Gold prices are likely headed higher

Paul Benjamin, balanced portfolio manager

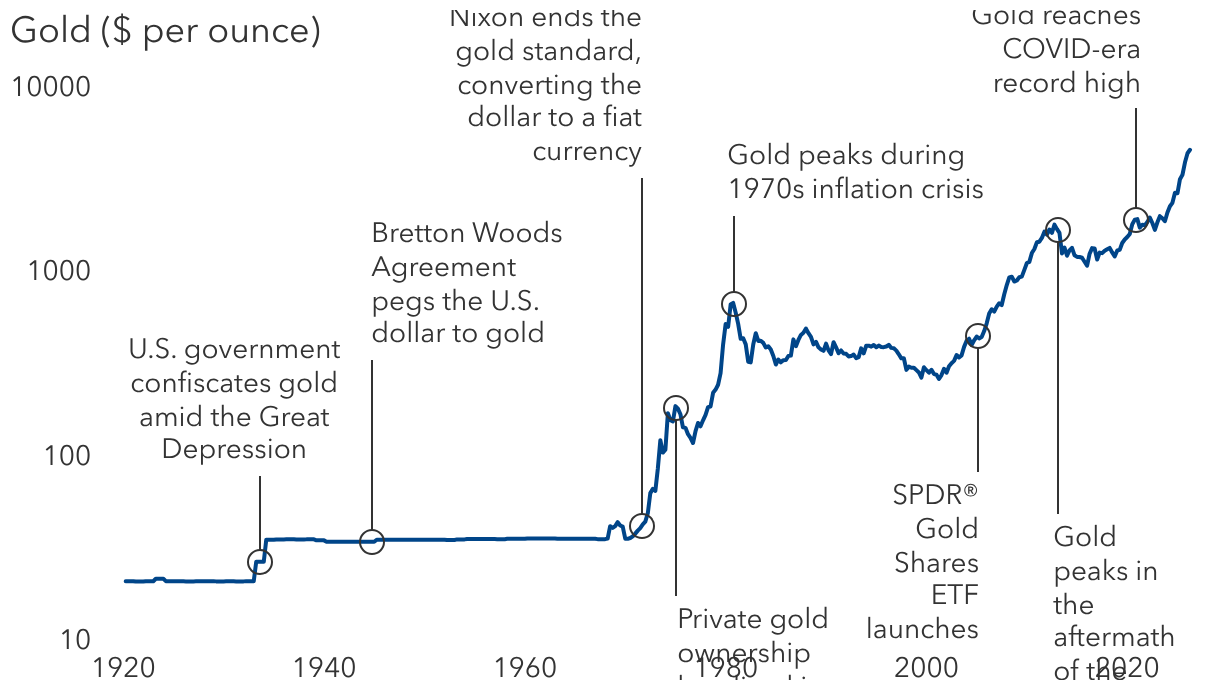

My outlook for gold prices is likely upward, but the magnitude will be determined by the level of real interest rates and real inflation-adjusted return from stocks and bonds. If you were to use a constant basket to define inflation, and you looked at real interest rates minus inflation, you would see that real rates have been very low since the global financial crisis. Gold tends to do well in those periods.

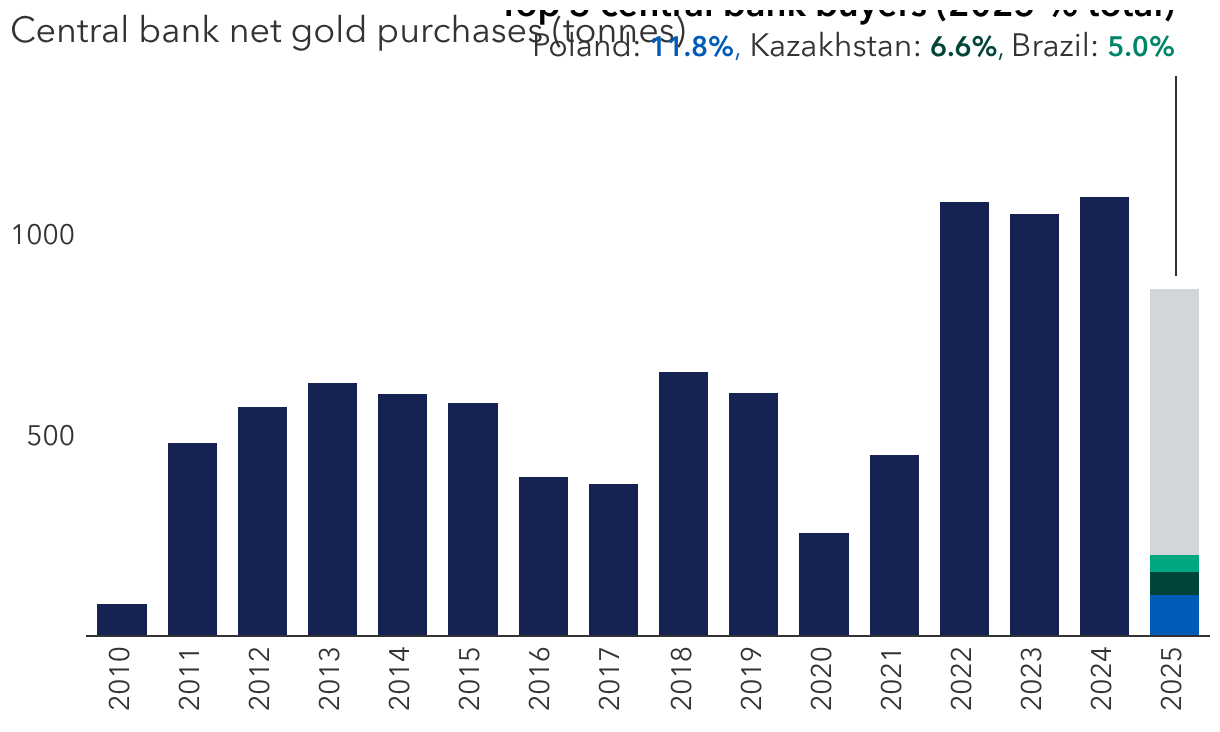

In addition, we had the freezing of Russian Treasury reserves in 2022, which caused central bank buying from non-Western central banks to accelerate dramatically. And then, interestingly, late last year we started seeing lots of news stories about the “debasement trade.” When people refer to the debasement trade, they are talking about fiscal concerns in many Western countries, including a lack of central bank independence and the risk that governments may need to inflate away their debt. I'd say those are the major issues that line up, driving gold and helping it accelerate in recent years.

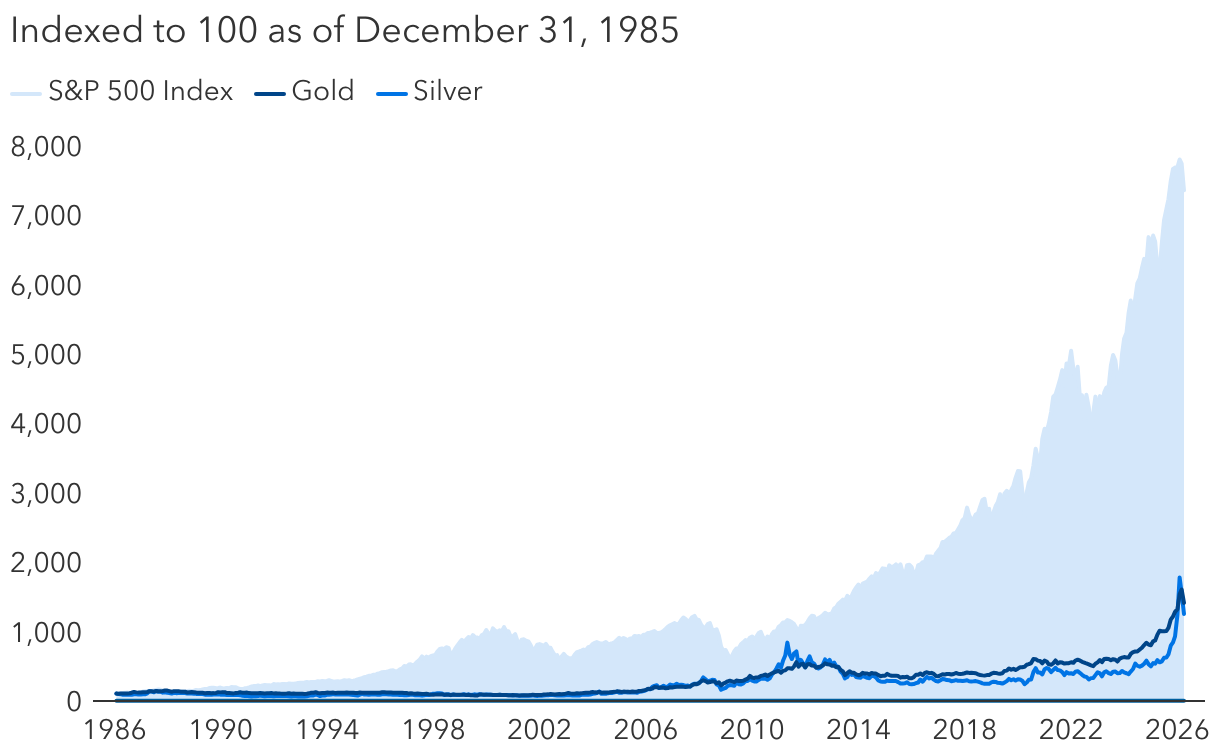

In my view, gold has an important role in a portfolio, particularly in a balanced fund. I view it as an important diversifier. At Capital Group, we don’t buy physical gold or gold ETFs. Instead, I prefer to invest in companies that create value and can do better than if you had just owned gold. They are known as gold streamers: companies like Wheaton Precious Metals, Royal Gold and Franco Nevada. They are not miners. They are effectively finance companies. They make loans to copper miners or gold miners, and the loans are paid back in gold. All three companies have compounded their earnings per share 600 to 900 basis points a year faster than the increase in gold prices. And so they have done exactly what you would want. They have provided the traditional gold hedge while also contributing substantially to growth of capital.

Central banks have been the key to rising prices

Lisa Thompson, equity portfolio manager

Central banks are what I call price-insensitive buyers. They are not investing in gold to beat an index. They have an entirely different objective. They are trying to diversify their reserve base. They tend to be focused on risk and liquidity. When they adjust their asset allocation strategy, they do not care about the price. In my view, that has been the primary driver of gold prices over the past three years. It started with Russia and has extended to many other emerging markets, China being a notable example. But even in markets like Poland, you are starting to see this desire to diversify into gold and away from the US dollar.