Global Equities

Categories

U.S. Equities

Roaring ‘20s: How pent-up demand could fuel recovery

Chris Buchbinder

Chris Buchbinder

Todd Saligman

Todd Saligman

Lisa Thompson

Lisa Thompson

March 11, 2021

Could pent-up demand for travel and leisure drive a Roaring ‘20s today?

“I think the quick introduction of vaccines is a major game changer, even with all the growing pains we are seeing in terms of distribution,” says equity portfolio manager Lisa Thompson. “A travel recovery is coming, and I think it can happen relatively quickly. Everybody is eager to go on vacation or to just get out and do stuff. The question is whether the recovery has legs. I think we will have to see how the vaccine rollout evolves, among other things.”

Ready, willing — and able — to spend

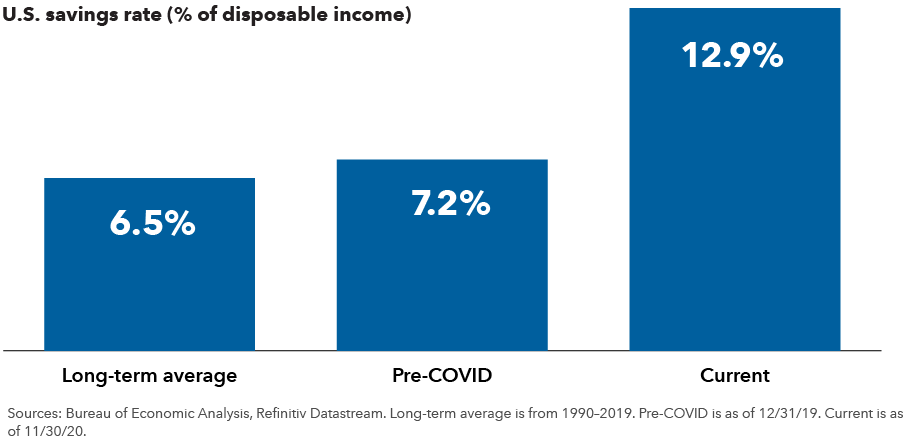

Indeed, cabin fever appears to have taken hold of consumers everywhere. There are signs that consumers are prepared to act: Savings rates have soared since the start of the pandemic, and though they have slowed a bit in recent months they remain relatively high.

Many consumers in the U.S. have boosted their savings during the pandemic

“Once there’s an all-clear, I expect the desire to travel plus the ability for many consumers to spend means we could see a powerful recovery, even if it takes a few years,” adds Thompson, who has spent more than 30 years as a professional investor.

“This crisis is much different than the global financial crisis in 2008 or any of the other crises I’ve seen in my career. Today, looser fiscal policy, looser monetary policy, a very strong banking system and high personal savings rates could help drive a very sharp pickup in demand.”

These conditions not only can benefit the travel and leisure industries but also the broader economy. To be sure, there will probably be hiccups along the way, and some areas will likely recover more quickly than others.

Passenger loyalty: A tailwind for cruise lines

Cruise ships became the epicenter of the COVID crisis in February 2020, when 3,700 people were quarantined aboard the Diamond Princess after a shipboard outbreak. At the time, the ship accounted for half of all known cases outside mainland China.

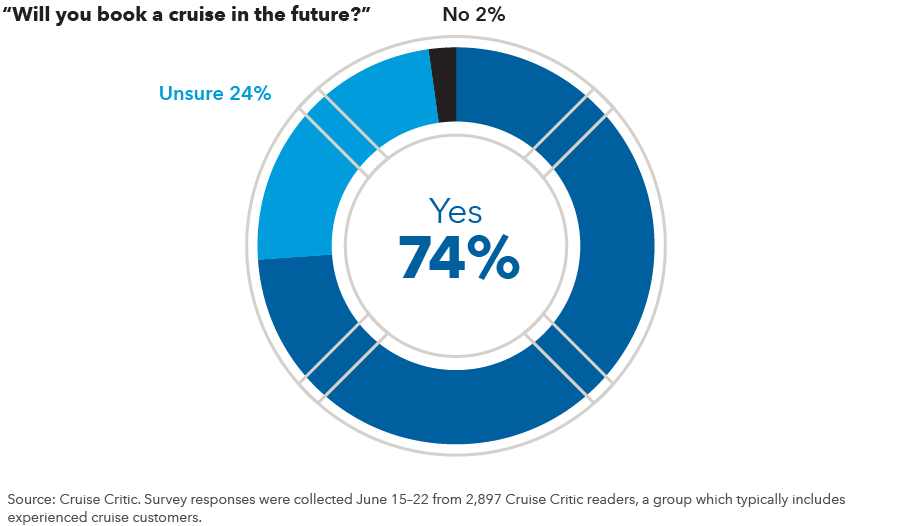

“This industry has gotten so much negative media, yet people are still booking cruises for 2021 and 2022 at prices higher than they were in 2019,” says equity analyst Todd Saligman, who covers cruise lines and U.S. and European airlines. “That’s pretty indicative of the demand. There is a loyalty and enthusiasm among cruisers that people who don’t cruise may fail to appreciate, and that loyalty has persisted through the crisis.”

In fact, more than 70% of respondents to an industry survey said they will cruise again.

Loyal customers can keep cruise industry afloat

While cruising has resumed in Europe, the U.S. Centers for Disease Control imposed a “no sail” order that has not yet been lifted in North America.

“It’s not clear when the ships will set sail again, but I believe they will be cruising near full utilization quicker than many people expect,” Saligman says.

Although cruise stocks have rebounded from their March lows, Saligman believes select cruise lines continue to represent opportunity for long-term investors.

What’s more, with intense focus on healthy sailing practices, “There’s a case to be made that they could one day be considered among the cleanest places on earth to vacation,” says equity portfolio manager Chris Buchbinder.

Vacation plans up in the air

As was the case in the cruise industry, global air travel was down an estimated 66% in 2020, about 20 times worse than the previous record. Within the U.S., which is more dependent on business travel, the devastation was worse: Air travel declined as much as 95% in the early months of the crisis.

The rollout of the vaccines and prior experience gives Saligman confidence that demand will bounce back. “I believe it will happen quickly as the vaccine rolls out,” he says. “We also saw this after the September 11 attacks. A lot of people thought consumers would never fly again, and traffic recovered quickly.”

Indeed, in China, where the virus is largely under control and the economy has rebounded, domestic air travel has nearly returned to pre-COVID levels.

Air travel in China has soared back. Will the U.S. soon follow?

The ripple effect

A revival in travel demand can also have a powerful ripple effect, creating the need for a range of goods and services and helping drive job growth across a variety of industries. Among these are aircraft manufacturers, jet engine makers, hotels, casinos and restaurants — all of which were devastated by the pandemic.

Consider aircraft engine makers, which operate a recurring revenue business model. Companies like Safran and General Electric build the engines and sell them at a modest profit, but the engines must be serviced regularly, and the engine makers can generate a great deal of revenue from the service contracts.

“They're not making any money this year, because airplanes are grounded, but as air travel resumes, those manufacturers will potentially see their cash flows rebound,” Buchbinder says.

Unlike other sectors of the economy during COVID, aircraft engine makers are not going to see digital disruption upend their business. “After all,” Buchbinder adds, “there are no digital aircraft engines.”

Markets tend to anticipate recoveries

Markets often anticipate recoveries in the underlying economy, so it’s important to recognize underlying trends early. Consider the global financial crisis, a period when the housing and automobile industries were severely beaten down. By 2012 it became clear that demand was building, thanks to changing demographics and an aging auto fleet. In both industries, a full recovery took several more years, but a rebound in auto- and housing-related stocks anticipated the recovery in demand and earnings. From February 2009 through December 2010, auto sales fell 6% while auto stock returns advanced 496%.

Auto stocks rebounded ahead of sales after the global financial crisis

More recently, since the introduction of the vaccines, shares of companies across a number of travel-related industries have registered strong gains. Select companies likely have room to run, Buchbinder says.

“The market often runs ahead of the actual recovery in earnings,” he says. “I think a year from now we will be in a very different environment where demand and earnings for some of these companies will begin to recover in a more meaningful and sustained way. Our job as investors is to identify those companies that stand to benefit most from the changing environment.”

Maintaining a balance

Students of history can look to many examples of past crises and declines that were followed by powerful recoveries thanks in part to pent-up consumer demand. Examples include the travel sector after 9/11 and the housing and auto industries following the end of the great financial crisis in 2008–2009.

As long-term investors, Capital Group’s investment professionals seek to identify trends early enough to select the companies that stand to benefit from these dynamics. For investors and their advisors, it is important to make sure portfolios are balanced with exposure not only to growth strategies but also to strategies focused on more value-oriented companies, like many of the travel-related stocks.

A review of more than 4,000 U.S. portfolios by Capital Group’s Portfolio & Analytics team found that investors significantly reduced allocations to value equities over the last three years. It may be time to rebalance.

Returns for leading growth companies have continued to be strong, for good reason. But it may be shortsighted for investors to become seduced by the runaway growth stories, considering that many of the beaten down stocks in travel and other sectors have attractive valuations. And recently there have been some early signs that the market rally may be broadening as many of these stocks have posted meaningful gains.

Investors have scaled back their exposure to value funds

“We’ve just been through a market downturn and recovery where the great secular growth companies led during the decline and on the way back up,” Buchbinder says. “That is a historically unusual pattern. As the vaccines roll out and the recovery broadens we will begin to see companies in the travel industry, or perhaps energy or financials, all of which had been very hard hit during the downturn, participate in the recovery.”

Learn more about

Our latest insights

-

-

Technology & Innovation

-

Demographics & Culture

-

-

Emerging Markets

RELATED INSIGHTS

-

Demographics & Culture

-

Long-Term Investing

-

Global Equities

©2021 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capital Group‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capital Group. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capital Group funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capital Group trademarks are owned by The Capital Group Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capital Group funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capital Group, a global investment management firm originating in Los Angeles, California in 1931. Capital Group manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capital Group funds offered on this website are available only to Canadian residents.