Global Equities

Categories

U.S. Equities

Is Big Tech in big trouble?

Brad Barrett

Brad Barrett

Mark Casey

Mark Casey

Tracy Li

Tracy Li

March 9, 2021

Is there such a thing as being too successful, too influential and just too big? We may find out in the months and years ahead as the world’s largest technology and consumer tech companies come under increasingly aggressive antitrust and regulatory scrutiny.

Government efforts to rein in Big Tech have been underway for years, but 2021 is likely to be a watershed moment due to a number of growing pressures. Political, societal and market-based forces are combining to put these companies — Alphabet, Amazon, Apple, Facebook, Microsoft and others — under the microscope.

“The sheer size of these companies means they're going to get a lot of scrutiny from every part of society, including government and regulatory agencies,” explains Mark Casey, a Capital Group portfolio manager who has covered the tech industry for more than 20 years.

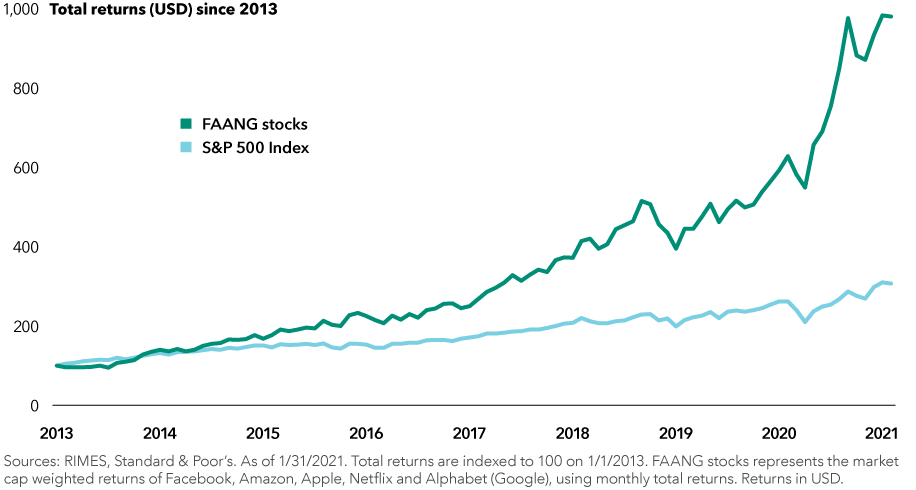

The rise of Big Tech: FAANG stocks have dramatically outpaced the S&P 500 Index

“Some of these companies have also played key roles in the past two U.S. presidential elections,” says Casey. “When you bring politics into the mix, that helps explain why these regulatory discussions are very prominent right now.”

In addition, the COVID-19 pandemic has accelerated the growth of many tech companies, increasing their power and influence during a severe global economic downturn. Of the top 10 U.S. companies by market capitalization, five are technology or digital businesses and their total market value exceeds USD$7 trillion — a figure that has grown by 54% over the past year alone.

Landmark litigation is underway

With that territory comes major league antitrust and regulatory risk:

- In October 2020, the U.S. Department of Justice filed an antitrust lawsuit against Google, alleging the internet search giant stifles competition. It’s the biggest antitrust case since the government targeted Microsoft in 1998.

- In December 2020, the Federal Trade Commission sued Facebook on similar claims that the social media network engaged in anticompetitive practices with its acquisitions of Instagram and WhatsApp.

- Many U.S. states have joined these two landmark legal actions while, at the same time, countless legislative efforts are underway at the state and federal levels.

- A bill introduced in the U.S. Senate in early February 2021 could make it more difficult for large companies to acquire competitors. In Florida, state lawmakers are considering legislation that would fine social media companies for de-platforming political candidates.

“Part of what makes this so complicated,” Casey notes, “is that Democrats have a whole set of issues with these companies — largely based on antitrust, privacy and hate speech concerns — while Republicans have another set of issues, particularly when it comes to the perceived censorship of conservative viewpoints. So there’s really no easy scenario where these companies can just make a few changes and everybody’s happy.”

Another element accelerating the regulatory push is the recent episode involving a group of retail investors who organized themselves on an internet chat board to drive up the stock prices of GameStop, AMC Entertainment and other struggling companies. When brokerage firms and trading apps imposed trading limits, some of those retail investors lost big. In a rare bipartisan move, Republicans and Democrats have called for Congressional hearings, which are expected to begin this month.

European influence

U.S. politicians and regulators seeking to limit the power of Big Tech can look to Europe for inspiration. European authorities have been far more aggressive in their regulatory efforts, including the threat of huge fines for violating data protection rules and engaging in anticompetitive behaviour.

The European Union was the first to enact major online privacy laws in the form of the General Data Protection Regulation, adopted in 2018. EU officials have since followed that up with a series of proposed regulations designed to block certain acquisitions, curb hate speech and provide more information to consumers about how their data may be used for targeted advertising.

“Many of these provisions are already being implemented by U.S.-based internet platforms because of the European regulations,” says Brad Barrett, a Capital Group analyst who covers ad supported internet companies. “Europe doesn’t have many of its own national champions in the social media industry, so it’s perhaps easier for the EU to be more aggressive in this area and for the U.S. to follow when it makes sense.”

So far, Barrett notes, the EU rules haven’t had a major impact on technology companies from a profit or revenue perspective.

FAANGs have proven to be unique while revolutionizing different industries

Regulators face uphill battle

Assessing the regulatory risks of large tech companies is a complex task, Barrett explains, given that they operate in different industries with vastly different competitive profiles — everything from retail to advertising to television. That said, in his assessment, the antitrust cases against Google and Facebook aren’t strong and likely won’t result in any forced breakups.

The government is facing “an uphill battle” to win these cases, Barrett says, evidenced by the fact that some members of Congress are pushing hard for changes in antitrust law.

“That by itself is an admission that it’s difficult to find antitrust violations based on case law going back 20 to 30 years,” he adds.

Not to mention that many of the products provided by Google and Facebook are free, diminishing traditional antitrust arguments that rely on pricing power to help determine monopoly status.

Is regulatory risk already priced in?

How should investors evaluate the outlook for Big Tech, given the potential for some sort of government intervention in the years ahead? One important question to ask is: Do company valuations reflect the risk? In other words, are they “priced in” to the stocks?

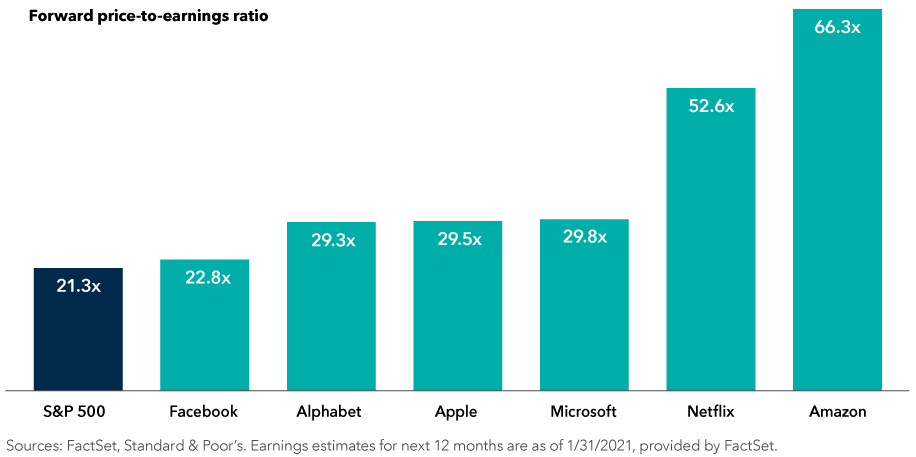

Looking at the FAANG stocks as a bellwether for regulatory risk, the two companies that are currently at the centre of high-profile lawsuits — Facebook and Alphabet — are trading at significantly lower price-to-earnings ratios than, for example, Amazon and Netflix. In fact, Facebook is trading just above the average P/E for the Standard & Poor’s 500 Composite Index despite its rapid growth rate and strong free cash flow.

Valuations for some Big Tech companies don’t look excessive

Last week, Facebook reported a fourth-quarter profit of USD$11.2 billion, a 52% increase from the same period a year ago. Alphabet, which trades at a slightly higher P/E than Facebook, reported a quarterly profit of USD$15.7 billion, up 40% from a year ago.

“These companies operate in large and growing markets, they have long revenue runways and they are very profitable,” explains Capital Group investment analyst Tracy Li, who covers internet companies. “If the regulatory risks were not present, in my view, they would be trading at higher multiples.”

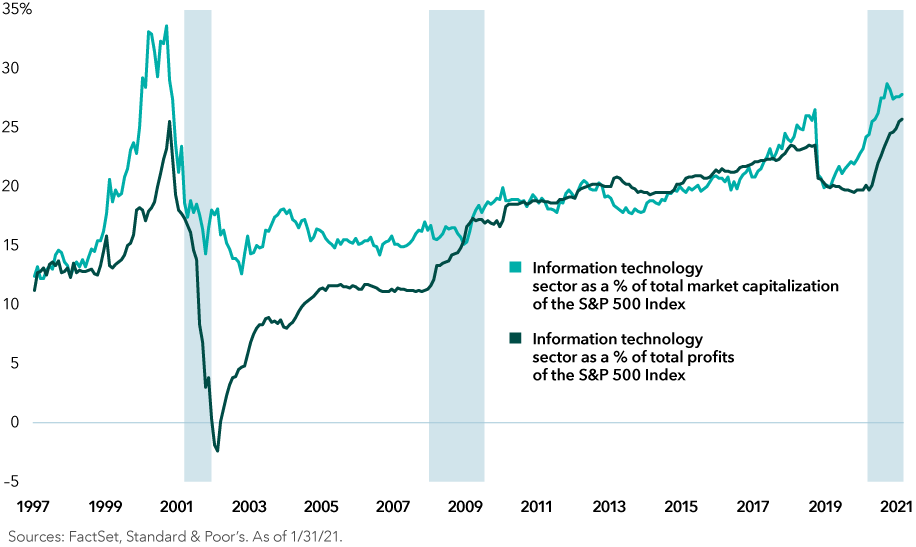

Unlike the dot-com bubble, tech company profits are more in line with prices

Breakup risk: The parts may be greater than the whole

In the unlikely event that one or more of these companies is forced to break up, a reasonable argument could be made that some of the spinoffs could be worth more on their own, Li notes. Indeed, sometimes the parts can be worth more than the whole.

WhatsApp, for instance, which was acquired by Facebook in 2014, currently does not make money. But as a stand-alone company, it would likely command a high valuation due to its user base of more than 2 billion people in 180 countries and the opportunity to monetize the service in the future. The same could be said for Instagram and Facebook Messenger.

“The fact that all of these businesses are under one umbrella does tend to obscure the value of each business,” Li says. “As we’ve seen with past antitrust cases, such as the breakup of AT&T or Standard Oil, the results can be quite favourable to shareholders over the long run.”

Learn more about

Our latest insights

-

-

Technology & Innovation

-

Demographics & Culture

-

-

Emerging Markets

RELATED INSIGHTS

-

Global Equities

-

Technology & Innovation

-

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.