Interest Rates

Categories

Emerging Markets

Emerging markets: What you need to know about the selloff and potential opportunities

Kent Chan

Kent Chan

Stephen Green

Stephen Green

Jens Søndergaard

Jens Søndergaard

August 29, 2018

KEY TAKEAWAYS

- EM equities have been hurt by country-specific risks, dollar strength and global trade uncertainties.

- Investors should expect continued volatility in EM as U.S. rates rise, trade tensions escalate and the political scene worsens in some countries.

- Despite macro uncertainty, the outlook for corporate earnings remains strong with aggregate profits projected to grow by double-digits in 2019.

- We see investment opportunities in companies in Asia-Pacific and India, which are benefiting from technological change and economic growth.

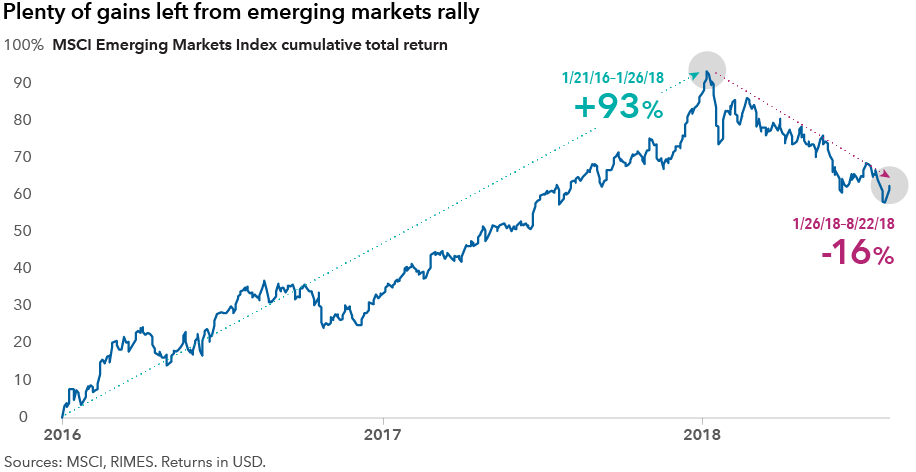

Emerging markets have hit a rough patch, with the benchmark MSCI Emerging Markets Index declining roughly 16% since hitting a two-year high on Jan. 26. The pullback is not a surprise, given the substantial 93% gain over a two-year period that stretched from January 2016 to January 2018.

Political uncertainty and economic turmoil in Brazil, Turkey and Argentina, which are large borrowers in international financial markets, have dragged markets lower at times. On the positive side, corporate profitability continues to be solid, especially for new economy companies in the technology and consumer discretionary segments. Nevertheless, volatility likely will continue as markets search for a new equilibrium.

Emerging markets: Old vs new

Even as we discuss the asset class broadly, it’s good to remember that emerging markets are a collection of very diverse countries at varying stages of economic maturity and political stability. We see two sides of emerging markets: one more defined by innovation and economic stability, and another that continues to be plagued by cyclical swings tied to commodity-related industries and political uncertainty.

The balance of power has shifted to Asian technology and consumer discretionary companies, some of which are now the biggest components of the MSCI EM Index. Mainland-listed Chinese companies, known as A-shares, are being added to the index. And India, now more business-friendly after a series of reforms, has surpassed China as the world’s fastest-growing economy.

“Some of the risks we see in emerging markets have more to do with country-specific and macro-oriented issues and less to do with certain pockets of the Asia-Pacific and India, where our managers believe there are attractive, long-term opportunities to invest in companies benefiting from technological disruption and secular growth,” says Kent Chan, a Capital Group investment director and emerging markets specialist.

It’s also important to remember that this recent selloff comes after a long period of impressive gains, and it appears profit-taking is among the factors contributing to weaker sentiment.

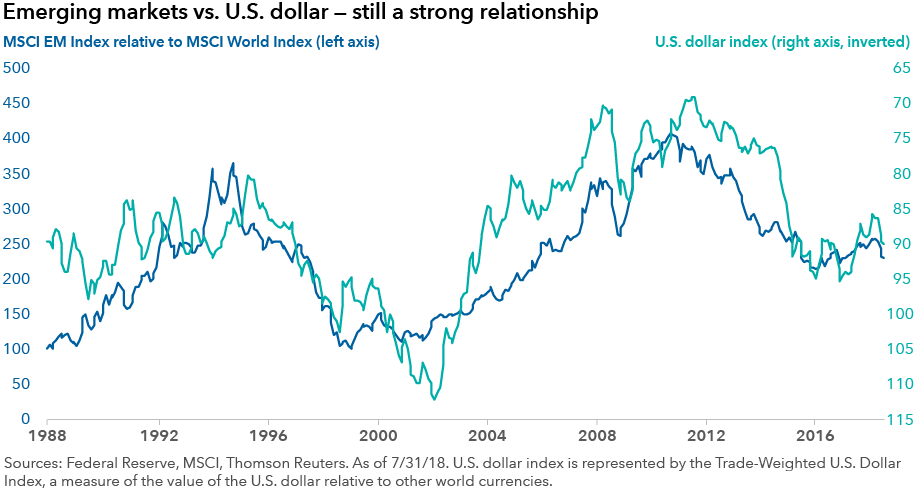

The EM-dollar relationship

A stronger dollar is making conditions difficult in emerging markets and has contributed to some capital flight. Historically, long periods of dollar strength have been a headwind for emerging markets, especially in cases where countries have relied on dollar-denominated debt for financing needs.

After weakening against several foreign currencies last year, the dollar’s rebound has been driven by the relative strength of the U.S. economy compared with Europe, expected U.S. rate hikes, stronger-than-expected earnings from U.S. corporations and increased uncertainty around trade tariffs.

Will emerging markets see any relief? Capital Group currency analyst Jens Søndergaard says further gains for the dollar may be hard to come by.

“For the dollar to rally further you need markets to start pricing even more Fed rate hikes than what’s already priced. That requires the current strong U.S. growth momentum to continue into 2019. It could happen but given the current trade war uncertainties, and signs of slower global growth ahead, I think we are now at peak U.S. growth,” Søndergaard says.

China’s slowdown

China’s economy in the second quarter grew at its slowest pace since 2016. Expect a gradual slowdown over the next six months and into next year, according to Capital Group’s China economist Stephen Green.

“Moves by the Chinese government to curb risks in the country’s financial system, and ongoing global trade tensions, should contribute to the deceleration,” Green says. “Deleveraging remains a priority in Beijing. While authorities are loosening up financing for infrastructure projects and encouraging banks to lend, I don’t think it changes the situation much in the near term. We may not see a stronger policy response in terms of stimulus until next year when more signs of the economic slowdown build up.”

Though it is slowing, China’s economy is still one of the fastest-growing in the world: Its sheer size, growing tech centers and increasing wealth mean there will always be pockets of opportunity for investors.

Portfolio managers in New World Fund® (NWF), and EuroPacific Growth Fund® have been focused on companies involved in internet-connected platforms, financial services, entertainment and travel. These include Hong Kong-listed insurer AIA Group, which has been seeing increased business in China; Alibaba Group, the world’s largest e-commerce business; and Taiwan Semiconductor Manufacturing, a contract-chip manufacturer for Chinese mobile phone companies, which were all top 10 holdings in both funds as of July 31, 2018.*

They’ve also selectively invested in companies that may benefit from the government’s focus on curbing pollution and creating national champions in the health care sector.

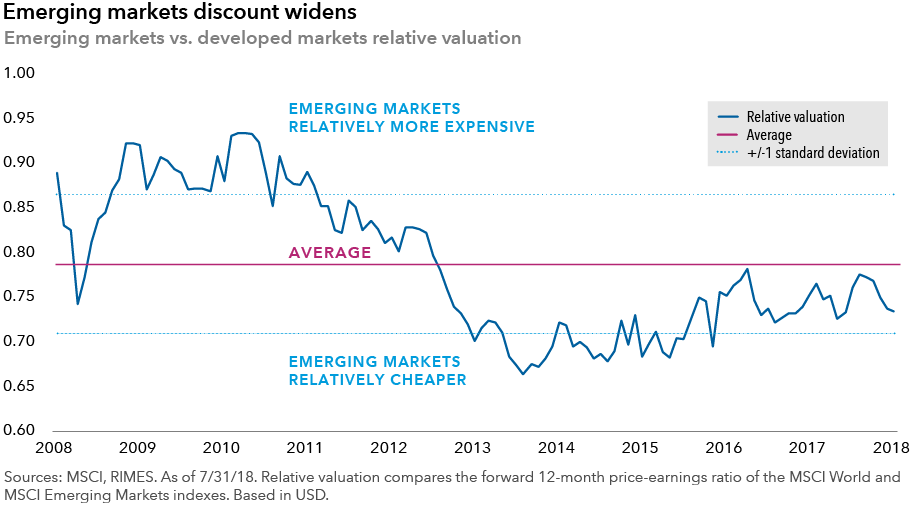

EM fundamentals look attractive

Despite recent volatility, emerging markets could gain support from a combination of factors.

Corporate profitability and debt measures are stronger and improving. Valuations for emerging markets stocks are trading below their 10-year average on a price-to-earnings basis, and the discount has widened recently. At the same time, aggregate profits for companies in the MSCI Emerging Markets Index are estimated to rise by 16% this year and 11% in 2019 on a year-over-year basis, according to estimates by data aggregator FactSet.

Selectivity is key, according to Chan.

“While we follow the macro developments closely, we invest bottom-up in companies that we believe can continue to grow despite geo-political uncertainty, risks of trade barriers and/or economic slowing, he says. “Furthermore, valuations, in some cases, have become even more compelling for companies that we believe have long growth runways as recent volatility is creating more opportunities to invest with our longer-term view.”

Learn more about

*As of July 31, 2018, AIA was 1.6% of net assets in NWF and 2.4% in EuroPacific; Alibaba, 1.3% in NWF and 1.8% in EuroPacific; Taiwan Semiconductor, 1.7% in NWF and 1.5% in EuroPacific.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings. Higher yielding, higher risk bonds can fluctuate in price more than investment-grade bonds, so investors should maintain a long-term perspective.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Our latest insights

-

-

-

Municipal Bonds

-

Artificial Intelligence

-

Technology & Innovation

This is the headline for the Newsletter promo. Customize the message.

RELATED INSIGHTS

-

Market Volatility

-

Global Equities

-

Dividends

Never miss an insight

The Capital Ideas newsletter delivers weekly investment insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only.

American Funds Distributors, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.