Long-Term Investing

Categories

Bonds

Midyear Outlook: Inflation? Keep calm about bonds and carry on

Pramod Atluri

Pramod Atluri

Ritchie Tuazon

Ritchie Tuazon

Karl Zeile

Karl Zeile

June 18, 2021

Higher inflation and rising yields have some investors questioning whether they should stick with bonds. Undoubtedly, 2021 is shaping up to be one of the more challenging years for fixed income investments in recent times. Even so, reports of the bond market’s death are greatly exaggerated. It’s no time to listen to the bond bears: Owning bonds in this kind of environment remains as important as ever.

As our colleagues explained in their U.S. outlook and its international counterpart, economic growth is expected to be strong. However, that strength will not be uniform across regions and sectors. The recovery has global policymakers on both the fiscal and monetary side curtailing their unprecedented COVID-19 stimulus. For central bankers, in particular, that normalization process will likely be gradual. They must consider the risk of upsetting the financial market as the recovery unfolds.

Although inflation has hit the Federal Reserve’s 2% target, full employment remains far from its goal. The central bank has communicated that it will endure inflation above target for some time. It sees this target as an average, not a ceiling. Inflation averaged below that level until recently.

In the Fed’s June meeting, monetary policymakers shifted their projections for 2023 from zero to two 25 basis point hikes. We believe the central bank is likely to follow through accordingly, assuming that unforeseen negative factors don’t throw labor market and broader economic recoveries off track. The Fed could begin to slow, commonly referred to as “taper,” its asset purchases as soon as later this year.

Currently, temporary pandemic-driven supply shortages and pent-up demand dynamics appear to be driving higher prices. But the unprecedented level of fiscal and monetary stimulus paired with some structural changes such as demographic trends could result in more persistent above-average inflation.

Markets have accounted for increased probability of sustained inflation in recent quarters, which helped to push up longer term U.S. Treasury yields earlier this year. After recording an all-time low of just 0.51% last August, the 10-year Treasury yield peaked at 1.74% in the first quarter of 2021. Since then, the benchmark rate has settled in a range around 1.5% but remains well above 2020 lows.

Although yields may climb farther, we see their ascent as likely to be gradual. That’s partly due to our view that the Fed’s tightening will be measured. But we also see other factors at play. One example is demand by global investors. Many find U.S. yields relatively attractive even after hedging for their home currencies.

Despite the recent rise in inflation and yields, investors’ long-term perspective should not change. We believe, for those seeking balance, fixed income remains essential and should be approached four ways.

1. Get off the sidelines

As June began, investors had $4.6 trillion sitting in money market funds. Their jitters related to fixed income investing in this challenging environment are understandable. However, holding cash or cash-like investments amid higher rates of inflation may not be a favorable investment strategy. In fact, second quarter cash holdings missed out on positive returns in most bond sectors while taking a hit to purchasing power thanks to higher inflation. Investors willing to accept a modest amount of credit and interest rate risk could find high-quality shorter term bond funds a better option.

These funds, such as Capital Group’s Intermediate Bond Fund of America® on the taxable side and Limited-Term Tax-Exempt Bond Fund of America® on the tax-exempt side, prioritize capital preservation while providing a modest amount of income. Due to a focus on high-quality shorter term bonds, these funds aim to have minimal exposure to credit and interest rate risk.

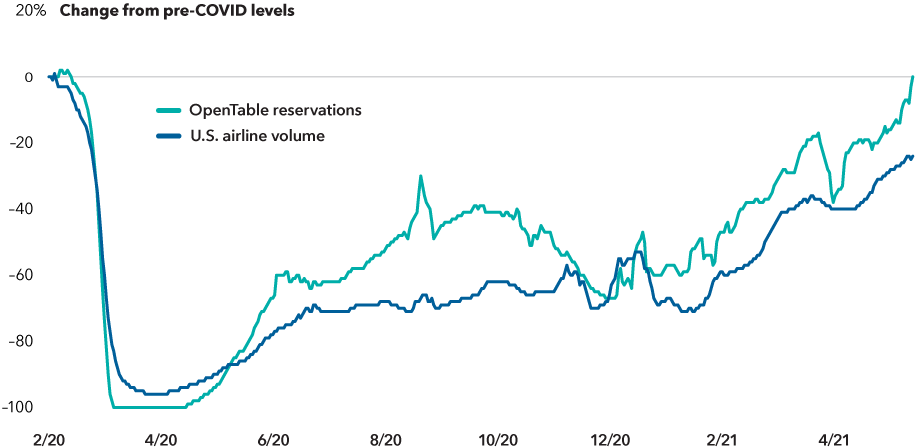

Signs show U.S. consumers are getting out and spending

Sources: OpenTable, Transportation Security Administration. Airline volume represents number of U.S. passengers screened by TSA and uses 2/18/20 as the pre-COVID baseline. All data uses seven-day smoothed averages and is as of 5/31/21.

2. Stay invested in core

Equities have hit new highs in recent quarters. As the recovery continues, so may this positive trend. However, a significant amount of upside is already reflected by current valuations. That means any negative news or setbacks could produce volatility should investors be forced to rethink some of their optimism. Put another way, in an environment when higher risk asset values are soaring, having a strong core bond allocation is as important as ever. This has the potential to provide all four roles of fixed income: Diversification from equities, capital preservation, income and inflation protection.

That last role might be at the forefront of some investors’ minds, given the trend in consumer prices. An actively managed core bond fund has the ability to invest in Treasury-Inflation Protected Securities — government bonds pegged to the Consumer Price Index — as well as other inflation-linked products.

But what about the potential for yields to drift higher? Does that mean capital preservation will fail? Historically, investors who owned high-quality core fixed income generally fared well over a medium-term perspective. Consider the five periods of sharpest yield increases over the past three decades. Following these spikes, two-year returns were positive for the core bond benchmark, the Bloomberg Barclays U.S. Aggregate Index.

Of course, rising yields are ultimately good news on the income front. As yields gradually increase over time, so will bond fund income. Bond funds focused on high-quality securities may also help to soften the impact of volatility on a broader portfolio. Look for a fund to provide a low correlation to equities by having a return pattern that is not closely tied to that of stocks, such as our core and core plus bond funds, The Bond Fund of America® and American Funds Strategic Bond FundSM.

3. Diversify your income

Corporate bonds have felt the positive impact of the strong economic expansion. However, we believe that much of the upside has already been priced into risky asset values. Consider the premium investors are currently paid for corporate bonds over Treasuries. These credit spreads for both investment-grade and high-yield bonds have tightened to pre-pandemic levels, which were already extremely low from a historical perspective.

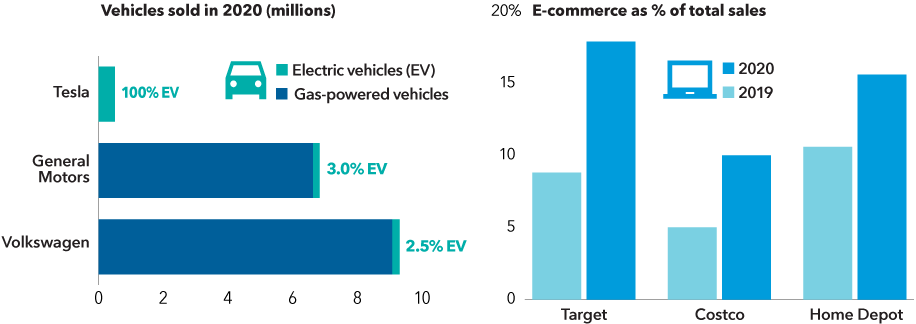

Old-guard companies in autos and retail are adapting to disruption

Sources: Capital Group, company financials, FactSet. General Motors sales includes SAIC-GM-Wuling joint venture. Target and Costco reflect fiscal year 2020 and 2019 sales. Home Depot reflects fourth quarter 2020 and fourth quarter 2019 sales.

Just because credit sectors now look expensive doesn’t mean managers can’t find opportunities. It means they must rely on research to unearth better relative values for investing. A multisector approach can provide the flexibility to pursue the best relative values across varying types of bond issuers. Funds like American Funds Multi-Sector Income FundSM provide managers the ability to pivot to sectors that research highlights as markets evolve. By blending higher income sectors, investors can also potentially capture more yield while reducing the overall volatility of their portfolio.

4. Investors in the highest tax brackets should consider municipal bonds

Some investors are also worried about possible impending federal tax hikes in the U.S. Whether those materialize or not, municipals will maintain a strong value proposition for those in the highest tax brackets. After-tax yields can add a considerable boost for those investors, whether looking at a core municipal fund like The Tax-Exempt Bond Fund of America® or a higher yielding version like American High-Income Municipal Bond Fund®.

There are also fundamental, bottom-up reasons that municipal bonds can be a favorable addition to a diversified portfolio. The impact of some of the massive COVID-related stimulus spending will continue to provide a boost to some municipal bond issuers. Those measures provided as much as $1.2 trillion in support for the sector over the past year. If Washington manages to pass an infrastructure bill this year, it could serve as an additional tailwind for credit improvement in a number of municipal bond sectors.

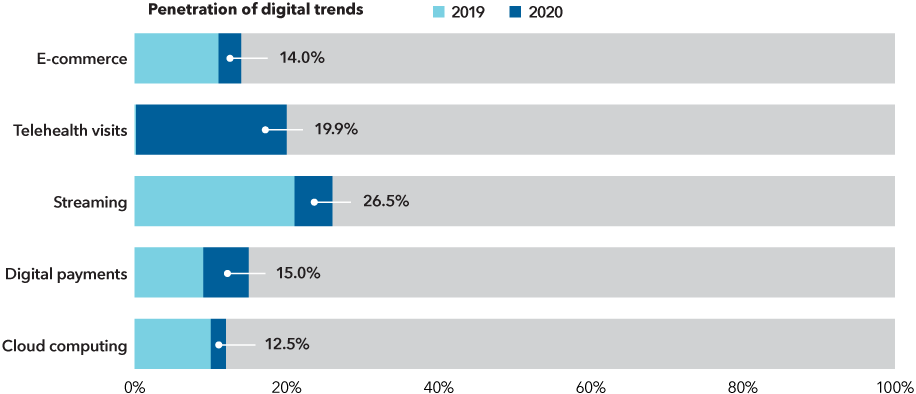

Leading digital trends still have growth potential

Sources: E-commerce = % of total U.S. retail sales (U.S. Census Bureau); telehealth visits = % of total primary care visits that were not in-person visits (U.S. Department of Health & Human Services, as of June 2020); streaming = % of time spent watching TV on streaming content (Nielsen, as of 3Q, 2020); digital payments = % of payments made with digital wallets (Statista); cloud computing = % of total IT spend on public cloud computing (Capital Group, IDC).

The second half of 2021 and beyond is likely to be a more challenging period for fixed income than some investors are accustomed to. But the importance of maintaining a balanced portfolio hasn’t changed. With lofty valuations across many asset classes, having a high-quality fixed income allocation that provides all the roles of fixed income remains essential for investors striving for long-term success.

Learn more about

The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings. Lower rated bonds are subject to greater fluctuations in value and risk of loss of income and principal than higher rated bonds. Income from municipal bonds may be subject to state or local income taxes and/or the federal alternative minimum tax. Certain other income, as well as capital gain distributions, may be taxable. The use of derivatives involves a variety of risks, which may be different from, or greater than, the risks associated with investing in traditional cash securities, such as stocks and bonds.

Bond ratings, which typically range from AAA/Aaa (highest) to D (lowest), are assigned by credit rating agencies such as Standard & Poor's, Moody's and/or Fitch, as an indication of an issuer's creditworthiness. If agency ratings differ, the security will be considered to have received the lowest of those ratings, consistent with the fund's investment policies

American Funds Strategic Bond Fund may engage in frequent and active trading of its portfolio securities, which may involve correspondingly greater transaction costs, adversely affecting the fund’s results.

Methodology for calculation of tax-equivalent yield:

Based on 2020 federal tax rates. Taxable equivalent rate assumptions are based on a federal marginal tax rate of 37%, the top 2020 rate. In addition, we have applied the 3.8% Medicare tax. Thus taxpayers in the highest tax bracket will face a combined 40.8% marginal tax rate on their investment income. The federal rates do not include an adjustment for the loss of personal exemptions and the phase-out of itemized deductions that are applicable to certain taxable income levels.

Bloomberg Barclays U.S. Aggregate Index represents the U.S. investment-grade fixed-rate bond market. Bloomberg Barclays U.S. Corporate Investment Grade Index represents the universe of investment grade, publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity and quality requirements. Bloomberg Barclays U.S. Corporate High Yield Index covers the universe of fixed-rate, non-investment-grade debt. Bloomberg Barclays Municipal Bond Index is a market value-weighted index designed to represent the long-term investment-grade tax-exempt bond market. Bloomberg Barclays High Yield Municipal Bond Index is a market value-weighted index composed of municipal bonds rated below BBB/Baa. Bloomberg® is a trademark of Bloomberg Finance L.P. (collectively with its affiliates, “Bloomberg”). Barclays® is a trademark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Neither Bloomberg nor Barclays approves or endorses this material, guarantees the accuracy or completeness of any information herein and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

For financial professionals only. Not for use with the public.