United States

Jared Franz

Jared Franz

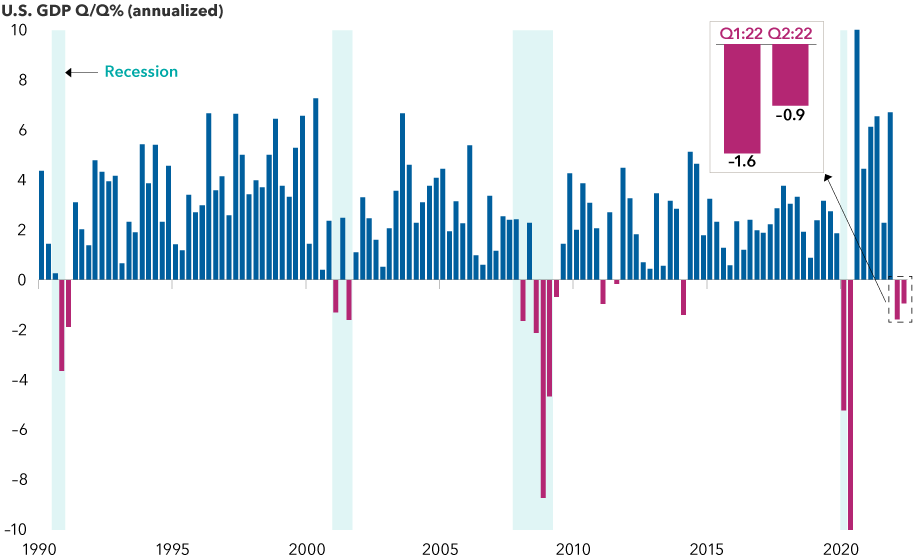

Is the U.S. economy in recession or not? That’s the question on the minds of many investors as U.S. gross domestic product (GDP) declined for two consecutive quarters in the first half of the year, a commonly cited definition of recession.

However, with consistently strong job growth, historically low unemployment and solid growth in consumer spending, that doesn’t sound like a recession most people would remember. So what’s the conclusion?

It depends on who you ask. With food, energy and shelter prices all rising faster than wages, the average American consumer would probably say yes. In my view, we are either on the edge of a recession or we are already tipping into it.

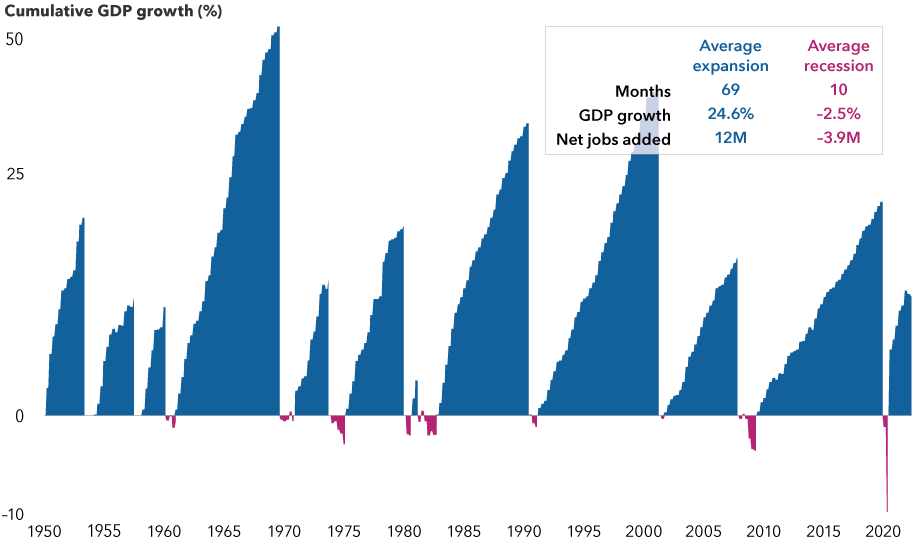

Over the past 70 years, the average U.S. recession has lasted about 10 months and resulted in a GDP decline of 2.5%. The next one may be worse than average, if current trends persist, but still less severe than the Great Recession from December 2007 to June 2009 that accompanied the global financial crisis.

Key economic indicators point to a potential recession

Sources: Capital Group, Bureau of Economic Analysis, National Bureau of Economic Research, U.S. Department of Commerce. Y-axis is limited to a range of –10% to +10% to represent a normalized range, but Q2:20 and Q3:20 exceed this range (at –35.7% and +30.2%) largely due to the pandemic. As of June 30, 2022.

When will we know for sure?

The official arbiter of U.S. recessions, the National Bureau of Economic Research (NBER), takes a while to share its view. The nonprofit group considers many factors beyond GDP, including employment levels, household income and industrial production. Since NBER usually doesn’t reveal its findings until six to nine months after a recession has started, we may not get an official announcement until next year.

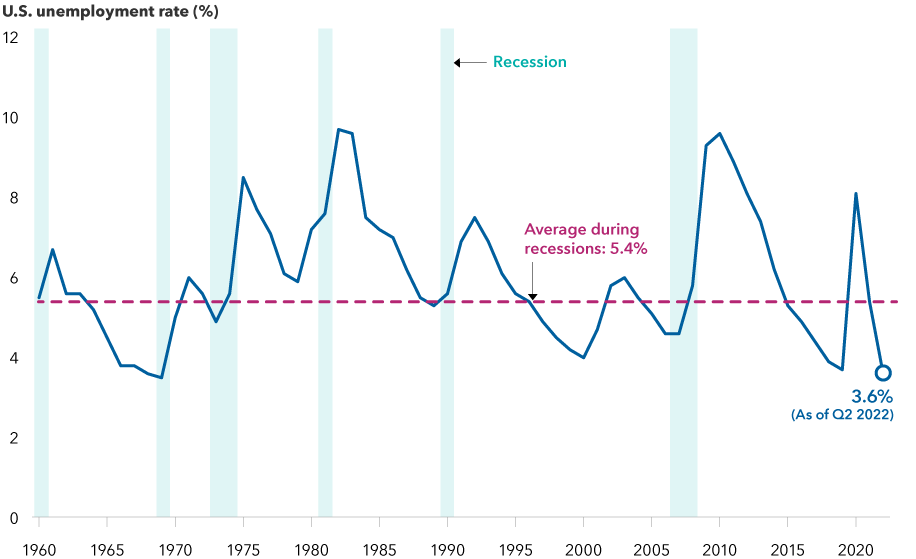

It’s fair to say that most consumers probably don’t care what NBER thinks. They see inflation above 9%, sharply higher energy prices and declining home sales. They feel the impact of those data points. The labor market is one of the only data points that isn’t signaling a recession right now.

The U.S. added 372,000 jobs in June, higher than most economists expected. The unemployment rate remained steady at 3.6%, close to a record low. However, that number reflects a supply-demand mismatch in an economy that hasn’t fully recovered from the pandemic. In the months ahead, I expect greater numbers of jobseekers to return. That should increase the unemployment rate as companies reduce hiring.

One bright spot: A strong U.S. job market

Sources: Capital Group, Bureau of Labor Statistics, National Bureau of Economic Research, U.S. Department of Labor. As of June 2022.

On the surface, consumer spending has also been strong, rising 1.1% in June. But after adjusting for inflation, it’s essentially flat. It also reflects higher spending on necessities such as health care and housing while masking declines in discretionary categories such as clothing and recreation. That spending shift was underscored recently when Walmart and Best Buy issued profit warnings, noting that higher prices for food and energy were hurting sales of discretionary items.

We haven’t seen overall consumer spending or employment levels decline yet, but if current trends persist, I think it’s just a matter of time.

Housing comes under pressure

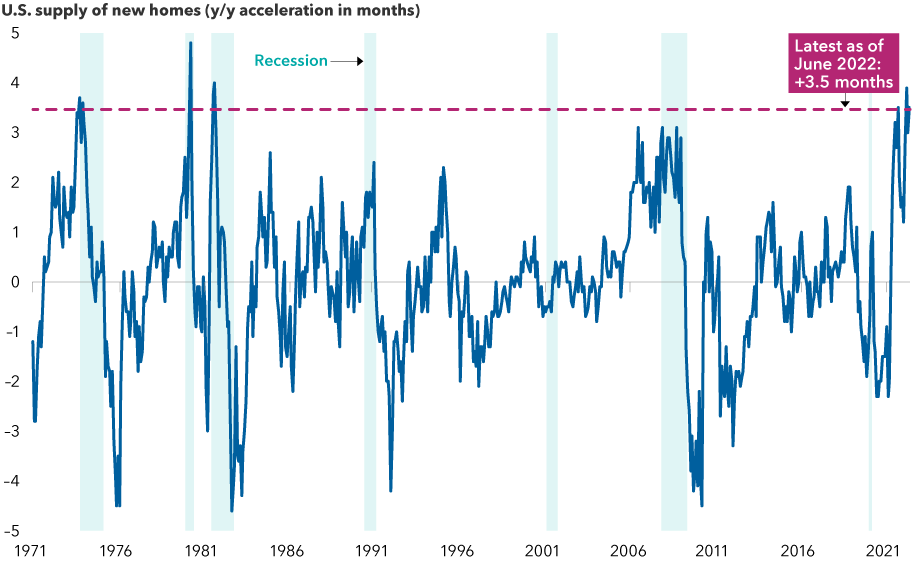

Another troubling sign is the rapid decline in new home sales. With the U.S. Federal Reserve aggressively raising interest rates to fight inflation, mortgage rates have soared in recent months, triggering a sharp reaction in the housing market.

New single-family home purchases fell last month by 8.1%, the biggest drop in more than two years. Sales of previously owned homes tumbled 5.4%, the fifth consecutive month of declines. Additionally, a dramatic rise in home prices during the pandemic raises concerns about the potential for a painful correction.

Rising home inventories suggest this recession could be more difficult

Sources: Capital Group, National Bureau of Economic Research, U.S. Census Bureau. As of June 2022.

When it comes to the impact on the economy, the housing market punches far above its weight. I'm mulling the risk that a larger correction in this sector could increase the depth and duration of the next recession.

Why inflation should subside

If we are heading into a recessionary period, the silver lining could be a reversal of the extreme inflation pressures witnessed over the past year. In June, U.S. inflation hit a 40-year high of 9.1%.

Heightened geopolitical tensions, elevated commodity prices and ongoing supply chain disruptions will likely make it hard for the Fed to sustainably get inflation down below 2%, as it was before the global financial crisis. But high inflation is not likely to turn into hyperinflation.

When the United States went into recession in 1980, then-Fed Chair and inflation hawk Paul Volcker cut rates substantially before raising them back up again. If inflation is persistent, current Fed Chair Jerome Powell could look to follow a similar template.

In fact, the bond market is already pricing in expectations that the Fed will cut rates multiple times in 2023.

Given the uncertainty around Fed policy in a recessionary period, investors should be prepared for ongoing market volatility. But it’s also useful to remember that recessions have not usually lasted very long, and expansions have lasted longer and were far more powerful.

Recessions have been painful but less impactful than expansions

Sources: Capital Group, National Bureau of Economic Research, Refinitiv Datastream. Chart data is latest available as of 6/30/22 and shown on a logarithmic scale. The expansion that began in 2020 is still considered current as of 6/30/22 and not included in the average expansion summary statistics. Since NBER announces recession start and end months, rather than exact dates, we have used month-end dates as a proxy for calculations of jobs added. Nearest quarter-end values used for GDP growth rates.

Institutional investors rely on our newsletter. Have you subscribed?

Our latest insights

RELATED INSIGHTS

Don’t miss out

Get the Capital Ideas newsletter in your inbox every other week