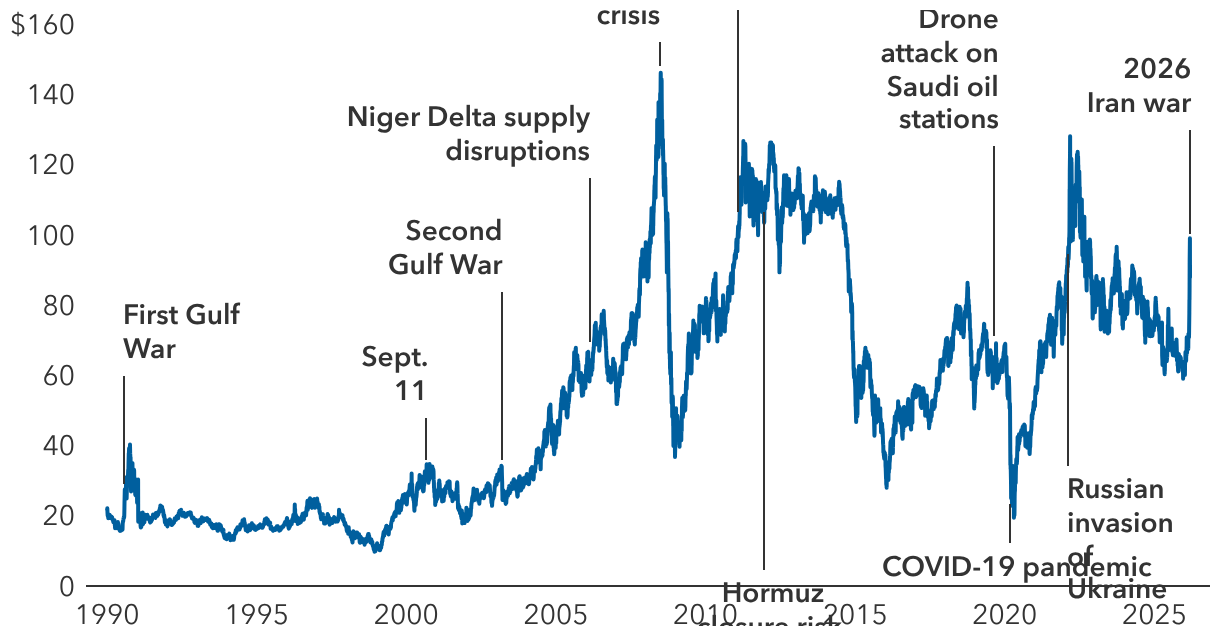

War in Iran has injected new uncertainty into the global economy, reviving concerns that high oil prices could drive inflation up, strain consumer spending and weigh on economic growth.

Prices for Brent crude and West Texas Intermediate (WTI) have zigzagged in recent days, hitting a high of nearly $120 a barrel as war escalated in the Middle East before quickly dropping below $100. As of 10 March, the global Brent price settled at $91.74 per barrel, roughly 26% higher than before the US strike on Iran.

About a fifth of the world’s oil supply moves through the Strait of Hormuz near Iran, so any disruption there will rapidly be reflected in fuel prices. Even in the United States, the world’s largest oil producer, the price of gasoline at the pump has jumped 20% since the US and Israel attacked Iran on 28 February.

“Consumers are quick to react to higher energy prices, often by dipping into savings and cutting back on gasoline use,” says US economist Jared Franz. If oil hovers near $85 a barrel through 2026, he estimates American’s purchasing power could fall by roughly 0.6%.

“The impact may be painful for consumers, but US GDP could remain on track to grow 2.8% this year, with unemployment stable in the range of 4% to 4.5%,” Franz says. “The global economy too, could show similar resilience with growth near 2.8%. But that baseline is fragile if the war drags on.”