Colvin, it was also important that the team took an unbiased look at the characteristics of different vehicles from many different firms in the industry and was able to point out the pros and cons of different investment options relative to her client portfolio goals. “They respected all the portfolio design and research I had done. The team also recognized that many of my client portfolios are tax-sensitive, and kept the analysis focused on my preferred investment vehicle of ETFs,” says Colvin.

“I got the second opinion I was looking for to think through a global model that could be adapted for different clients,” she says.

Looking for another perspective on global allocations?

Get an unbiased point of view on portfolios and talk through solutions with trusted partners. Connect to your Capital Group representative or sign up for an in-depth portfolio analysis and review today.

Learn more about

*The Capital Group Portfolio Consulting and Analytics team analyzed 1,188 portfolios in consultation with financial professionals from July 1, 2023 through September 30, 2023. Of the portfolios specifically analyzed for global flexibility, 539 had allocations to the Morningstar Global Large Blend, Value and/or Growth and Global Small/Mid Stock categories. These 539 portfolios comprised 45.37% of all portfolios analyzed, while 649 portfolios (or 54.63%) did not have an allocation to global equity strategies. To determine the average allocation to global equity strategies, the team took a weighted average of the allocation to global equities across all 1,188 portfolios. They calculated that weighted average by multiplying 45.37% (percentage of portfolios that had allocations to global equity strategies) by their average allocation (13.41%) and then added the product of those two numbers to the product of 54.63% (percentage of portfolios that had no allocations to global equity strategies) by 0% (since those 54.63% of portfolios had 0% allocated to global equities). The sum of those two products is 6.1%: the average allocation to global equities across all 1,188 portfolios analyzed from July 1, 2023 through September 30, 2023.

The S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

MSCI All Country World ex USA Index is a free float-adjusted market capitalization-weighted index that is designed to measure equity market results in the global developed and emerging markets, excluding the United States. The index consists of more than 40 developed and emerging market country indexes. Results reflect dividends gross of withholding taxes through December 31, 2000, and dividends net of withholding taxes thereafter.

MSCI EAFE® (Europe, Australasia, Far East) Index is a free float-adjusted market capitalization weighted index that is designed to measure developed equity market results, excluding the United States and Canada. Results reflect dividends net of withholding taxes. This index is unmanaged, and its results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes.

Past results are not predictive of results in future periods.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and/or summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

This material does not constitute legal or tax advice. Investors should consult with their legal or tax advisors.

There have been periods when the results lagged the index(es) and/or average(s).

The indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. Please visit the data provider's website for more information.

Each S&P Index ("Index") shown is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2026 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.